Being data-driven is complicated. We can help. VOL. 35 • NO. 12 • DECEMBER 2022 THE AUTHORITY FOR THE DATA-DRIVEN BUSINESS PM40050803 ❱ 7 Does Direct Mail Work Anymore? (Yup.) ❱ 18 Dr. Doug Norris Examines Latest Census Data Release Interview: of Scene+ Matthew Seagrim The Future of Loyalty

SECNE+

COURTESY

We’ll Help You Keep It Clean

Melissa.com 800.MELISSA (635-4772) Trust the Address Experts to deliver high-quality address veri cation, identity resolution, and data hygiene solutions.

Dealing with bad data is a task no marketer needs on their checklist. Inaccurate, outdated, and duplicate records can build up in your database, affecting business decisions, the customer experience, and your bottom line.

Address Experts, Melissa helps our customers improve their direct marketing efforts with the best Address Veri cation, Identity Veri cation and Data Enrichment solutions available. We validated 30

records

which is why thousands of businesses worldwide have trusted us

their data quality

Contact us for a Free Proof of Concept and ask about our 120-day ROI Guarantee. BAD DATA BUILDUP Missed Opportunities Returned Mail & Packages Decreased Customer Insight Real-time Address Veri cation Change of Address/NCOA Processing Geographic & Demographic Data Appends DATA CLEANLINESS

As the

billion

last year alone,

with

needs for 37+ years.

PRESIDENT Publisher & Editor-in-Chief

Steve Lloyd - steve@dmn.ca

DESIGN / PRODUCTION

Jennifer O’Neill - jennifer@dmn.ca

ADVERTISING SALES

Steve Lloyd - steve@dmn.ca

CONTRIBUTING WRITERS

Fiona Roach Canning

Andrew Eppich

LLOYDMEDIA

Doug Norris Billy Sharma Stephen Shaw

Phone: 905.201.6600 Fax: 905.201.6601 • Toll-free: 800.668.1838 home @dmn.ca • www.dmn.ca

EDITORIAL CONTACT:

DM Magazine is published monthly by Lloydmedia Inc. DM Magazine may be obtained through paid subscription. Rates: Canada 1 year (12 issues $48) 2 years (24 issues $70) U.S. 1 year (12 issues $60) 2 years (24 issues $100)

DM Magazine is an independently-produced publication not affiliated in any way with any association or organized group nor with any publication produced either in Canada or the United States. Unsolicited manuscripts are welcome. However unused manuscripts will not be returned unless accompanied by sufficient postage.

POSTMASTER: Please

send

// 3 DECEMBER 2022 DMN.CA ❰ Vol. 35 | No. 12 | December 2022

Todd Hoover INC. HEAD OFFICE / SUBSCRIPTIONS / PRODUCTION:

302-137 Main Street North Markham ON L3P 1Y2

all address changes and return

undeliverable copies

Canada Post Canadian Publications Mail Sales Product Agreement No. 40050803 Twitter: @DMNewsCanada MARKET TRENDS TRADITIONAL DM NEXT ISSUE: The Customer View of Fulfillment and Delivery PLUS: A Special Awards Wrap Up FINANCE DATA INSIGHTS ❯ 7 Does Direct Mail Work Anymore? ❯ 9 The Growth of the EcosystemConnected Business ❯ 17 Customer Growth: 7 Ways for Financial Service Firms to Drive Growth LOGISTICS ❯ 4 Talking Points talkingpoints ON THE COVER ❯ 18 Census 2021: Rising Education Levels and Labour Force Activity Changes FINANCE DATA ❯ 20 Sustainable Digital Infrastructure: Modernizing Financial Institutions ❯ 22 In the Race for Customer Primacy it’s Time for Traditional Banks to Win INTERVIEW ❯ 10 Loyalty 2.0: An Interview with Matthew Seagrim, Senior Vice President, Scene+ ISTOCK/ BUTENKOW ISTOCK/ SURASAK SUWANMAKE COURTESY SECNE+

Occasionally DM Magazine provides its subscriber mailing list to other companies whose product or service may be of value to readers. If you do not want to receive information this way simply send your subscriber mailing label with this notice to: Lloydmedia Inc. 302-137 Main Street North Markham ON L3P 1Y2 Canada.

all

to: Lloydmedia Inc. 302-137 Main Street North Markham ON L3P 1Y2 Canada

talkingpoints

New Research: Insights into How Companies Can Anticipate Supply Chain Disruptions.

Research from York University’s Schulich School of Business shows how companies can anticipate – and prepare for – supply chain disruptions.

The findings are contained in the paper “The effects of tie strength and data integration with supply base on supply disruption ambiguity and its impact on inventory turnover,” which was published in the International Journal of Operations and Production Management. The paper was co-authored by M. Johnny Rungtusanatham, Canada Research Chair in Supply Chain Management and Professor of Operations Management & Information Systems at the Schulich School of Business; Rahul Pandey, Assistant Professor of Supply Chain Management at the University of Memphis; and Dipanjan Chatterjee, Associate Professor of Information Systems at Goodman School of Business, Brock University.

They introduce the concept of “Supply Disruption Ambiguity”, which the researchers describe as the inability of a sourcing firm to attach probability point estimates to the occurrence of supply disruptions and the magnitude of loss from those disruptions. The researchers analyzed survey data from 171 North American manufacturers and archival data for a subset of 88 publicly listed manufacturers.

The researchers found that strong supply base ties decrease Supply Disruption Ambiguity, which, in turn, increases inventory turnover. Moreover, strong supply base ties and data integration with the supply base have positive effects on inventory turnover. As sourcing firms strengthen ties and integrate data exchange with their supply base, their inventory turnover improves from access to information that allows them to effectively detect and diagnose supply disruptions.

“Research on supply disruption management has paid more attention to the ‘disruption recovery’ stage than to the ‘disruption discovery’ stage,” says

Rungtusanatham. “In this paper, we add novel insights regarding the recognition and diagnosis aspects of the ‘disruption discovery’ stage. These novel insights reveal how and why sourcing firms reduce their overall ambiguity associated with detecting and assessing losses from supply disruptions through establishing strong ties with their supply base and how and why reducing such ambiguity improves inventory turnover performance.”

Known as Canada’s Global Business School, the Schulich School of Business in Toronto is ranked #1 in Canada and among the world’s leading business schools by a number of global MBA surveys, including The Economist, Forbes, Corporate Knights and CNN Expansión. The Kellogg-Schulich EMBA program is ranked #9 in the world by The Economist.

Agency partnerships, audio marketing on the upswing in 2023, survey finds.

Word is that one in four marketers have ‘fundamentally changed’ their digital strategy. Amidst shifts in consumer behaviour and a challenging economic climate, marketers are increasing their use of audio marketing, and more broadly, their reliance on agency partnerships, according to the 16th annual Digital Marketing Pulse Survey released by Ipsos Canada in partnership with the Canadian Marketing Association. The report evaluates how digital tools and strategies are viewed and utilized across the industry, with a view to helping marketers navigate the constantly changing circumstance.

“As we head into an uncertain future, advertisers must adapt. One in four marketers and agencies agree that the current economic realities have ‘fundamentally changed’ their approach to digital marketing,” said Steve Levy of Ipsos Canada.

Audio marketing is one strategy that is gaining ground. 54 percent of Canadian consumers say they are willing to receive digital advertising through audio streaming apps, yet marketer usage has been comparatively low in recent years…. until now. 2022 saw the frequent use of digital audio advertising move up from 24 percent to 33 percent for agencies and from 17 percent to 29 percent for marketers, reflecting the increasingly sophisticated and scalable marketing opportunities that exist on these platforms.

