www.globalbankingandfinance.com Issue 43 Alli a nz Trade in Asia Pacific CEO On Group’s Go2025 Strategic Plan Paul Flanagan

Varun Sash

Editor

Wanda Rich email: wrich@gbafmag.com

Head of Distribution & Production

Robert Mathew

Megan Sash, Amanda Walker

Video Production and Journalist

Phil Fothergill

Graphic Designer

Jessica Weisman-Pitts

Chanel Roberts

Rick Saikia, Monika Umakanth, Stefy Abraham,

Samuel Joseph, Dave D’Costa

Advertising

Phone: +44 (0) 208 144 3511 marketing@gbafmag.com

GBAF Publications, LTD Alpha House 100 Borough High Street London, SE1 1LB United Kingdom

Global Banking & Finance Review is the trading name of GBAF Publications LTD Company Registration Number: 7403411

VAT Number: GB 112 5966 21 ISSN 2396-717X.

The information contained in this publication has been obtained from sources the publishers believe to be correct. The publisher wishes to stress that the information contained herein may be subject to varying international, federal, state and/or local laws or regulations.

The purchaser or reader of this publication assumes all responsibility for the use of these materials and information. However, the publisher assumes no responsibility for errors, omissions, or contrary interpretations of the subject matter contained herein no legal liability can be accepted for any errors. No part of this publication may be reproduced without the prior consent of the publisher

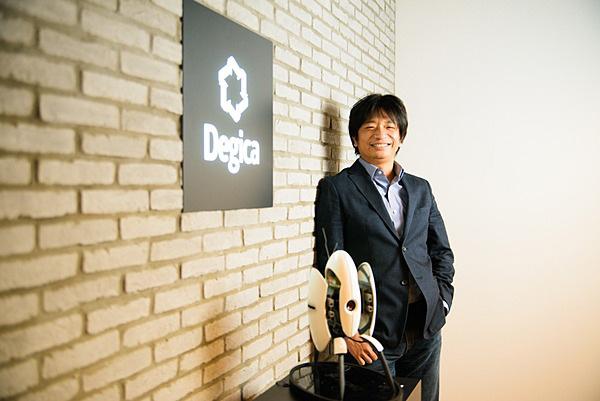

Allianz Trade, formerly Euler Hermes and part of the Allianz Group, is international world leader in trade credit insurance (TCI). Its product offering also includes surety bonds, guarantees and business fraud insurance. Since 1910, Allianz Group has had a presence in the Asia Pacific region, where it currently serves 21 million customers. I got the lowdown on Allianz Trade’s Go2025 strategic plan in a recent interview with Paul Flanagan, Regional CEO of Allianz Trade in Asia Pacific. (Page 24)

In this edition we also take a look at the impact of the Metaverse and GenZ on banking, delve into the ethics and risks in using AI-generated content, and explore the impact of consumer sentiment as recession fears rise.

We strive to capture the latest news about the world's economy, financial events, and banking game changers from prominent leaders in the industry and public viewpoints with an intention to serve a holistic outlook. We have gone that extra mile to ensure we give you the best from the world of finance.

Send me your thoughts on how I can continue to improve and what you’d like to see in the future.

Stay caught up on the latest news and trends taking place by signing up for our free email newsletter, reading us online at http://www.globalbankingandfinance.com/ and download our App for the latest digital magazine for free on Google Play and the Apple App Store

I am pleased to present

Issue 43 of Global Banking & Finance Review. For those of you that are reading us for the first time, welcome.

the

Beaudreau

The metaverse presents exciting opportunities for banks when it comes to customer experience and managing transactions.

It will go beyond existing digital banking opportunities to create an immersive experience using technology like augmented reality (AR), virtual reality (VR) and artificial intelligence (AI) – in addition to other technologies such as blockchain and NFTs.

It will revolutionise the way banks engage with their customers, both in the products they offer and the new marketplaces they can explore. Given the demographics of likely metaverse users, it also has great potential to reach new customer segments.

Financial services companies are already starting to explore the metaverse

In December 2021, Bloomberg Intelligence predicted that the metaverse “revenue opportunity” could be worth $800bn as early as 2024.

We’re seeing financial institutions take their first steps towards banking in the metaverse.

JP Morgan, for example, has its Onyx lounge in Decentraland, an openworld metaverse environment built on the Ethereum blockchain. Spain’s CaixaBank also has a version of its imaginCafé there.

HSBC and Standard Chartered have purchased virtual land in a metaverse environment called The Sandbox.

To avoid disintermediation, card providers are also exploring opportunities, with American Express filing patents to provide metaverse payment services, for example.

This is just the beginning of the metaverse journey for traditional retail banks, which are starting to think about how they can use the metaverse to achieve business goals (such as customer experience and service). But first, they need to understand what the metaverse is, how it works and how financial services can play a role. They need to know about the platforms, technologies and ecosystems in play and how they can use them to shape a metaverse strategy that has customer experience at its core.

How will the metaverse revolutionise retail banking?

While the introduction of so many new technologies will be disruptive to traditional retail banks, they’re also a massive opportunity. As cryptocurrencies become more mainstream and people want to trade digital assets as easily as they do physical ones, they’ll need banking services that facilitate and protect their transactions.

The metaverse will allow banks to differentiate themselves in several ways. Here are three core services that retail banks may want to think about, and how the metaverse could enhance them.

1. Using immersive, virtual experiences to attract and engage new customers

As the metaverse becomes more mainstream and more consumers start to use it, those consumers will start to need financial products and services designed with the metaverse in mind.

Younger generations already spend a lot of time playing games and socialising digitally. As more of them start to embrace NFTs and the metaverse, they’ll likely be more predisposed to using virtual goods and buy digital assets.

The metaverse will allow retail banks to reach new customer segments like creators, gamers and creatives who are creating multiple sources of income for themselves and looking for help – like instant loans – from banks as they seek to improve their presence in the metaverse.

One emerging strategy for retail banks is to create educational experiences and engage and connect with customers by setting up virtual lobbies and displaying demos on financial wellness and planning. Quontic Bank has started doing this in Decentraland, for example.

2. Providing innovative products and services

As well as providing the needed metaverse-specific products and services, we could see banks developing virtual world platforms – allowing their customers to seamlessly complete transactions between physical and virtual worlds.

We’re already seeing financial services companies develop metaversespecific products. For example, TerraZero Technologies claims to offer the first-ever metaverse mortgage for customers who are looking to buy virtual real estate. This “virtual land grab” is one of the hottest trends we see within the metaverse.

Decentralised finance (DeFi) facilitates borrowing and lending of cryptocurrency against collateral (which could be an NFT or blockchain token-based digital asset). As more consumers and organisations join the metaverse, we’ll see more decentralised autonomous organisations (DAOs) make the metaverse increasingly accessible - creating fairer ways to invest in

and monetise digital assets. Again, this kind of ethical investment environment is likely to appeal to younger customers.

Banks are also considering supporting digital payments by launching credit or debit cards that customers can use to make secure payments in the metaverse. They could also allow for secure lending against NFT assets and help facilitate the metaverse real estate market.

Retail banks, like all financial institutions, are looking for innovative ways to attract and retain talent now that hybrid and remote working models are becoming the norm.

Immersive technologies like AR and VR will become standard ways to foster creative, collaborative and inclusive environments for employees. We’re already seeing personalised avatars, for example. These will include services like Microsoft Mesh for Teams and Meta’s Horizon Workrooms.