“Given the growth of Spotify, Apple Music and the world of podcasting, it should come as no surprise that there’s been significant growth in the use of digital audio marketing,” Levy said. “As the quality of the content improves and the audiences expand, we anticipate significant investment in digital audio strategies which can provide for great brand narratives.”

These shifts in audio, and other strategies,

demonstrate marketers’ resilience and agility.

“The Digital Pulse research is another proof point for how incredibly agile Canadian marketers and agencies are,” said Alison Simpson, president and CEO, Canadian Marketing Association. “They’re navigating unprecedented uncertainty and adapting their approaches to deliver business results in the face of changing consumer needs and market dynamics.”

In 2020 and 2021, just 28 percent and 25 percent of marketers, respectively, said they’d increased their reliance on agency partnerships. But the pendulum swung back this year, with 42 percent of marketers reporting that they’d increased their reliance on their agency.

This pivot doesn’t necessarily indicate a return to the past, however. Many teams are creating a “hybrid model,” where marketers take specific tasks in-house and rely on agencies for others. At the same time, others are outsourcing certain tactics or elements of tactics for access to innovation and specialization – talent that is not available in-house. And these changes are accompanied by a wave of new challenges not least of which is the disuse of third-party cookie tracking.

“The realignment of the brand-agency collaboration, and the variety of approaches to this, reflect how marketers are embracing new ways to reach consumers in a landscape that is increasingly dynamic and complex,” Simpson said. “The revitalized relationships between marketers and external agencies reverses a pandemic-era trend and signals a broader strategic shift.”

The CMA’s purpose is to “embolden Canadian marketers to make a powerful impact on business in Canada”. Ipsos is one of the largest market research and polling companies globally, operating in 90 markets and employing over 18,000 people.

Free Santa DIYversity toolkit makes Christmas more inclusive.

Santa gets multiple makeovers to better represent diverse families that are traditionally underrepresented during the holiday season. For hundreds of years, Santa has been portrayed in the exact same way across every Christmas touchpoint: with one skin tone only. As a result, many children with darker skin tones have worried about Santa not visiting their homes over the holidays because he doesn’t look like them or the people in their families.

To solve this problem, three advertising industry friends - André Yumbla-Bell, Andrew Oliver, and Eric Seenarine – created SantaDIYversity.com, a first-of-its-kind, opensource style, online Christmas toolkit for families of all backgrounds and skin tones. At

// 4 ❱ DMN.CA DECEMBER 2022

■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■

■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■

❯

SantaDIYversity.com parents can download free wrapping paper designs, greeting cards, gift tags, t-shirt templates, and other DIY decorations featuring a Santa with their family’s skin-tone(s), making the holiday season happier and more inclusive for all.

“As multicultural individuals whose family’s skin tones cover the spectrum, we wanted to create something that made everyone feel included during what is supposed to be the most wonderful time of the year”, says Seenarine. “Children in our families have felt worried that Santa isn’t for them because his skin colour is different than theirs, so we knew we had to do something to address this hurtful narrative,” adds Oliver. “Our industry skills allowed us to create a toolkit that expands on Santa’s existing look, embracing all his existing magic to include all kids who might not relate to or identify with traditional Santa imagery,” says Yumbla-Bell.

The SantaDIYversity.com online toolkit includes:

8.5 x 11 wrapping paper template

❯ 11 x 17 wrapping paper template ❯ 3 greeting card designs ❯ Gift tags

❯

Cricut t-shirt and mug design template

The three friends hope that a project like this will impact society , and at the very least, their own families, especially the young children in them. They explain that the purpose of this project is to embrace modern representation in a very traditional space. By sharing these design tools with the world using an “opensource” approach, they’re hoping to have a positive impact on as many families as possible. They didn’t see others doing much to make Santa and Christmas more diverse and inclusive, so they decided to do it themselves.

“This project was self-funded by the three of us,” says Yumbla-Bell. “We have no plans to monetize this offering, and are purposely launching it as an early gift to parents and families like ours who may feel underrepresented by the current Christmas machine.”

and their goal is to help make a world where everyone feels seen, heard, and represented.

Bumble shares what to expect from data in

The women-first dating app has released its annual predictions for the seven trends that will shape dating in the new year, including Open Casting, Wanderlove, Guardrailing, and more. This year brought the return of iconic Y2K couples and fashion, an obsession with pink barbiecore, and viral beauty hacks. But what about our dating lives?

Bumble’s 2022 trends focused on rediscovery as we emerged from the pandemic with new behaviours such as hardballing, the rise of alcohol free ‘drydating’, and an obsession with making hobbies part of our dates.

Looking ahead, it seems this year has taught us some lessons about what we want and how to best articulate our needs and boundaries. Following 2022’s year of rediscovery, Bumble’s global research suggests that next year will be more focused on challenging the status quo and finding more balance in the way we date.

According to the popular dating app, we should be optimistic about dating in 2023, with 70 percent of people around the world saying they feel positive about the romance that lies ahead.*

When it comes to dating next year, Bumble suggests we should expect…

1. Open Casting: It’s time to do away with the tall, dark, and handsome requirements

as the narrow search for our physical ‘type’ is not serving us. The opposite of type-casting, open casting refers to how 1 in 3 (38 percent) people around the world are now more open to who they consider dating beyond their ‘type’. 1 in 4 (28 percent) are also placing less emphasis on dating people that others ‘expect’ them to, which especially rings true in Canada, where 1 in 3 (33 percent) Canadians said the same thing. What are people looking for? The overwhelming majority of global respondents (63 percent) are now more focused on emotional maturity than physical requirements.

2. Guardrailing: With the return of office culture and busy social schedules, the majority of people are feeling overwhelmed right now. This has forced us all to prioritize our boundaries and more than half of global respondents (52 percent) have established more boundaries over the last year. This includes being clearer about emotional needs and boundaries (63 percent), being more thoughtful and intentional about how we put ourselves out there (59 percent), and not overcommitting socially (53 percent). These numbers were even higher for Canadian respondents, as 66 percent are being clearer about emotional needs, 64 percent are being more thoughtful and intentional with how they put themselves out there, and 55 percent are not overcommitting themselves socially.

3. Wanderlove: Looks like we’re after an ‘eat, date, love’ moment with 1 in 3 (33 percent) Canadians saying that they are now more open to travel and relationships with people who are not in their current city. Post-pandemic WFH flexibility means that 1 in 7 (14 percent) global respondents have explored the idea of being a ‘digital nomad,’ opening up how we think about who and where we date.

4. New Year, New Me(n)/Modern Masculinity: Conversations about gender norms and expectations have been front and centre. Over the last year, 3 in 4 (74 percent) men from around the world share

// 5 DMN.CA ❰ DECEMBER 2022

Founded by three creative types with diverse backgrounds that want to make a difference, their families are uniquely diverse, ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■

2023.

talkingpoints

that they have examined their behaviour more than ever and have a clearer understanding of ‘toxic masculinity’ and what is not acceptable. More than half of men on Bumble (52 percent) are actively challenging stereotypes that suggest that they should not show emotions, for fear of appearing weak, and while 1 in 3 (38 percent) men around the world now speak more openly about their emotions with their male friends, this number is even higher for Canadian men on Bumble, as 42 percent said the same thing.

5. Dating Renaissance: Much like a wellknown Queen B, many of us are having a renaissance with 1 in 3 (39 percent) of those on Bumble having ended a marriage or serious relationship in the last two years. These people are now jumping into their second chapter with 1 in 3 (36 percent) using dating apps for the first time, learning to navigate new dating language and codes.

6. Ethical sex-ploration: The way that we are talking, thinking about, and having sex is changing. More of us are approaching sex, intimacy, and dating in an open and exploratory way (42 percent). Sex is no longer taboo, with more than half (53 percent) of the global respondents agreeing that it’s important to discuss sexual wants and needs early on; this is even more true in Canada, where 57 percent said the same thing. Over the past year, 22 percent of Canadians have explored their sexuality more, which is slightly higher than the global average of 20 percent, and nearly 1 in 5 (17 percent) Canadians have recently considered a non-monogamous relationship, which is also higher than the global average (14 percent). However, this doesn’t mean we’re all having more sex. In fact, more than 1 in 3 global (34 percent) and Canadian respondents (35 percent) both shared that they are not having sex, and they are fine with this.

7. Cash-Candid Dating: The rising cost of

living has led to more honest and open conversations about money and dating with more than 1 in 4 global (28 percent) and Canadian (29 percent) respondents setting financial boundaries for our dating lives. This doesn’t mean we’re dating any less, but rather that we’re changing how we date with a majority of both global (57 percent) and Canadian daters (59 percent) sharing that they are more interested in casual dates than something fancy. In fact, nearly 1 in 3 are less impressed by over the top first dates.

Shan Boodram, Bumble’s Sex and Relationships Expert said: “In 2023, we will continue to see how external factors – such as working remotely and the rising cost of living – will affect our dating behaviours. Additionally, I’m excited to see how people’s approach to dating will shift as many will challenge the status quo and find more balance in the way that they date. As 49 percent of Bumble members in Canada shared that they’re approaching dating in a thoughtful and considered way, we’re excited to watch these trends play out and can’t wait to see what 2023 has in store for our community.” To help people connect in meaningful ways, those within the Bumble app can now recommend a profile to a friend via the ‘Recommend to a Friend’ feature. If you come across a profile on Bumble that’s not right for you but might be for someone you know, you can now directly share a link to their Bumble profile.

Nearly half of Gen Z Canadians believe social media has a negative impact on their mental health.

Despite being digital natives, Gen Z consumers have started to exhibit some self-awareness and are questioning if allencompassing tech usage is good for them. New Mintel research indicates that while 51 percent of Gen Z Canadians (aged 13-17) cite a desire to integrate more tech into their lives, nearly the same percentage (47 percent) also agree that social media and large amounts of tech usage have a negative impact on their mental health. In fact, 47 percent say they are trying to limit their social media usage. When examining the platforms that Gen Z uses, all of them rely heavily on visual interaction: Mintel research shows Gen Z Canadians engage with YouTube the most (77 percent), followed by Instagram (75 percent), Snapchat (58 percent), and TikTok (52 percent).

Michael Lloy, Senior Technology Analyst, Mintel Reports Canada, said: “Our research shows that due to significantly more time spent on these platforms, a portion of Gen

Z has become more aware of their mental health and are exploring ways to reduce their usage of social media. This indicates that there is growing discontent among younger consumers about the negative effects that social media has on their lives, which may prompt radical behaviour shifts away from social media as they age. This will require brands to think strategically about how and where they market to Gen Z consumers as they age in order to develop and sustain an engaged and loyal audience.”

Gen Z consumers use of social media is a behavioural trait that sets them apart from other demographics. They are a heavily plugged-in generation with 51 percent saying they are on the hunt to find technology to make their lives easier, more efficient, or more exciting. What’s more, 64 percent say they engage with social media more than TV/ movies.

However, nearly half of Gen Z (47 percent) agree that social media has a net negative effect on their mental health and nearly all (95 percent) agree that mental health is just as important to maintain as physical health.

“Gen Z reducing their screen time due to mental health concerns presents an opportunity for brands to lean into the visibility of their values in order to be seen to support causes that Gen Z cares about. Both Millennials and Gen Zs are heavily plugged-in generations, but there are a few, notable differences when it comes to social media. First, while Gen Zs are digital natives, most Millennials are not, and this informs the speed at which each generation adapts to new technology. Life stages are another piece of the puzzle. Millennials are a split generation. Some Older Millennials are married, homeowners, have children, or some combination of the three, while some Younger Millennials are closer to Gen Z in their life stages. These key differences will be important for brands to remember as they market to Gen Z consumers moving forward.”

Since its launch in late 2021, the metaverse has been a popular topic for brands but has made less of a splash among consumers. Mintel research shows only 3 percent of Canadian Gen Z consumers actually use the metaverse and 26 percent have never heard of the metaverse before now.

“As many Canadian consumers are getting back to their pre-pandemic lifestyles, including in-person gatherings, the lack of eagerness to interact with the metaverse has been evident. Overall, only 15 percent of consumers, on average, can even envision a world where they interact using the technology, meaning brands that currently or plan to leverage the metaverse in their marketing strategy have some work in front of them in order to convince consumers of the metaverse’s usefulness and applicability to their daily lives,” concluded Lloy.

// 6 ❱ DMN.CA DECEMBER 2022

■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■

❯

Does Direct Mail Work Anymore?

BY BILLY SHARMA

The answer is a resounding “YES!”

Direct mail is referred to as “salesman in print” for a very specific reason: it allows you to make your pitch or tell your story, long or short. However, direct mail will only work as hard as you do — if it is done in the proper way, to a good list, with a compelling offer, and with targeted and persuasive creativity.

Having created hundreds of successful direct mail packages for all the companies listed alongside, here are some of the rules that I have learned from others and from my own experience:

1. Get to the point immediately. You must get to the point, and the offer — faster than ever before. People no longer wait patiently for the “punchline”.

Here’s proof: the classic Wall Street Journal two-page letter, that raised a million dollars for the Wall Street Journal, was finally beaten (after 32 years!) by a simple list of everything you received with your subscription.

2. Bullet-proof your information. People have very little “disposable attention” today and only spend it on things that really interest them. So, organize the information for them. Lists and bullet points are extremely effective. Side bars work well. So do short sentences, small paragraphs and white space. By the way, these rules also apply to emails. Above all, be clear about exactly what you want them to do — and why they should do it — now.

Example: What catches a reader’s attention?

❯ The salutation

❯

A headline or Johnson box

❯ A captivating first sentence (keep it short; no more than

❯ 10 words)

Underlines: in direct marketing, use sparingly; in viral marketing, underline only words as hyperlinks

❯

❯ The closing

❯ Who signed it or the sender

❯ The P.S.

❯ Images (with captions or inserts)

❯ Free offers

Things to click on. This applies to the numerous links to the donation page in viral marketing.

❯ Interactive features: in direct mail use scratch cards, involvement devices, a quiz, etc. In viral marketing use a button to click on to forward to a friend.

3. Attraction is Not Enough. Once upon a time, a great opening sentence or headline was enough. And of course, you still need one. But today, you don’t just need to attract their attention you need to keep their attention — sentence by sentence, paragraph by paragraph. Otherwise, people get bored.

A Covenant House letter did that in spades. Email me and I will send you a copy.

4. An Added Dimension. Direct mail is the only medium I know where you have three dimensions to work with, and no limits on how much information you can provide. It allows people to hold the product or your marketing material in their hands.

5. E is for Engagement. Without engagement you are not getting that stickiness to hold your reader’s attention. For example: The International Rescue Committee (IRC) raised millions for Refugees. They used videos on their social media sites and on their website and even had links to it in their direct mail material. They were successful in spreading their emergency messaging, resulting in over 7 million views, 57 million impressions, and a 90 percent awareness.