The metaverse will offer a great way for retail banks to provide an engaging employee experience and promote a general feeling of ‘togetherness’. It will help attract and retain talent as well as offer new ways to train employees through virtualisation and gamification.

We could even see on-demand, AIpowered digital coaches training employees and providing interactive and immersive metaverse-based learning experiences.

Bank of America already offers immersive and engaging training using VR, where employees can learn via scenarios played out in a simulated environment.

It is clear that the metaverse will give banks powerful new ways to connect with their customers. Right now, it might be hard to imagine the benefits that banks and customers could gain from this new virtual world–it’s still in its very early stages, and a lot of people remain sceptical of its potential. The truth is, we don’t yet know the full potential of the metaverse (in the same way we didn’t really know the full potential of the internet in its very early days).

However, now is the time to start thinking about it and planning for success. We’re already seeing financial institutions taking calculated risks by innovating in this area. Banks that start thinking about metaverse products and services now will find themselves in a very competitive position by the time consumers are ready to fully embrace this brave new world.

Owen Wheatley Lead Partner for Banking & Financial Services ISG (www.isg-one.com)The global supply chain is, in essence, the movement of goods between manufacturers, retailers, and consumers. It is a complex web of moving parts that is, in its current state, is easily impacted by an array of external factors. As of July 2022, consumers have seen an increase in fuel, food, and energy prices, alongside a short supply of brands and items. In the USA, for example, consumers have seen a shortage of babyrelated products, like baby formula, throughout 2022 due to issues with the supply.

New SAP research shows that almost a quarter of decision-makers anticipate that supply chain issues will remain a problem in the summer of 2023. This daunting prospect has encouraged some retailers to rush investment into technology solutions, like artificial intelligence and machine learning, in an attempt to find a solution. However, a strong focus on perfecting the fundamentals of supply chain systems would be a far more effective approach.

The global supply chain itself has undergone significant change during the last two years, driven largely by the ripple effect of the COVID-19 pandemic. Recent reports suggest that hybrid working models have transformed customer expectations of retail experience: 27% of consumers and 36% of Gen Z prefer a hybrid shopping model with a blend of digital and physical channels. As a result, retailers are now under increased pressure to not only deliver a streamlined and effective online experience but also to bring digitalisation into their stores to

improve customer experience in-store as well. Tech-enabled touchpoints that allow customers to locate products, order food, and self-checkout easily are just some of the tools that customers have grown to expect as part of their retail experience.

This transformation has also come at a time of huge disruption for the supply chain. The traditional supply chain model, “just in time”, failed to hold under the pressure of the pandemic, where demand for goods outweighed the supply. Lockdown gave some consumers excess cash, saved from spending less on expenses like travel and eating out, which drove up demand for goods, and an appetite for accessible and intuitive online shopping experiences.

The pandemic was only the start of problems for the supply chain. Rising fuel prices and a shortage of HGV drivers are driving up the cost of transporting goods through these traditional systems and putting an increased burden on supply chain managers to adapt. Additionally, disruptors such as the war in Ukraine and new coronavirus outbreaks in China are interrupting trade and forcing retailers to move away from specific regions for goods: exacerbating an already strained supply chain.

It is clear, therefore, that retailers need to rethink how they approach the supply chain and reinvest time into ensuring their foundations are secure. By developing a concrete foundation, retailers can limit the disruption that external factors might have on their supply.

The pandemic forced many retailers to adapt quickly to manage business disruption in an unprecedented set of circumstances. However, now is the chance for retailers to focus on getting the fundamentals right and optimising their supply chain.

The key to this is redefining how we perceive supply chain disruption. First, a distinction must be made between supply chain disruptors and poor supply chain management. Whilst geo-political situations disrupt the supply chain, they are not the root cause of why we’re missing products off our shelves. Instead, it results from clients struggling to react to the market and feeling the effects of chronic underinvestment in supply chain technology.

Some retailers, most notably those in the fashion industry, have turned to near-shoring solutions which involve bringing manufacturing closer to end consumers. Inditex, a fast-fashion giant, now manufactures 53% of its fashions in Europe. This not only reduces shipping costs and increases the reliability of their supply but can also improve a company’s environmental impact.

Others have turned to new technology to improve their delivery services. Dark stores and automation, from factory robotics to delivery drones and autonomous vehicles, have become popular methods for improving efficiency.

However, getting the basics right is often found to be the most effective way to elevate a delivery service. General merchandiser Target, for example, has released an app that allows shoppers to switch from pick-up in-store to drive up or send someone in their stead, all changeable in real-time with a couple of clicks. The solution works as it addresses a key consumer issue, the collection of goods, in a quick, accessible, and intuitive way, without any over-complication.

Perhaps the biggest struggle facing retailers is predicting demand and optimising their supply chain to reflect uncertain times. This has become clear during the last few years when demands have become more volatile, and retailers have struggled to keep up.

An effective system that maps your supply against demand allows you to plan a strategy to sustain your growth. This is where Data and Analytics Platforms become essential.

Access to real-time data insights allows businesses to plan for seasonal peaks and react to the unexpected. The lockdown showed that businesses that were unable to adapt to demand quickly, for example, and didn’t meet demands for eCommerce solutions, suffered

the most. By equipping yourself with a real-time understanding of supply and demand, you can bolster yourself against these potential disruptors rather than get lost in the storm.

A positive consumer experience is about more than just super-fast delivery. It is about working with the consumer to ensure they receive their goods reliably and at a time that reflects their needs.

Essential to this is being transparent and accurate with delivery times. The sense of control given to a customer by sharing precise times for pick-up or home delivery and proactive warnings about delays creates a positive relationship between retailer and consumer.

Amazon has set the benchmark for expectations. Even though the company is not a direct market competitor for all retailers, the experience it offers has led to consumers expecting the same experience across all retailers, and responding negatively to those who fail to deliver these standards.

To meet this requirement, some retailers have started integrating the shipping data into their own systems. This can streamline the tracking process by reducing the need for multiple logins and simplify any returns processes by keeping it in-house. It also allows you to ask your consumers when they want their products and focus on meeting the individual needs and expectations of the customer.

Another area in which retailers need to invest in is warehouse efficiency. Current shipping models rely on just-in-time supply chains, which are subject to geo-political disruption and disruption from a lack of skilled workers in the shipping and HGV industries. However, many retailers are ill-equipped to evolve into new shipping models.

Limited warehouse infrastructure in the UK means that retailers cannot effectively move stock into the country ahead of time. Over the last decade, the scale of warehousing growth in the UK has been huge, but warehousing costs are around three times higher than they were ten years ago.

Bringing increased automation into these spaces, such as through warehouse robotics, has limited impact as the supply chain is still vulnerable to supply chain disruptors. To move forward, retailers must focus on building their real estate before investing in new technology.

Retailers must seize the opportunity to optimise their warehouse spaces. Click and collect services can be used to create local hubs, as retailers only need to transport goods to spaces, such as supermarkets, which are conveniently located near their endconsumers. Most supermarkets now offer this service as an alternative to home delivery, and the total market for click and collect is set to be valued at £9.8bn by 2023. The model is an easy way for retailers to save costs as they can use their in-store staff to sort orders and minimise the additional cost of delivering the items to the consumer. Other options include huband-spoke models, which use regional hubs and reduce your reliance on HGV drivers – currently in short supply –and utilise vans instead. These models can help retailers meet the customer expectation of order fulfilment without incurring a high cost.