Here’s the VIDEO LINK: https:// youtu.be/JfQTFD_5CX8

narrow their focus on the copy. Short columns are easier to scan. Keep your copy width down to sixty characters or less — that’s about six inches, maximum. Think paperback novels. Beyond that width the reader needs to move his head back and forth horizontally, making reading more difficult. It can also literally be a pain in the neck.

7. Add Photos to Tell a Story. Example: Move the letter to one side and add a sidebar with a testimonial from someone who benefited from your organization’s good work. Or add a tear-off column with helpful tips or a schedule of upcoming events.

8. Promises, Promises. Remember, we are not just selling a product we are also selling a promise.

Good writing in our business is not academic writing, but persuasive writing. Forget what you learned in school about good grammar, direct marketing, or fundraising copy. Your words should sound like someone talking — like a conversation with the reader.

❯

for me?”

❯ Contrast: black and white, new versus old. That’s why comparison tables are extremely effective.

Texture, tactility. It’s the only channel we have to awaken one of the senses that isn’t often used: make your readers feel bumpy, lumpy, odd shapes, and all that sort of stuff.

❯ Tangibilty, touch. It’s real, it’s physical. It can do things. And in print, we can have things pop up; we can have things unfold. Every time we get that involvement of the real, especially in direct mail or where things are unfolding with pieces and multiple elements—that’s giving us time of consideration.

❯ Emotionality happens through story and through picture.

9. Relevancy. Finally, it’s not just personalization that attracts, it’s relevancy.

Example: The Environmental Defence Fund put together an interesting little quiz called Earth Day Jeopardy. Rather than go on and talk about the issues to their donors, they challenged them to take a few minutes to test their knowledge. It is a great engagement idea with plenty of value.

❯

Bolded or italic sentences (use sparingly)

Bulleted lists

❯

6. Easy Reading. Make sure that the width of the letter is designed for optimum legibility.

Use wide margins, so readers

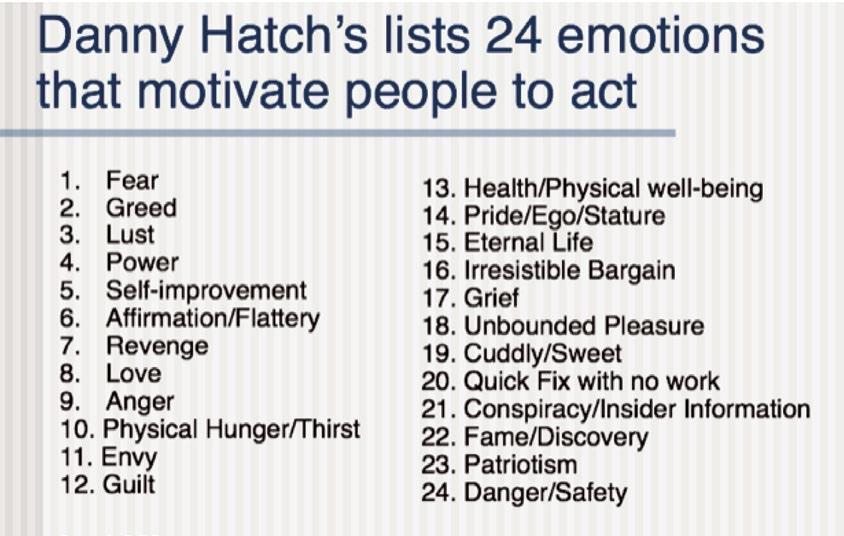

Example: Danny Hatch listed several emotional copy drivers. He said that if your copy isn’t dripping with one or more of these tear it up and start all over again. Today, these copy drivers are considered as neuroscience since they engage the primal brain releasing dopamine or one of the hormones that stimulates interest. Emotions are the biggest factors that make us buy or want a product or donate to a cause.

Five major stimuli

❯ “You-centricity”—“what’s in it

Another great example: After the recent controversial Supreme Court of the United States decision on abortion, the charity, National Organization for Women (NOW), sent an invitation to their donors to go to a planning meeting in the town right next door. Sometimes charities seem to forget the incredible power to “localize” their brand. This was a great example of doing it right.

BILLY SHARMA is President & Creative Director of Designers Inc. He started his career in the advertising world and have worked in four major cities — Munich, Montreal, New York and Toronto for some of the largest advertising agencies. For the past three decades he has run his own company, Designers Inc.

// 7 DMN.CA ❰ DECEMBER 2022

DM

TRADITIONAL

Direct Marketing is a Lloydmedia, Inc publication. Lloydmedia also publishes Foundation Magazine and Total Finance Magazine. 2023 Plan your media buy. Great rates. Brilliant results. Get Your 2023 Media Kit Now www.dmn.ca and Connect To Readers in Multiple Channels Steve Lloyd steve@dmn.ca

The Growth of the EcosystemConnected Business

STAFF

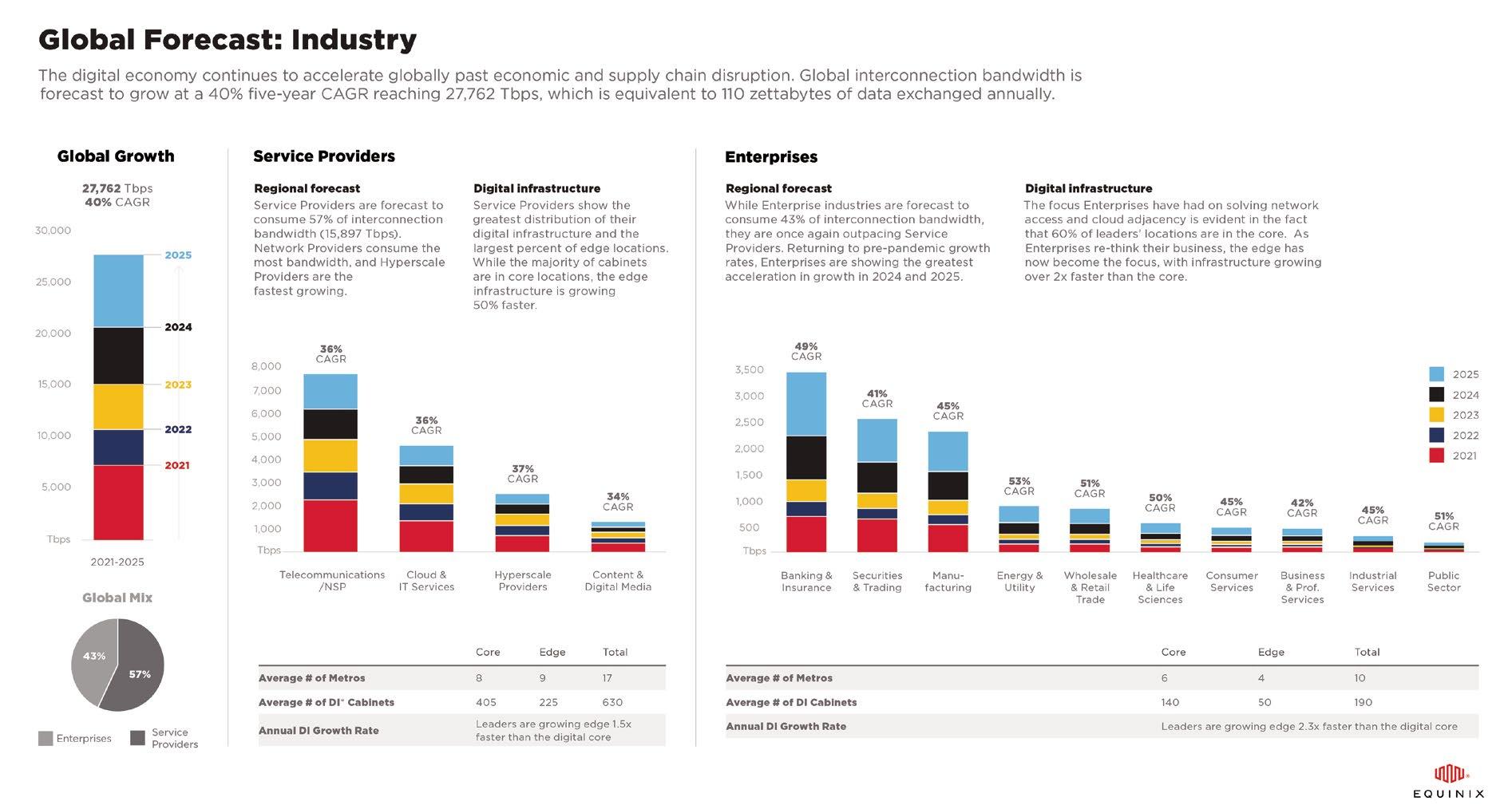

Current supply chain constraints and geopolitical and economic instabilities are not slowing the pace of digital infrastructure investment for the most connected companies, according to a new report.

The latest Global Interconnection Index (GXI) 2023, an annual market study published by Equinix, found that the most ecosystem-connected businesses — those directly interconnecting with partners to provide their own digital services — have expanded their digital operations more in the past five quarters than in the previous five years. On average, organizations are connecting to three times as many business ecosystem partners and metros, consuming more than twice the amount of interconnection bandwidth.1

As businesses reinvent themselves in the aftermath of the global pandemic, ecosystem density has become a catalyst for digital innovation, which continues to fuel the growth of interconnection bandwidth. According to GXI 2023, global interconnection bandwidth is forecast to reach 27,762+ terabits per second (Tbps) by 2025, representing a five-year compound annual growth rate (CAGR) of 40 percent, equivalent to 110 zettabytes of data exchanged annually, or enough bandwidth to support over 50 million autonomous cars each exchanging over 2,000 terabytes (TB) of data per year. This forecasted growth shows how organizations are rethinking their business to implement future-proof infrastructure on technology platforms.

Toronto was the second largest edge metro in the Americas behind Los Angeles; with a growth rate of 46 percent CAGR; while Montreal was listed as the eighth largest edge metro behind Houston. Toronto was also identified as mature Financial Service hub,

showing nearly 20 percent of bandwidth being driven by B2B partner access. By industry, Toronto was also ranked fourth in the Americas for securities and trading; and industrial services.

“In today’s dynamic setting, every business is becoming a digital provider, which requires a new type of digital infrastructure built sustainably around leveraging ecosystems to deliver seamless digital experiences. Those with a digital-first strategy in place, investing in a robust, future-looking business model and interconnecting to rich ecosystems, are prepared to scale, adapt and thrive,” said Steve Madden, Vice President of Digital Transformation & Segmentation at Equinix.

Additional Insights from GXI 2023

Interconnection continues to accelerate in Canada, with Toronto the second largest edge metro in the Americas behind Los Angeles; while Montreal was listed as the eighth largest edge metro. Globally, interconnection bandwidth is forecast to continue growing at over 35 percent CAGR across all regions and major metros through 2025.

Financial sector drives interconnection: Toronto was also identified as a mature Financial Service hub, showing nearly 20

percent of bandwidth being driven by B2B partner access. By industry, Toronto was also ranked fourth in the Americas for securities and trading; and industrial services.

The move to the edge is accelerating: both enterprises and service providers are forecast to interconnect to edge infrastructure 20 percent faster than the core globally.

Businesses are becoming digital providers: GXI 2023 predicts that 90 percent of Fortune 500 companies will become digital providers, both selling and consuming digital services by 2025.

The sustainable road to digitally thrive: All industries are harnessing digital to accelerate ESG objectives, where 64 percent of Canadian IT decision-makers say sustainability is now one of our organization’s most important drivers.[1] GXI 2023 forecasts the Energy & Utility sector to lead in digital growth rate through 2025 as all organizations explore a sustainable approach to build and expand their digital presence.

“As digital transformation strategies continue to accelerate in this digital-first economy, organizations in Canada and abroad are under pressure to invest in digital infrastructure to keep pace,” said Andrew Eppich, Managing Director, Equinix Canada. “Interconnections within

Toronto and Montreal have continued to grow since the last Global Interconnection Index, but we’re also seeing a renewed effort to improve interconnection from coast to coast. Equinix remains committed to building Canada’s digital infrastructure; and empowering national and global businesses with the solutions and services to fuel interconnection and growth.”

Industry Perspective on the Global Interconnection Index

Steve White, Program Vice President, Channels & Alliances, IDC. “As companies increasingly adopt digital-first strategies and look for new ways to drive differentiation, the ecosystem plays an even more critical role. Organizations are relying on ecosystems and digital infrastructure as the foundation to sustainably scale and deliver business value. In order to achieve these business outcomes, companies are interconnecting to customers, partners and vendors to accelerate collaboration and co-creation, as well as meet sustainability commitments.”

1. Equinix (Nasdaq: EQIX) is the world’s digital infrastructure company™. Digital leaders harness Equinix’s trusted platform to bring together and interconnect foundational infrastructure at software speed. Equinix enables organizations to access all the right places, partners and possibilities to scale with agility, speed the launch of digital services, deliver world-class experiences and multiply their value, while supporting their sustainability goals.

// 9 DMN.CA ❰ DECEMBER 2022

LOGISTICS

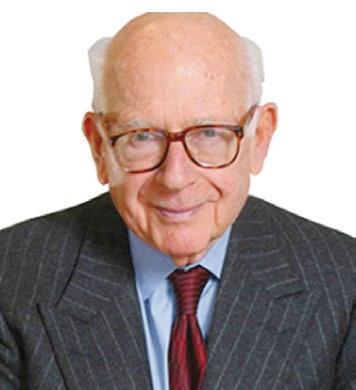

Loyalty 2.0:

An Interview with

Matthew Seagrim,

Senior Vice President, Scene+

BY STEPHEN SHAW

BY STEPHEN SHAW

For thirty years the Air Miles Reward Program has ruled the skies in Canada. Its familiar blue membership card can be found in the wallets of roughly 10 million Canadians. But in recent years Air Miles has lost altitude. Several high profile sponsors have exited the program, most notably Sobeys, the second largest supermarket chain in Canada, which this past summer switched over to the newly revamped Scene program, now called Scene+. The switchover followed the move by Sobeys owner, the Empire Company, to team up with Cineplex and Scotiabank as a joint owner of the coalition loyalty program.

The Scene program was launched in 2007 as a way for Cineplex and Scotiabank customers to earn rewards going to the movies and buying snacks. But exactly one year ago Scene merged with the Scotia Rewards program to offer members many more ways to earn rewards. Now members can not only rack up points on their movie-going and credit card purchases, but they can also take advantage of earning opportunities through the online cashback company Rakuten and by booking travel through Scene Plus Travel powered by Expedia. And that’s just the start. Next summer Home Hardware stores will be joining the program, making Scene+ a formidable contender for front-of-the-wallet status.

Historically coalition programs have floundered everywhere in the world but Canada. Thanks in part to urban density, the existence of strong national brands in high volume earning categories like groceries, banking, fuel and retail, and an affinity amongst Canadians for loyalty programs (the average household has 13 memberships), the loyalty market in Canada is thriving. It is estimated to be worth $4.4 billion and is expected to grow at a compound annual growth rate of 11 percent over the next four years. No wonder Scene has elected to transform itself into a full fledged

coalition loyalty program, determined to grow its 10 million member base.