Analysing your warehouse space can bring further benefits. Making a note of your warehouse space, production line speed, and system accuracy enables you to maximise efficiency and measure your warehouse’s spare capacity. If you find you have a significant amount of excess space, you can rent it out to other companies and bring in additional revenue.

Retailers need to work smarter, not harder. By making full use of all their infrastructures and existing metrics, retailers can provide goods quickly and reliably without incurring a considerable cost.

Martin Pateman-Lewis Engagement DirectorDigital

The current goal is to have those in non-financial roles produce reports with the same rigour as financial controls in the next three years; however, this may be unrealistic considering that financial reporting took significantly longer than a few years to get right. In order for organisations to achieve this goal they must assemble a cross-function team. Bringing teams together from both financial and non-financial roles enables organsiations to produce the best, most collaborative assurance and board-ready reporting that is investor grade.

Pressures are mounting from regulations like the Corporate Sustainability Reporting Directive (CSRD) to meet the growing demand from investors and other stakeholders to provide high quality, transparent, reliable and comparable reporting on climate and other environmental, social and governance (ESG) matters.

However, there seems to be a growing confidence crisis amongst UK organisations. A 2022 ESG survey research by Workiva, has revealed that nearly two-thirds (63%) of senior decision makers in the UK feel their organisations are underprepared to meet their ESG goals and regulatory reporting mandates. Despite the current lack of confidence in tackling these reports, there are significant positives to getting ESG reporting right - such as attracting investment and better alignment with customers, and other stakeholders.

Perfecting ESG reporting will not happen overnight but there is no better time than now to begin this journey. As such, this article will discuss the existing steps businesses can take to improve their confidence in the ESG data they report.

Despite evidence that over half of UK organisations (59%) are addressing the issue, having appointed an ESGspecific role to oversee reporting, 73% still do not have confidence in the data being reported to stakeholders. This may simply be down to time, as organisations have not been required to produce ESG reports long enough to have real confidence in their processes.

Meanwhile, among expectations that are concerning businesses are stakeholders who are calling for more detailed and uniform data related to ESG. Despite progress needed across all facets of ESG, tackling the environmental or ‘E’ element is clearly the current major focus.

Included in this data gathered, reporters are expected to calculate greenhouse gas emissions and provide carbon accounting details which are currently the areas that decision-makers are most concerned about reporting on. In fact, for almost half (43%), these were cited as priority concerns.

While identifying the areas where major focus is needed is evidence that businesses are taking steps in the right direction, being prepared does not stop there. Organisations also need to understand existing and upcoming regulatory demands and determine how these will impact ESG strategy.

The lack of preparedness by decision makers can be strongly tied to the lack of clarity around the future ESG expectations that might lie ahead.

In efforts to improve this issue, government and industry regulators are currently rolling out a range of regulatory reporting requirements to provide constant standards across the globe. These range from the recent Sustainable Finance Disclosure Regulation (SFDR) directive in Europe, to the ESG disclosure rule proposed by the SEC in the U.S. and the Singapore Exchange’s recommended 27 core ESG metrics. Meanwhile, the Task Force on Climate-Related Financial Disclosures (TCFD) has outlined the most effective principles for companies to analyse, understand and ultimately disclose climaterelated financial information.

Government regulators and internal policymakers are needed to communicate requirements clearly and work closely with reporting teams as well as their technology providers to ensure that these initiatives bring about the change they envision. Having the right controls in place ultimately makes processes more robust and repeatable, ensuring that the resulting metrics stand up to scrutiny. In particular this process applies to materiality assessments, which illustrate which ESG issues matter the most to an organisation’s stakeholders.

More regulatory requirements are still needed and these can come into place over time. As regulations, frameworks and stakeholders’ demands evolve, the key to maintaining confidence in reports will be to stay committed to regularly reassessing the processes organisations have in place. This will ensure they are equipped and ready to meet ever-evolving ESG standards.

Organisations are calling out for solutions to navigate the challenging ESG landscape. Meanwhile, financial reporting is in the middle of a digital revolution, focused on re-architecting and modernising systems. By taking lessons learned from finance and applying them to ESG reporting, businesses do not need to reinvent the wheel. Moreover, there are existing solutions that account for both financial and ESG reporting, which should encourage collaboration between the teams. The key outcome is to ultimately produce decision-useful data.

Desirable solutions should unite teams and workflows, and simplify the process of gathering data from across the organisation. Survey respondents also see these as being important for validating data for accuracy (80%) and mapping disclosures to regulations and framework standards (85%).

For example, automation is critical to ensuring consistently accurate results. Where data is input manually, the risk of calculation error is significant. Automating processes has been proven to remove additional steps that offer an invitation for human error. Where uniformity is needed across different reports and where data input is usually a repetitive task, automation offers a time efficient solution.

Similarly, through real-time collaboration, financial and nonfinancial reporters can ensure that when a data point is updated in one place, it is updated in every relevant analysis and report. Since data needs to be consistently merged in real-time to produce fully transparent, trustworthy ESG sustainability reports which can easily be integrated with financial data, there really is zero margin for error. Uniform, accurate reporting can be produced most effectively when combined with a platform that centralises related teams and integrates the full reporting process.

To navigate this era of change in ESG, organisations must be forwardlooking and flexible in their planning. Regulators, investors, customers, and other stakeholders have identified what’s essential in today’s reporting, but this is only part of what will be essential for tomorrow.

Looking ahead, organisations are planning to dedicate more resources to improving their ESG reporting, with the ‘E’ becoming more of a priority. This renewed focus will ultimately help drive tangible change to improve the business impact on the environment and society at large.

Technology which enables seamless integration between teams in one centralised platform will be key to streamlining the reporting process in the long term. This will also support in delivering transparent reports that are critical to meeting evolving demands as well as attracting investors and wider stakeholders. Ultimately, smart preparatory efforts that take advantage of innovation will enable organisations to feel more confident in their current reporting now and when facing future ESG mandates.

Mandi McReynolds Global Head of ESG Workiva

More than one third of the world’s population is Generation Z.

To give you an idea of what this means in figures, the UK has approximately 12.6 million (19%) Gen Zers entering the workforce, whilst the world’s eighth most populated country, Bangladesh, has well over 58 million Gen Zers – a staggering 35% of the population, around 27% of whom live in urban areas.

With larger numbers of young people entering the workforce at one time than any generation before it, what legacy will these digital natives leave on the banking sector?

Interestingly, wherever they are from, whether the UK or Bangladesh, Gen Zer’s have common behaviours and common challenges for the banking sector.

Every generation approach money and personal finance in a different way. Millennials discovered the road to adulthood was paved with financial difficulties including slow pay growth and uncertain economic conditions. This environment contributed to the development of the group’s spending patterns and views toward debt.

Millennials made their fair share of financial blunders along the way (as most generations do), but evidence is already accumulating suggesting the “next generation”, Gen Z, is already learning lessons from their elders. Some of Gen Zers’ older acquaintances struggled to reach high-paying professional roles while simultaneously taking on significant debt. As a result Gen Zers seem to be approaching personal finance with a level of caution.

Financial institutions offer services to customers of all ages, but many focus their marketing efforts on the youngest group, timed to coincide with the time when they complete college and begin to enter employment. Building a solid, enduring relationship with youthful customers can be profitable and result in many years of business. Many people stick with the same retail bank they joined as a college student for life. Institutions have the chance to develop and maintain its brand with each new generation whilst balancing the needs and wishes of older, existing customers.

Digital innovation and customer engagement is becoming fundamental to banks’ ability to differentiate themselves to customers. Gen Zers, as digital natives, demand different approaches. They are forcing the banking system to enter the innovation of technology.

There’s a proverb that says you can learn a lot about someone’s worldview by looking at how it was when they were in their twenties.

Few generations in recent times have experienced pandemics, transformational digital change, recessions, inflation, and global instability. Digital-first customers are no longer the future of banking but the present. Unlike millennials, who came of age during the 2008 global financial crisis, Gen Zwas expected to inherit a strong economy and record-low interest rates. The Covid crisis changed all of this.

Keeping Gen Zers motivated and interested in their financial futures will require creativity. Around 40% of Gen Zers use TikTok over Google for search. Fun and educational, video led, banks’ communication needs to ensure it reflects (and demonstrates an understanding of) the interests and concerns of this group.

In order to further promote economic accessibility, fintechs across the world are working to make credit inclusive, making way for the younger generations to be able to step out of the credit paradox and qualify for their first loan.

Gen Z has recently entered the banking industry, and they are upending it. The 2008 financial crisis impacted this generation’s parents, and they took lessons from it. Gen Z have a new relationship to credit. Despite having access to credit and the possibility of debt, Gen Z does not necessarily make use of it. Even though the majority of this generation has at least one loan account and is credit active, they handle their money wisely. The majority of Gen Zers who use credit are managing their debt better than Millennials did at the same age.

Gen Z are the obvious target for fast growing e-commerce brands. Gen Zers’ inspiration comes from aesthetic Pinterest boards, and TikTok highlights are used to capture their every move; therefore, it only makes sense that their methods of purchase are online first. And, e-commerce brands were quick to embrace fintech solutions for part payments or delayed payments. Such benefits previously were only limited to a smaller segment of customers having credit cards.

Historically, to be eligible for this credit customers had to earn the ‘right salary,’ with the right amount of transaction histories to be considered credit-able for the banks. Younger shoppers were almost always excluded from that group. The Klarna Generation have been granted access to credit in huge numbers. But, are these customers getting the ‘right’ credit? With little access to Gen Z to date, banks’ are missing out on the opportunity to service these customers.

And, with limited financial education, are Gen Z making the best financial decision for themselves? This is where next generation UK fintech, AGAM International, comes in. AGAM is the answer to the real-world financial problems faced by the unbanked community. It provides lenders with the information and access to those who have previously been denied a credit score. With the creation of a more sophisticated credit scoring method known as ‘Individual Independence Index’ individuals with limited credit histories, but who the data show are suitable borrowers, are able to receive access to loans – instilling a sense of financial confidence and security in many individuals without previous financial knowledge.

In order to further promote economic inclusivity, fintechs across the world are working to make credit accessible and it can only happen with digital innovation in every step of the way.

To remain in business, let alone thrive, financial institutions must embrace Gen Z’s digital native sensibilities and respond – and that means accelerating their digital transformation, adopting more sophisticated credit scoring and payment systems and communicating with Gen Zers in a language and format they understand.

Shabnam Wazed Founder and CEO

Shabnam Wazed Founder and CEO

A major part of effective Ecommerce marketing involves writing search engine optimized content, a job that can be rather tedious. It is no wonder some writers attempt to simplify the task using artificial intelligence (AI) generated content. However, this raises the concern of whether AI copywriting tools can actually develop helpful content that solves the consumer’s problem by providing the right answer to their search intent. Is their contribution to the web a net positive or a net negative?

AI content generators rely on pattern identification by crawling through billions of sentences online. The tools then use a transformer model to generate predictive text based on the learning samples; that’s where the major concern lies for critics of AI writing tools. This article will delve into the ethics and risks of using AI-generated content in Ecommerce marketing and how it could potentially be harmful for your brand in the future.

AI content generators rely on a set of inputs such as keywords or topic headlines to predict word by word entirely ‘new’ content. At the very core of the generator is a collection of machine learning algorithms which identify patterns in the human language. The language models rely on mathematical functions designed as neural networks similar to the way neurons in the brain are wired. The prediction is made by computing the strength of neural connections to reduce prediction error via parallel training. These models are pre-trained on billions of pages with all manners of content on the internet.

A large number of AI-content generators rely on the GPT-3 language model, which uses deep learning to create human-like text. The key phrase here being ‘human-like’. When it comes to predicting text, the model uses generative pre-training meaning its predictions are based on the patterns it learned from the training data. While the model may come up with uncanny and sometimes almost genius sentences, it's still based on statistics and not actual humanlevel intelligence.

Since AI content generators learn from both supervised and unsupervised sources, there’s the inherent risk that the model will be exposed to biased and toxic content. Keep in mind that the models cannot fully comprehend what the content they are trained on really means. Think of it as a big game of word association. Sooner or later, the algorithm will learn to associate certain words with similar ones as they appear more often in similar contexts in the training data.

While Ai writing tools can create well-structured content, there’s still the likelihood that they will spew hate speech amidst a normal sentence. Researchers attribute this to the presence of hate speech-related words in the training data, which leads the algorithm to form statistical relationships between phrases that it's trained on. Still, it doesn't fully understand the context or meaning behind them.

It goes without saying that if this kind of content is published without being thoroughly checked and edited by a human, it could have a real negative impact on any Ecommerce brand using AI to generate web content for the purpose of promoting their brand.

While most large language models train on billions of parameters in what is best described as brute force scale, there are still scenarios when their predictions do not make any sense at all. Professor Emily M Bender, A computational Linguist from the University of Washington, referred to these models as “stochastic parrots” owing to their echo chamber-like abilities to make ridiculous yet comprehensible statements. This is because the algorithms just introduce randomness to existing content in their predictions, so they retain the biases in the training data.

When you prompt a writing tool to generate text on a topic that's not very common on the internet, chances are that the model will have even fewer data to learn from. This affects the varying quality of the results, and often, the generated text will contain placeholder text that has nothing to do with the topic at hand. The predictions may also contain statements that are not fluent and the paragraphs lacking in the flow of ideas.

In a recent blog post, Google stated that its upcoming update will focus on helpful content in an effort to fix the loopholes that websites have been using to gamify the ranking system. The fix involves changes in the search engine's ranking signals to rank content worthiness. It's expected that the update will change how the algorithms evaluate a website’s content and how it's helpful to satisfy the searcher’s intent.

With this update, Google will give top priority to people-first content so that quality evaluation will be paramount. This is bound to negatively impact websites with AI-generated content that doesn't clearly demonstrate the depth of knowledge and expertise of the topics covered. While the new signal is automated based on machine-learning models, it will not mark content as spam or issue a manual action. Instead, Google's ranking algorithm will consider the signal while ranking websites in search engine results pages (SERPs). If you are looking to rank higher, it's high time you got rid of unhelpful content, especially if you use extensive automation to write your content on many topics.

Ryan Turner, founder of Ecommerce marketing agency EcommerceIntelligence.com, said the following when asked about the trend of Ecommerce businesses using AI to make content marketing production faster and cheaper: “It is something we’re wary of for sure. Many brands we speak with have ambitious content publishing goals which are potentially focused too much on quantity instead of quality. We haven’t seen search engines take any kind of definitive action against AI content yet, but it is something many in the industry feel will happen at some point in the near future.”