The argument in favour of a coalition versus a proprietary program has always been strength in numbers, giving members greater “earning velocity”. But a careful balance has to be struck between the perceived value of those rewards and the effort required to obtain them. Attempts to devalue that currency — or make it harder to redeem points — or rely on “breakage” (that is, unredeemed points) to inflate the bottom line - can backfire (as Air Miles discovered when it tried to put a 5-year expiry on points, igniting a fierce consumer backlash that forced the company to back off). Plus, the various category sponsors have to be deftly managed as well. Category exclusivity promises have to be honoured — conflicting strategic priorities resolved — proof supplied that members are buying more, more often. Not to mention the technical complexity of converting purchases across many different payment systems into variable points currency and then personalizing member offers based on their particular affinities.

Matthew Seagrim, the strategic architect behind the transformation of Scene1, is intimately familiar with all of those challenges. For seven years he worked at former Aeroplan owner Aimia in charge of product strategy. And for the past seven years he’s been in charge of program development at Scene. His efforts are being rewarded — a staggering 65 percent growth in membership over that time, and recognition as one of the top-ranked programs in the country. But Scene is on a mission to create a next generation program — one that goes beyond discounts to offer members even more of a rewarding experience.

// 10 INTERVIEW

STEPHEN SHAW is the Chief Strategy Officer of Kenna, a marketing solutions provider specializing in delivering a more unified customer experience. Stephen can be reached via e-mail at sshaw@kenna.ca

CONTINUED ON page 14 ❱ DMN.CA DECEMBER 2022

COURTESY SECNE+

Stephen Shaw: As a mechanical engineering graduate, did you ever imagine that you’d be running one of the largest loyalty programs in the country?

Matthew Seagrim: I certainly never did. I made a decision to study engineering hoping to build spaceships and had the good fortune to do really neat projects like working on designs for the Mars Pathfinder Rover. At the end of undergrad, I came to Toronto because there was an opportunity in management consulting, which struck me as a really interesting field. As it happened, Canada Trust was planning to move their head office from London, Ontario, to Toronto. One of my colleagues at the consulting firm approached me and said, “Look, they’re trying to build a team. They’re trying to scale this business. They’re trying to relocate it. They’ve launched a really interesting partnership with Capital One.” Canada Trust would provide Capital One with back-office support, while Capital One would bring their world-class thinking around analytics and datadriven marketing, capabilities that were leading edge at that time. It just seemed like a really interesting opportunity. So I joined this very small team that was in startup mode, trying to scale the leadership in the Toronto office, and it was fascinating. We learned an enormous amount over a short period of time about how to leverage data, to personalize offers, drive adjudication, make smarter banking decisions, and as a team, we were able to learn from this advanced analytics group at Capital One.

SHAW: As I recall the whole field of customer analytics was just beginning to mature around that time in the late 1990s led by the big banks and card marketers. SEAGRIM: Yeah, it was an industry that was in transformation, and there were some leaders in that space who were using analytics to drive personalization in a way that organizations had never done before. And because our team was so small, everyone was wearing many hats. I don’t think there were many other places in the country where you could be responsible for credit card acquisition while also helping to set the adjudication policy and the line assignment policy and the income verification policy. Usually, those duties are quite separate. So, it was a really interesting place to be, and it set me on a path for the next ten years working in product development, in one-to-one marketing, in product management, in financial services.

At Canada Trust I worked on a number of new co-branded loyalty products, did loyalty co-brand design when I moved over to Citibank for a few years, and then ultimately, moved to PC Financial when they were still in growth mode, and again found myself in this extraordinary team of people, small, really

committed, passionate about what they were doing, feeling like we were changing the world by creating something fundamentally new, on a rocket ship, just driving incredible growth and disrupting the industry. And that led me to Carlson Marketing, which was later acquired by Aimia, allowing me to broaden into other areas of consumer-focused marketing. So, I did a tremendous amount of product development with most of the major banks across the country, getting exposure to card-linked loyalty through work Aimia was doing in that space, and then also an opportunity to work internationally, building out product concepts in Mexico with Club Premier, and launching a product in Thailand with Thanachart Bank.

could engage directly with their customers. And the arrangement they had with Aimia limited the value they were getting from the program. So, when it was finally announced it felt like the right thing to do. In many ways, it was the end of an era for Aimia. But it seemed like the best outcome for everyone.

SHAW: So you left to join Scene — I’m going to call it 1.0 — as Managing Director, and at the time, the program was simply a way to collect points by going to movies and buying popcorn. At what point did it start to shift from an entertainment to a lifestyle program?

SEAGRIM: That was really part of the conversation when I joined in 2015. When I arrived it was already a well-loved program. Scene was created as a joint venture between Cineplex and Scotiabank to create something fundamentally new. Cineplex wanted additional information on who their customers were, while Scotiabank was looking to attract a younger demographic. When they started the program in 2007, it immediately took off. By the time I arrived, it was in 38 percent of households across the country. So it had established a really solid foothold. But the challenge was, how do you take it to the next level?

SHAW: So, you don’t regret giving up your dream of building rocket ships?

SEAGRIM: Well, I think we’ve been building one for the last number of years. And its velocity has been accelerating.

SHAW: I guess so! You were at Aimia just prior to joining Scene. But you left there a few years before Air Canada decided to repatriate Aeroplan2. Did you see the writing on the wall at that point?

SEAGRIM: When I left, it wasn’t inevitable, but one could see there were lots of reasons it made sense. The airline was looking at ways they

We recognized that we needed to work on our positioning. There were some nascent partnerships that were already in place but they just felt awkward: so it was hard to make sense of our story. And that led us to do some really profound branding work, trying to understand what the program’s role was in the lives of its members. As we started talking to our members we heard all these stories about how it was helping them in their lives — such as people who told us that the program was how they went on their first date with the person they later married. We had grandparents who told us that this was the way they could have a dinner out every month with their grandkids. We had families tell us it was the only way they could afford to do some of the things they wanted to do in their lives. And the more we dug into it, the more it became clear that the reason Scene had such a strong member attachment was more than the reward, more than the transaction, it was that we were enabling people to spend time with friends and family.

Once we understood the role that the program actually played in people’s lives, it allowed us to reposition and rebrand the program. So we went from being an entertainment program in 2015 to being all about encouraging togetherness in 2016. And that was the spark that helped us to expand our partnerships in dining, to partner with the NBA, to build out a music brand. It allowed us to really take the program to a place where we could credibly be more than we had been before. And that allowed us by late 2019 to grow past 10 million members. At that point, we were in 53 percent of houses across the country. So, really

// 14 INTERVIEW CONTINUED FROM page 11

❱ DMN.CA DECEMBER 2022

“We were enabling people to spend more time with their friends and family.”

meaningful growth out of this one key insight into the role that we played in people’s lives.

SHAW: So the inflection point was this unifying idea of family togetherness?

SEAGRIM: That’s exactly right. And beyond allowing us to partner with more organizations, it really gave the team a sense of profound meaning about what we were doing. It ignited the imagination of our marketing teams and our agencies. And, quite importantly, when movie theaters and restaurants were closed during COVID, we still had this meaningful message that we could communicate around “better together even when we’re apart” that would not have been possible otherwise.

SHAW: You launched expansion of the program last year — Scene 2.0, can I call it? — to extend the earn and burn opportunities. Can you take me through the thinking around your partnership strategy?