Ai writing tools are bound to repeat inaccurate information that already exists in the training data. In this case, the tools generate inaccurate information without the intention of causing harm in what is commonly referred to as misinformation. However, as AI tools advance in complexity, there’s fear that they may start deliberately generating false information, a common disinformation tactic. This is often the case with AI tools that write news articles that can dupe human readers.

In an effort to stay competitive with larger brands in their market, some Ecommerce marketers publish AIgenerated articles without much human proofreading and editing of the content. This mass publication of AI-generated content is more likely to spread disinformation by repeating existing malicious information in a never-ending cycle. Some researchers have estimated that 99% of the internet will be based on AI-generated content by 2025 if we continue at the current rate of adoption, raising concerns on just how accurate all that information will be.

There’s no denying the fact that artificial intelligence is here to stay. While AI writing tools have experienced drastic improvement over the last couple of years, there still exists some serious ethical and operational risks associated with publishing AI-generated contentparticularly if it is online representing a premium brand. AI writing tools can be used to help generate article and blog post ideas and headlines, as well as the overall structure of the piece. However, it might be a good idea to rely on real humans to do most of the actual writing.

Ryan Turner Founder EcommerceIntelligence.com

As we find ourselves living in a world of ever-changing global challenges, the future of banking over the next 10 years will no doubt look very different from today.

With banking apps increasingly taking the place of in-person visits to the local branch, personal devices such as smartphones will greatly shape the way consumers manage their money. Bank cards will be a thing of the past, making the smartphone a major player in how consumers interact with financial goods and services.

Handling cash, once a defining feature of banking, will also be phased out. All, if not, most, money will be digital. According to UK Finance, only 17% of all payments made in the UK were cash payments. That figure is expected to decline further over the next decade, which leaves ample room for digital payments to take precedence over all other forms of payment.

In tandem with this, the next 10 years of banking will likely do away with all finance hardware. Banking activities, from payments to savings, will be conducted online using software and will be further optimised to enhance the customer experience.

Moving away from legacy banking systems will create an increased appetite for frictionless and more personalised banking. Consumers do not want to wait for payments to clear or get generic service offerings that do not suit their needs. All financial services will need to be fast but tailored, otherwise consumers will vote with their feet and will take their money with them.

As such, the future of banking looks to be one of complete ease and inclusivity, without the need for consumers to meet specific criteria all the time. Sending money to friends, recuperating group expenses or even just splitting a bill will become the norm as peer to peer payments will be seamless regardless of where they bank.

Another change to look out for will be the fight for consumer retention and engagement. Established banks have long enjoyed consumers flocking to their services, but now challenger banks such as Monzo and Revolut have given consumers greater financial choice. This will mean increased competition between banks and generous reward systems to ensure customer loyalty.

Over the next decade, we will also likely see more regulated ‘buy now, pay later’ services and should expect to enjoy greater flexibility that suits every day life in our banking experiences.

With severe disruptions to their education and entry into the workforce, Gen Z are arguably the most economically fragile compared with previous generations. Gen Z will need banks who will cater to their unique pain points as they face their first recession.

Gen Z desires banks that won’t penalise them for their lack of financial knowledge or stability. They want banks that are sympathetic to their financial and personal goals. A bank to this generation will not just be where they store their first paycheck, but will be their own personalised financial guide.

We will see the banking sector face an increased push for innovation and this generation will be quick to give their feedback. Banks behind on innovation will lose out on having Gen Z customers and will struggle to entice them away from competitors.

This generation wants to know; will you make a decision on what I can do today, tomorrow and not my past?

As they face the most financially challenging times in recent history, Gen Z will turn to services that will make their financial lives easier. Gen Z wants to save whilst they spend; looking to services, such as cashback offerings, that will not require them to greatly alter their consumer habits. Gen Z needs to navigate the cost-ofliving crisis but not at the expense of their wellbeing.

As time goes on, we will see a bold shift away from legacy banking processes to new hyper-personalised experiences. Fintech innovation is already improving business to consumer (B2C) and consumer to consumer (C2C) payments, boosting the financial economy - we can expect this trend to continue.

As digital natives, Gen Z are tech savvy enough to adapt to the changes we foresee over the next 10 years. They will take full advantage of opportunities to make and save extra money using technology and social media content.

Our personal mobile devices will take on an even greater role in our everyday life and will determine our engagement with financial services. As a result, we know that the next 10 years in banking will be greatly shaped by technological innovation and exciting developments in the world of finance. Watch this space.

Tariq Zaid CEO and Co-founder Cheddar

Tariq Zaid CEO and Co-founder Cheddar

Allianz Trade, formerly Euler Hermes and part of the Allianz Group, is international world leader in trade credit insurance (TCI). Its product offering also includes surety bonds, guarantees and business fraud insurance. Since 1910, Allianz Group has had a presence in the Asia Pacific region, where it currently serves 21 million customers. Wanda Rich, editor of Global Banking & Finance Review, interviewed Paul Flanagan, Regional CEO of Allianz Trade in Asia Pacific, when he gave the lowdown on Allianz Trade’s Go2025 strategic plan.

“APAC is a growth region, and our strategy is all about growth,” he began. “It focuses on three pillars.

The first is to extend core business; we want to expand our leadership position in our TCI core business across all geographies. We will do this by being a strong and consistent partner for our customers, particularly now as we enter uncertain economic conditions. Our clients value our financial strength, our global footprint and the level of support provided by the local teams in over 50 countries. We are constantly working to improve our communication to our clients and the market and to refine our strong level of service to our customers.”

“When it comes to growth, we have a unique multi-channel distribution model based on strong relations with brokers, internal sales teams and increasingly, online,” he continued.

“We will continue to extend our core business with banks and, following our recent rebranding, the Allianz network. In addition, as trade is increasingly done online, we have developed products that support our customers in making that transition.”

The second, Paul reported, is about boosting growth via scalable engines.

“While we are already a recognised expert in the surety business, we also have other specialty products such as Specialty Credit and Excess of Loss. The surety market is twice the size of TCI and growing twice as fast. We look to drive surety to the next level through our investment in people, refining our underwriting framework and expanding our product offering.

Meanwhile, Asia Pacific and the US will continue to serve as our growth engines in the TCI business as well.”

The third focuses on exploring the new world of trade, and seizing the opportunity given by the online shift of B2B trade by becoming a key player in this ecosystem.

“We will do this by developing specific products that support the market, such as e-commerce sales and Buy-NowPay-Later (BNPL) business,” Paul said.

“We will capitalise on our strong value proposition as a global credit insurer, our financial strength, proven credit expertise and worldwide collection network. The development of our API offerings is opening up many opportunities for growth and, already, APIs support a significant proportion of our revenue stream.”

He described the aforementioned rebranding from Euler Hermes to Allianz Trade as “significant, but also a natural move for us.” Euler Hermes was a brand full of history and it has existed, in one form or another, for over 120 years. “Of course, in the TCI space, Euler Hermes was a strong brand, especially in Europe. The Allianz brand is the number one global insurance brand and adopting that brand is a game-changer for us. As Euler Hermes had been wholly owned by Allianz since 2018, it was a natural decision to rebrand and carry the Allianz brand.”

“The trusted Allianz brand will open new markets and new segments for us, from multinationals to SMEs, as well as new distribution channels, starting with the Allianz distribution networks. There will be more opportunities for collaboration and knowledge sharing and also for building common technology assets, to better accompany the changes happening in online trade. Rebranding to Allianz is a win-win scenario.”