SEAGRIM: I have to take a step backwards to explain how this all came together. Scotiabank, prior to this summer, was a 50 percent owner of Scene. We’ve now welcomed Empire as a one-third owner3. So the three owners each have a third. But in 2019, Scotia was looking at not only their ownership in Scene but also at their own proprietary program, Scotia Rewards, and they made the strategic decision to go all in on Scene. And so, what we ended up doing at the end of last year was merge the two programs together, and that’s what allowed us to launch Scene+. Scene moved from being entertainment only to becoming a broader lifestyle program with more ways to earn and redeem points with a series of partnerships.

SHAW: Is the positioning still around togetherness, or has that had to evolve as a result of the relaunch?

SEAGRIM: Yeah, it’s had to evolve. But we’re trying to do it in such a way that we don’t lose a lot of that equity we’ve built in the brand position. There’s so much of what we’re doing that’s still about doing the things that you love with the people that you love.

SHAW: You have this tripartite alliance now across three entirely different businesses. Is it tough to get strategic alignment around the goals of the program?

SEAGRIM: There’s been a lot of work with the Empire leadership team and our board of directors around everyone’s aspirations for the program. And what’s been wonderful is how committed everyone is to the same goals. Everyone’s interested in building a program that they can be proud of. Everyone’s interested in building a program that builds real value for their customers. Everyone is fully committed to creating

something that allows them to unlock the power of insights across this ecosystem that we’re building. So I’d say at the macro level, we’ve got tremendous alignment. And it was really important in the early days of building out this strategy to make sure that we clearly understood the strategic priorities of each organization independently, and that we could have one North Star to rally around as we were building something greater together.

SHAW: Did Sobeys see this as a way to scale its loyalty program in a way that it couldn’t have done on its own?

SEAGRIM: I think Sobeys saw the commitment from Cineplex and Scotia to build something great together. They saw momentum in the program and a level of engagement with the brand that was really strong. We also had a really strong commitment as an organization to creating value for our owners and our partners. But this was a big decision. It was a very strategic move by a very large and powerful organization in a highly competitive market. All of us at Scene are humbled by the fact that they’ve made this decision, but we also keenly feel a great responsibility. Sobeys is in a highly competitive market, Scotia is in a highly competitive market, Cineplex is just coming out of COVID, trying to make sure their business is going to thrive going forward. And we have a part to play in helping them.

SHAW: Rakuten is a huge multi-retailer cashback program. In some ways you can almost consider them an indirect

competitor. Why partner with them?

SEAGRIM: We felt it was a really important partnership to help us broaden the appeal of the program, and also to bring in an e-commerce partner that allowed people to have more opportunities to find value in the currency. Rakuten has done an exemplary job of building strong relationships with their customers. The feedback they get from their customers is overwhelmingly positive, consistently, and we felt that we had a lot of alignment between our brands and in the objectives we were trying to pursue. So, it really did feel like a win-win in striking a partnership with them.

SHAW: Coalition programs have floundered pretty much everywhere in the world but here. Are Canadians just more receptive to these types of programs? Or is it the fact that we have national brands in almost all of the key categories?

SEAGRIM: We’ve not only got more programs per person than many countries in the world but more engaged participation per person. One of the key differences is our partners want to be part of something bigger instead of going it alone. They recognize the advantages of instantaneous scale, the opportunity to tap into network effects, to shift brand preference from their next nearest competitor to themselves. But we’ve also very deliberately gone into these conversations with a view to maximizing the data that we can make available to our partners, to helping our partners build their own ability to market to their customers.

SHAW: The economic model is interesting, too. Certainly, Air Miles has made a lot of money on breakage. But you’re actually trying to achieve financial goals that align with your owners as opposed to operating purely as an independent business unit trying to maximize your bottom line.

SEAGRIM: Yeah, our structure has been a key part of our success. We don’t have an external shareholder to please. We’re all about creating value for our members, owners and for our partners. We haven’t had to make the choices that some other organizations have had to — reduce the dividend to a member or reduce the value of a reward, or intentionally drive-up breakage. We take quite the opposite approach. We’re quite proud of having very low breakage rates and of delivering really high value to our customers in the market. We’ve long considered ourselves to be more of a customer engagement platform than a loyalty program, per se. What we’re trying to do is facilitate deeper relationships between our members and our owners and partners. And the best way we can do that is to maximize the value exchange between the two and to reduce friction in the middle.

// 15 INTERVIEW

“Scene moved from entertainment to being a broader lifestyle program.” DMN.CA ❰ DECEMBER 2022

SHAW: You have direct competition with other coalition programs, but there’s also the threat of cannibalization from proprietary programs – and from the growth of retail networks with their own ecosystem of suppliers and partners.

SEAGRIM: When I think back to 2018, we had three versions of the database, we had different ways of calculating and recognizing points, we had incomplete views of customers. But now we have a more holistic and valuable view of a member’s behavior and their participation in the program, encompassing grocery purchases and nights out with the family and banking behavior. And that single, consolidated view is a big advantage over a proprietary program.

SHAW: At this point, the earn and burn opportunities are transactional in nature, discounts and freebies, that sort of thing. Are you looking at some point down the road at other forms of rewards? I’m thinking of experiential rewards as an example.

SEAGRIM: We are pretty uniquely positioned with the assets that we can bring to the table. There’s a world of opportunity for us to take advantage of with all our partners. I think it’s worth noting that Scene+ as a program is only a year old. We are still very much in transformation mode. There’s a lot more building to come.

SHAW: I suppose that’s where analytics can help, yielding insights that lead to innovation and transformation. How are you set up to support that?

SEAGRIM: Over the last two years we’ve been investing significantly in our analytics team, in our engineering team, in building out new dashboards and new reporting, so that we can meet the needs of the expanded program. Now that we are playing such a significant strategic role for all of our partners, we have to start creating different forms of insight. In the day-to-day business, we’re always focused on overall program metrics, engagement in the program, satisfaction, NPS, the typical growth metrics. Coming out of the pandemic, we had to shift our focus very strongly to reactivation, to ensuring that we’re being relevant in our communications, that members were satisfied with the rewards, and being really focused on whether the program was making members more likely to continue doing business with our partner brands.

With Sobeys now rolling out across the country, we want to make sure that our members are aware of the benefits, that they understand the program, that they’re having a smooth enrollment experience, trying to track things like how long does it take before the first transaction. Are you happier now than you were before, either with the old Scene program or with the program that Sobeys was in before? These are the things you’ve got to measure very

closely at this point in our transformation. And in a few months, we’ll be in a very different place again.

SHAW: You have a one-size-fits-all program design right now. A natural evolution is to tailor the program to different segments within your base, particularly given the rich array of data that you’re collecting. Is that part of your vision?

SEAGRIM: The answer is emphatically yes. But I also think it’s really important for us to stay focused on one of the things that has made Scene strong over time. We have had almost a manic focus on simplicity, and that’s been really important for us over the last 15 years to make sure that the program is easy to understand, that when someone signs up they’re not trying to comb through terms and conditions and reward grids and trying to figure out what they get by signing up. It’s critically important that the program be understandable, that it be clear, that the value prop be understood in seconds. And I’d say we’re not all the way done. We’ve still got some things that we want to make even simpler. But to answer your question, while it may look like it’s one size fits all, there’s a tremendous amount of work between amongst the partners to make sure that we’re delivering highly personalized, highly relevant content and offers that really speak to an individual and their needs.

SHAW: Gamification appears to be a growing trend in reward programs to create greater engagement. Blockchain is a potential delivery mechanism for currency. And there’s the metaverse, of course. What’s your perspective on these new technologies?