Paul also spoke on the current trends being witnessed in the APAC trade credit markets in terms of trade flows and volumes. “The inflation increase resulting from the COVID-19 pandemic and geopolitical tensions in Europe and Asia, as well as demand for normalisation, have resulted in a challenging and volatile business environment,” he said. “The actions taken by central banks to curb inflation will have a significant impact on the global economy in the coming months. The increase in debt servicing costs, currency devaluation and slowing consumer demand will put pressure on all business and will increase the risk of payment default.”

A slowdown in trade flows has already been seen between APAC, the US and Europe caused by the slowdown in the respective economies. “Intra-regional trade is showing more resilience but this may change if the global economy slows further,” Paul told Wanda. “During the pandemic, we saw a significant reduction in insolvencies due to government support and monetary policies. With global insolvencies expected to increase by 10% this year and 19% next year, we are seeing many enquiries for trade credit insurance across Asia Pacific, especially from companies who are looking to expand to new markets or customers.”

He acknowledges that today’s climate of uncertainty makes it even more important to protect business growth and cash flow against late payment or insolvencies. “At Allianz Trade, our team of experts brings together local expertise and global reach for companies to help us make fast, informed risk decisions that meet globally coordinated compliance standards and optimise trade risk management.”

Next, Paul discussed the recent announcement of Allianz Trade’s collaboration to develop a BNPL solution for the B2B space. “Allianz Trade is uniquely positioned to grasp this new business opportunity leveraging on our assets and our first mover advantage,” he said. “B2B e-commerce is projected to grow at 17% CAGR until 2027, with market size reaching EUR21 trillion. While 95% of businesses prefer paying on

credit terms, just as they are able to when buying offline, less than 10% of e-merchants offer such an option.”

This scenario can often lead to B2B customers abandoning their baskets, hence a sales opportunity is wasted. This, Paul explained, is where BNPL comes into play. “BNPL refers to shortterm financing that allows buyers to make online purchases and pay for them at a later stage. By offering payment terms, sellers can increase their customers’ average shopping baskets and improve conversion rates. It is a real competitive advantage and builds customer loyalty.

“Our strategy is two-fold. First, we look to directly address large merchants and give them the ability to offer credit terms to online customers. In addition, we are able to support businesses providing BNPL services to sellers who want to offer BNPL

terms. Our strategy is to offer a bundled product, partnering with fraud specialists and banks, and offer it to both traditional sellers and platforms.

“Our e-commerce product allows our customers to offer deferred payment terms to their buyers with complete peace of mind, confident that the transactions are secured. With e-commerce credit insurance from Allianz Trade and via API integration, sellers can safely and automatically propose payment terms to their customers in real time.”

“Finally, the execution of our strategy depends on our teams who will deliver it and who have direct contact with our customers. We will continue to invest as we grow, not only in additional resources, but in our existing teams in terms of personal development and training to keep pace with a fast-changing business environment,” Paul concluded.

Over the last few years, the banking sector has faced severe disruption which has dramatically accelerated digital transformation across the banking sector. Catalysed by the Covid-19 pandemic, the transformation has irreversibly changed banking as we know it.

Previously, banks would attract new customers through their various offerings and services and people physically going into their local bank branch. However, when it comes to customer expectations, in-person interactions have fallen to the bottom of list, especially for simple or recurrent transactions and interactions. Most customers now expect and prefer the convenience of being able to carry out these kinds of transactions using online banking and mobile banking solutions.

The surge in demand for digital banking services has levelled the playing field for financial services providers. With the sharp rise of digital banks and legacy banks transforming their products and services, customers are now spoilt for choice when it comes to how and who they choose to bank with. Consequently, identifying differentiators between banks and fintechs is becoming increasingly difficult in an already saturated industry. What’s more, economic uncertainty is set to limit attractive interest rates set by lenders, so there isn’t much financial services providers can do to remain competitive. As a result, greater emphasis has been put on customer experience (CX), as providers try to strike the balance between attracting new customers and ensuring existing customers stay with them.

The impact of the pandemic alongside the recent explosion of fintech brands, has brought the value of high-quality digital interactions to the forefront. So, how can banks make CX their strongest asset?

According to Insider Intelligence’s Mobile Banking Competitive Edge Study, 89% of consumers said they use mobile banking, rising to 97% of millennials. These users don’t leave their bank for fees. Instead, they’re most likely to leave because of dissatisfaction around mobile banking capabilities (43%), online banking capabilities (35%) and customer service (33%).

In addition, 75% of respondents to the 2022 World Retail Banking Report said they are attracted to new agile competitors as they offer fast, easyto-use products and experiences that are readily available while remaining low in cost.

With in-person interactions playing a much smaller role in banking, CX is one of the main ways that banks can ensure they stand out from the crowd. Customers still want to be understood, respected, appreciated, and valued – they want to maintain the human connection that was traditionally established through in-person interactions. The key is learning how to offer this through digital channels.

Most customers prefer digital interactions over physical or phone conversations, the delivery of these interactions is the main differentiator. They must be delivered in a way that’s both transactional and emotional, demonstrating to customers that their bank genuinely wants to help them achieve their financial goals.

This will bolster consumer confidence and loyalty. Although the journey towards customer-centricity doesn’t happen overnight, banks that invest in good CX have higher rates of recommendation, greater wallet share, and are more likely to up-sell or cross-sell products and services to existing customers.

Ultimately, customers have increasingly high expectations and are demanding more from their banking experiences. The onus is therefore on banks to rethink their business models and focus on providing an overwhelmingly easy, convenient, and distinctive CX. The key to success lies in understanding customer needs, and then fulfilling those needs in a way that no other brand can.

Financial services customers are generally looking for four things: help in maximising the benefits of existing products, relevant product offers at the right time, personal knowledge of things they care about, and customised product features. Therefore, banks strengthen their customer knowledge so they can serve customers holistically.

The starting point is to establish a CX vision. This will help shape business goals and connect them to key experiences that will distinguish the brand and ensure customer loyalty. For example, this could include defining how certain features will work, identifying the right training for employees, or structuring CX teams in a certain way.

Once the CX vision has been defined, banks should then set up an analytics framework to measure their progress. Any effective analytics framework will have highly defined KPIs, data sourcing and reporting – along with market analysts who can generate and interpret insights that will enable real-time customer guidance and help banks track their success.

The final step is workforce transformation, which should be addressed from an operational and cultural perspective. Operational in terms of defining ways of working, organisational and process improvements, and access to applications for employees to work more effectively. Cultural in terms of identifying skills gaps and building a culture that encourages employees to adopt new technologies and a customer-centric mindset.

These steps will help banks to identify any gaps, as well as the opportunities to introduce consistent, crossfunctional omnichannel experiences.

They can also look to banks that have successfully transformed their CX for inspiration. For example, Scotiabank rolled out a global AI platform called C.MEE, which analyses data across all customer touchpoints to deliver personalised and relevant banking experiences. Additionally, Capital One significantly increased its CX investment after identifying that 47% of its customers are early adopters of technology and 88% regularly use their smartphone for banking interactions.

Digital banking is prevalent in today’s society and it will continue to shape the industry for years to come. CX is now a clearer differentiator than price or products, so there is more pressure on banks to deliver on this front. With consumers facing more choice than ever before, banks must lay the groundwork to provide unbeatable customer experiences. Failure to do so could be detrimental to their ability to maintain existing customers as well as attracting new ones, so banks must prioritise CX and ensure they’re meeting customer expectations.

The finance sector is a lucrative target for cyber criminals. Attacking fintech organisations offers numerous avenues for profit through theft, fraud, and extortion, while nationstate-backed groups are increasingly targeting the sector for political and ideological leverage.

As such, the heat is rising for businesses. The Financial Conduct Authority (FCA) recently revealed that malicious attacks targeting financial websites and servers increased fivefold in 2022, with a quarter of all incidents involving distributed denial-of-service (DDoS) attacks. To add fuel to the fire, 81% of cyber leaders in the finance sector have reported a rise in attacks since the start of the Russia-Ukraine war, according to research by Bridewell.

As the finance sector continues to undergo major digital and infrastructure transformation, it is more important than ever for businesses to reconsider their cyber security investments. Organisations should seize the opportunity to adopt a proactive approach to security operations and implement a robust cyber security transformation process, so that they can continue to improve services whilst minimising cost and risk.

No other sector is more data-driven, digitised, or more attractive to cyber criminals than the finance sector. As both a vital component of the UK’s critical national infrastructure (CNI) and a treasure trove of sensitive data and financial capital, the industry continues to be targeted by hackers around the world. And these criminals are becoming ever more sophisticated in finding and targeting weak points across the finance community.

For fintechs in particular, the threat landscape is evolving in line with technological advancements, with cyber criminals leveraging insecurities in cloud configurations for easier access to sensitive personal data and valuable corporate intellectual property. For example, ransomware has rapidly evolved from being a malware issue to a highly profitable and nuanced human endeavour. Different from traditional commodity ransomware attacks, humanoperated ransomware (HoR) sees criminals with high levels of offensive security knowledge gaining access to organisations and surveying the environment for extended periods of time, before launching devasting attacks on data and systems.

Even the big players in fintech can fall prey to sophisticated and multi-layered ransomware. In 2020, the world’s third largest financial services software provider, Finastra, was hit by a ransomware attack that caused disruption to its global operations and interrupted services for its 9,000-strong customer base. Fortunately, customer and employee data remained untouched in this instance – but attacks like these can have cascading negative impacts, including a broader loss of consumer confidence.

When escalating geopolitical tensions are added to the mix, the stakes for financial organisations are even higher. Bridewell’s recent survey of cyber leaders in CNI found that over three-quarters (76%) of IT decision makers in the finance sector are worried about the impact of cyber warfare. Following the recent rise in cyber attacks in the wake of the Russian invasion of Ukraine, the

need for organisations to collaborate more effectively and mount a proactive response to evolving security risks could not be clearer.

Today, fintech organisations must protect themselves against a diverse and escalating range of threats. As cyber crime rapidly displaces conventional crime in both volume and sophistication, it is important for all business leaders to be able to define and truly understand the specific threats facing their organisation. This understanding should encompass all potential adversaries, motivations, and tactics. By asking themselves some challenging questions, fintechs can gain a crucial head start in defining clear security objectives and adjusting their cyber strategy accordingly.

Traditionally, many senior managers in finance have considered digital transformation and cyber security to be two separate strategies with independent objectives and goals. This approach is fundamentally flawed, as it causes organisations to overlook the security weaknesses and system vulnerabilities that come with rapid technological change.

As ever, criminal groups are poised to take advantage of any business that quickly deploys new tools or completes fast upgrades without properly securing systems and defences first.

Instead, cyber and digital security strategies should be thought of as inseparable, enabling organisations

to plan and integrate both into their transformation projects from the very beginning. Financial organisations are already making good progress in this area. Bridewell’s research found that, for many cyber leads in finance, the source of greatest pressure to improve cyber maturity came from the business itself and the need to support new technology and digital initiatives. This suggests that organisations are taking steps to ensure they have a strong cyber security strategy that matches their digital transformation strategy.

For financial organisations, the next step towards cyber maturity and resilience involves shifting mindsets from reactive – based on meeting minimum compliance – to proactive. This change of stance is key to staying one step ahead of cyber criminals.

While legislation like the NIS Regulations has undoubtedly helped improve security within finance, it is important that business leaders do

not use regulation as a primary driver for cyber security improvements. Nor should they simply build cyber security walls higher and only respond to breaches after they occur. To become truly mature in the face of threats from all angles, fintech organisations should embrace an integrated, well-considered, and proactive strategy centred around intelligence-driven managed detection and response (MDR).

An effective MDR strategy consists of threat intelligence, threat hunting and penetration testing, along with deployment and management of security monitoring and incident response. By blending artificial intelligence (AI), automation, and human analysis, MDR provides enhanced visibility over networks and systems, enabling organisations to detect and prevent both internal and external attacks. This holistic view of cyber security allows organisations to gain full visibility across people, skills, and technologies as well as processes, driving far-reaching improvements to their overall cyber posture.

Innovation is the lifeblood of any successful fintech, so no organisation should be afraid to transform. The good news is that the jump to cloud and modern technologies needn’t come at the expense of cyber security.

More and more organisations in the finance sector are realising how cyber security can drive both digital transformation and business transformation, rather than holding them back. As such, a golden opportunity exists for fintech’s to align their cyber and digital security strategies from the outset. By ensuring that security is weaved into their DNA, organisations can implement a proactive cyber posture to keep critical services running whilst building a wider culture of security.

Like many industries, banking can be demanding. Long hours, a competitive landscape, and rapid decision-making make it a challenging, but also a highly rewarding, career path. However, in an age where businesses are in a race for competitiveness to retain talent, organisations within the industry need to look at how they can best respond to a rapidly changing landscape.

The industry is incredibly broad. Encompassing, but not limited to, legacy banks, building societies, challenger and even retail banks, the sheer variety of challenges within these different settings is vast. There is common ground however, with one particular challenge plaguing each of these organisations; the high volume of repetitive tasks workers must complete on a daily basis.

Whether it’s loan processing, account closures, anti-money laundering, or even accounts payable, organisations need to look at innovative ways to reduce the repetitive, data-intensive tasks which are still being carried out by staff. This requires an adaptable technological solution which can free up worker time and improve their dayto-day roles, and that is exactly where software automation comes in.

Software automation isn’t a new solution to the banking industry. In fact, it is already in many banking organisations worldwide, working behind the scenes to improve customer service and increase operational efficiency. But, many are overlooking its potential to help support and nurture their employees even further.

It’s important to note that software automation isn’t a replacement for human teams, rather an accessory for them. By emulating human workers on the software they use within their jobs – such as ERP systems and MS Office – via a front-end interface, automation can perform rule-based, tasks, taking these repetitive and tedious tasks away from workers.

Interestingly, a staggering 43% of all work in financial services has the potential to be automated, which would give back vital time to employees, helping them avoid burnout, become more productive and, hopefully, happier in their roles.

There are many strings to the automation bow. An inherently customisable solution, it provides real potential for every team and can empower individual needs. For example, we are currently seeing significant use of automation at the back end, such as reconciliation and updating general ledgers, however, it can be especially empowering for customer-facing employees in call centres and retail branches also.

It's undeniable how important human empathy is within customer interaction. When it comes to finances, customer-facing teams often have to deal with emotional and serious situations. In these cases, it is important employees can engage with the customer, create a rapport and have the right information on hand to swiftly solve issues. Having to sort through multiple siloed and legacy systems to find a solution is not only tedious but can result

in poor customer service. Having a solution – such as automation – in place which can source masses of data within a few keystrokes can speed these interactions up and provide an overall better experience for both the customer and, just as vitally, the employee.

Expanding the use of automation to every area of the organisation is important in helping all employees feel equally supported and satisfied in their work. Personalised robot assistants are another way in which automation can assist, ensuring each team feels encouraged to put their energy into the heart of the job and can focus on what they want to be doing, rather than simply getting through admin work. KYC checking, client onboarding, replying to emails requesting information, and many more time-consuming tasks can easily be automated.

With hundreds of IT systems in play at once, banks generally can’t afford to carry on the way they are – reliant on legacy IT systems which often aren’t compatible. This current setup creates a lot of repetitive work involving moving, transforming, and validating data, and often leads to attrition and frustration within teams.

Traditionally, there has been a widespread fear that automation will replace a large number of jobs, but this couldn’t be further from the case. In fact, automation is at its best when used to complement human workers and their skills, while also providing them the freedom and time to upskill and reskill in areas that can truly impact business growth.

Simply put, automation creates additional capacity for banks to further develop the skillset of their staff. This, in turn, boosts employee satisfaction and enables financial organisations to retain highly skilled talent while automation meets demands in other areas.

Due to the digital and rules-based nature of the tasks performed by bank workers, automation has presented a great opportunity for financial organisations to modernise their services into the digital age. In the industry, automation is already performing tedious work of thousands of people in many banks and expanding its use will be key for improving the employee experience and talent retention.

The simplicity of automation adds to its appeal. It is possible for one person to automate a simple process in as little as a few days, making it a disruptive delivery solution with transformative ROI and time to value.

Financial service organisations need to jump on this opportunity as a way to boost employee satisfaction sooner rather than later. By giving back precious time once spent on time consuming, data-heavy processes, employers can have a tangible impact on the employee experience and significantly improve the level of engagement of workers.

Keelan Singh Industry Practice Director UiPath

Often fascinating and counterintuitive, historical data of consumer sentiment can powerfully foreshadow market behavior and its impact on investment market performance.

As fear of recession rises, a review of consumer behavior during recessions of the past gives us a pretty good idea of how financial institutions and markets may fare during the coming year.

For example, concern about an uncertain future typically motivates consumers to hold on to cash assets and take refuge in safe investments.

For financial institutions during the pandemic, this has meant soaring deposits as consumers sought security in saving against the potential for unexpected financial hardships that could arise from this unprecedented (in our lifetime) global occurrence.

At the same time, interest rates remained low throughout the pandemic, until recent hikes by the European Central Bank and the U.S. Federal Reserve. This has meant that financial institutions are beginning to enjoy a wider spread between what they pay on deposits and what they make on the loans that they underwrite.

Now that interest rates and the Consumer Price Index (CPI) are on the rise, will consumer behavior follow the same pattern as it has in the past?

Interestingly, the answer may be “no.” Usually when interest rates are high, deposits decline as people look for higher yields through stocks or other investment options. However, because the Central Bank and the Fed are trying to cool the economy to bring inflation down, prompting fears of recession, and people are nervous.

It's entirely possible that people will stick with the safety of their FDIC-insured or European Banking Authority-insured bank deposits rather than take the risk of betting on a potentially higher yield, simply because they’re scared of a recession. Consumers may be seeking a return of their savings more than a return on their savings.

This will be a particular challenge for people in or nearing retirement, who will be hit particularly hard by inflation. They’ll be looking for strategies to protect their savings and investments while covering increased costs caused by inflation.

An unfortunate and truly unprecedented market anomaly is complicating matters for them, however: both stocks and bonds have declined simultaneously. Usually, when one goes down, the other goes up. So, this is really disorienting for a lot of people who would normally be shifting from more stock-heavy portfolios to more bond-heavy portfolios.

Fortunately, there are strategies for mitigating the risks of inflation, such as low-risk government-issued I bonds that currently offer a yield in the 9% range (but investment amounts are limited), Treasury

Inflation-Protected Securities (TIPS) that increase or decrease with changes in unexpected inflation, or inflation swaps that can be easily accessed in a mutual fund format.

Of course, another tactic is to invest in shorter-term bonds so that every year or two you can reinvest maturing bonds at a potentially higher rates.

As with any investment, the key is balance. There can be a cost to protecting against inflation.

For example, a two-year treasury bond may have a 4% yield today. If you buy a two-year TIPS bond, which has inflation protection built into it, you’ll get a lower yield. Accepting the lower yield is the price investors pay for protection from unexpected inflation. But if inflation is lower than expected, you would've been better off getting the 2-year treasury without inflation-protection at 4%.

The best inflation hedge over time is stocks.

For people who are still saving toward retirement, the decline in the stock market can be viewed as good news: stock prices just got a lot cheaper than they were at the beginning of the year.

The paradox is that the time for strong value creation is when things feel the worst. Existing value is going down now, but that gives us the opportunity to buy at a tremendous discounts with the expectation that we’ll see a rebound in returns in a year or two.

There’s nothing to indicate that we should be expecting an economic downturn that is greater than what the market has already priced. But, in this time of unprecedented occurrences, if the economy sinks further than expected, it’s good to remember that for disciplined investors it can represent another opportunity for buying stock at a discount.

Month-to-month inflation data during a time of market volatility will always generate a lot of noise, with analysts and traders interpreting the meaning of each single inflation reading.

But when we look back five years from now, we’re unlikely to remember what inflation did in September of 2022. We will be talking about the overall trajectory and, perhaps most importantly, the Fed’s determination of the “neutral rate,” which is the rate that provides the optimal balance between price stability (inflation) and full employment.

It’s important to remember that while monetary policy can affect the demand side of the inflation equation, it has relatively little effect on the supply side. Improvement or deterioration of supply conditions will have a material impact on both the trajectory of inflation and the final destination (or “neutral rate”). There are good reasons to expect some improvement to supply as China’s zero COVID policies ease and Europe adjusts to the ongoing war in Ukraine.

There is an old saying: “If you don’t know your tolerance for risk, the market will teach it to you.” I would like to suggest modified version of this: if you don’t know the benefit of diversification, the market will teach you.

Periodically, markets recalibrate. It’s a healthy process, akin to periodic forest fires clearing underbrush and preventing the kind of devastating wildfires that come with excess fuel. The current environment is a healthy recalibration of markets, and those with diversified portfolios are weathering the volatility well.

It’s even important to diversify your diversifiers. Some investments just feel safe. Gold is a good example. At the risk of raising the ire of investors who favor gold, this is what we call “imperfect hedge.”

There’s a saying about gold, for instance, that you could buy a decent suit for an ounce of gold in the 1800s, and you can still buy a decent suit for an

ounce of gold in the 2000s. If you had invested the same amount of money in stocks over that same time period, you could buy many more suits with the resulting performance above inflation.

There’s certainly nothing wrong with gold or other securities that offer a measure of inflation protection, but there is a risk during volatile periods that investors will abandon diversification for assets they perceive as “safer.”

Building a resilient, diversified portfolio begins with a clear assessment of the risks that need to be managed. Remember that inflation, for example, isn’t the same for everyone. If you commute, you’ll feel rising gas prices more. If you’re a vegetarian, you may not feel as much pain at the checkout counter as other consumers when meat prices go up.