SEAGRIM: We’ve seen many organizations in this space be very successful at leveraging game mechanics to drive behaviors. We’ve certainly looked at Blockchain and what Starbucks is going to be doing with the Odyssey Program4 that they’ve announced. We’ve had many organizations put forward proposals to do redemptions for cryptocurrencies and a few have gone to market with crypto rewards. Our members’ interest has waxed and waned depending on the value of cryptocurrencies at the moment. Where I’m more interested is where the industry is going on leveraging Blockchain as a tool, and from my point of view that starts to become really interesting when you start talking about member-to-member points transfer or points pooling or cross currency exchange. There’s lots more still to be learned in this space and how it can best be utilized. And metaverse? I think it’s a big, “We’re not sure at this moment.”

SHAW: You and everybody else. What’s the immediate path ahead for the program?

SEAGRIM: The growth with Sobeys has been extraordinary. We’ve brought in 150 percent more members in the last two months than our best year ever — growth that is unprecedented and awe-inspiring. And we’re not done with the rollout. We’re really in the early weeks. And then next summer we’re going to be adding Home Hardware to the business, with a thousand locations coast to coast to coast. And when they join the program, we will have a meaningful presence in communities of every size across the country. We just need to make sure that we’re laying the track out sufficiently ahead of ourselves so that we can maintain the speed and the momentum to achieve our vision without going off the rails. We’re on a journey right now. We’ve been in construction for the last two and a half years. For us to be successful we need to deliver world-class capabilities. And that encompasses analytics, it encompasses data science, it encompasses our ability to maximize our level of insight. And so, there’s a tremendous amount of capability still to be built to make sure that we can deliver against our vision. But we’re feeling like we’ve got a great path ahead.

1. Management of the Scene+ program is in the process of transitioning to Tracey Pearce who was appointed President of Scene in May 2022.

2. Air Canada launched a new loyalty program to replace Aeroplan in 2020. Aimia subsequently became an investment holding company.

3. In June 2022, Empire Company joined the partnership and added its supermarket chains, including Safeway and Sobeys, to the Scene+ program.

4. Odyssey is a Web3 offering by which Starbucks Rewards members can purchase and trade limited-edition NFTs to secure rewards benefits and earn digital badges called “journey stamps” that can be redeemed for experiential rewards like virtual espresso-martini-making classes or international trips.

// 16

INTERVIEW

❱ DMN.CA DECEMBER 2022

“We’re delivering highlypersonalized, highlyrelevant content and offers.”

Customer Growth: 7 Ways for Financial Service Firms to Drive Growth

BY TODD HOOVER

Your financial services firm serves a wide range of consumers, each with varying financial needs and goals. But not all consumers offer the same potential for your brand. Especially when consumers face inflation and economic uncertainty, like many are currently.

In fact, about 20 percent of households hold more than 84 percent of the nation’s wealth. These are the consumers that hold the most opportunity for growth — they invest more, spend more, and pose less risk than other consumers. Despite higher prices, these consumers continue to buy their desired goods and services while still accumulating wealth for the future.

The challenge is to attract these valuable consumers, meet their savings, investment, and credit needs, and provide exceptional customer service. This will result in long-term relationships and a higher ROI for your firm.

Actionable, data-driven solutions to attract the right customers and grow share With so many financial products and services available to today’s consumers, financial marketers need additional data insights to help drive their strategies and focus on high-potential consumers. By using advanced insight on the overall asset and credit picture for prospective and current customers, marketers can support many customer growth initiatives. In part 1 of this 2-part series, we will explore the first three of seven ways for financial marketers to drive customer growth.

Target affluent, highvalue consumers for new investment and banking relationships. If you are looking to expand your customer base for your wealth management or deposit

businesses, then incorporating a more complete view of consumers’ asset potential can help you reach wealthy audiences. For example, target prospects that are likely to hold over $1 million in assets.

Leveraging asset insights (instead of survey information) has helped leading firms steer their prospecting campaigns toward affluent investors and savers.

Expand and refine your lending audiences.

Consumer borrowing is on the rise. But, consumer finances have fluctuated over the past few years due to inflation and job turnover. At the same time, over 77 million consumers have thin files or are unscored. However, lenders have plenty of options to expand their view of consumers’ credit situation to fuel acquisition campaigns, expand access to credit, and better address risk in today’s world.

For example, lenders can refresh their acquisition models with more recent credit data. This could provide a 15 percent lift in performance right from the get-go.* Additionally, lenders can go beyond credit scores to explore data on a household’s likely affluence or that sheds insight on everyday payment behaviors, employment, or income. Gaining a broader view of household credit can help lenders refine audiences while managing risk.

Uncover hidden opportunity to grow wallet share

If a financial marketer could assess its current customer base and capture 1 percent of held-away asset and credit balances, that could translate into millions of dollars. After all, many consumers spread their wealth and their borrowing across multiple firms. This “spread” can be a puzzle for financial marketers.

Adding insight on households’

likely total assets or ability to meet financial commitments to a firm’s own data can open new doors for cross-sell efforts — and help capture both incremental assets as well as low-risk credit balance transfers.

The economy is continuing to fluctuate. Financial marketers are starting to shift priorities and reduce budgets. But, one goal remains a priority for many financial firms. The goal of finding consumers that offer the most potential for their brand. While some consumers are affected by inflation and income stagnation, others continue to spend and invest while offering less risk. These are the consumers that financial marketers can focus on to find and keep.

Maximize the customer experience

Delivering an optimal experience is critical to both attract new customers and keep your best. Financial marketers can use consumer financial insights to recognize best consumers across all channels, deliver premium treatment to highvalue customers, and personalize offers based on financial needs. These efforts can pay off. One bank generated $700 million in new revenue by identifying and reassigning high asset customers to a premium service channel instead of relying on internal data.

Optimize cross-sell to deepen the relationship

Moving customers beyond a single product (i.e. just a deposit customer, just a credit card customer) can be a challenge. By mixing up audience targeting, such as promoting lending products to deposit customers, and gaining more insight on asset potential and portfolio allocation, marketers can deliver the right next-best product offer. One firm used asset insights to segment current customers for a

growth campaign. This enabled the firm to deliver messages based on likely product needs and achieve an over 100 percent lift in deposit, investment, and loan balances.

Act fast to seize in-market customers

seeking credit

Let’s say an existing customer is browsing for a new car loan. If you knew about the search as it was taking place, how would your firm respond? With near real-time alerts, your firm can have the opportunity to deliver a competitive offer and protect market share. Alerts such as this one can be extremely effective to help lenders not only recognize when their customers are seeking additional credit, but also reveal behaviours or events that could lower (or increase) risk.

Drive product activation

To deepen relationships, marketers can take steps to encourage customers to activate and use the products that they hold. 3 steps marketers can use to promote product usage include:

❯ providing continuous product education

❯

incenting spending amongst affluent cardholders

❯ increasing credit limits for segments that are more likely to meet financial obligations.

Young affluent households — offering 3x higher spending power and 20x higher assets as young non-affluent consumers — are a particularly ripe audience for increased education and product activation efforts.

Learn more about how you can gain valuable new customers and build stronger relationships by checking out our eBook.

As Equifax’s Marketing Practice Leader, TODD HOOVER leads a consulting team that enables clients to build best-in-class, data-driven marketing capabilities and programs.

// 17 DMN.CA ❰ DECEMBER 2022

FINANCE DATA INSIGHTS ISTOCK/ NUTHAWUT SOMSUK

Census 2021: Rising Education Levels and Labour Force Activity Changes

BY DR. DOUG NORRIS, PHD

When the seventh and final wave of data from the 2021 Census was released by Statistics Canada, it covered the two main topics of education levels and the labour force. This release also includes data on place of work, commuting patterns and languages spoken at work.

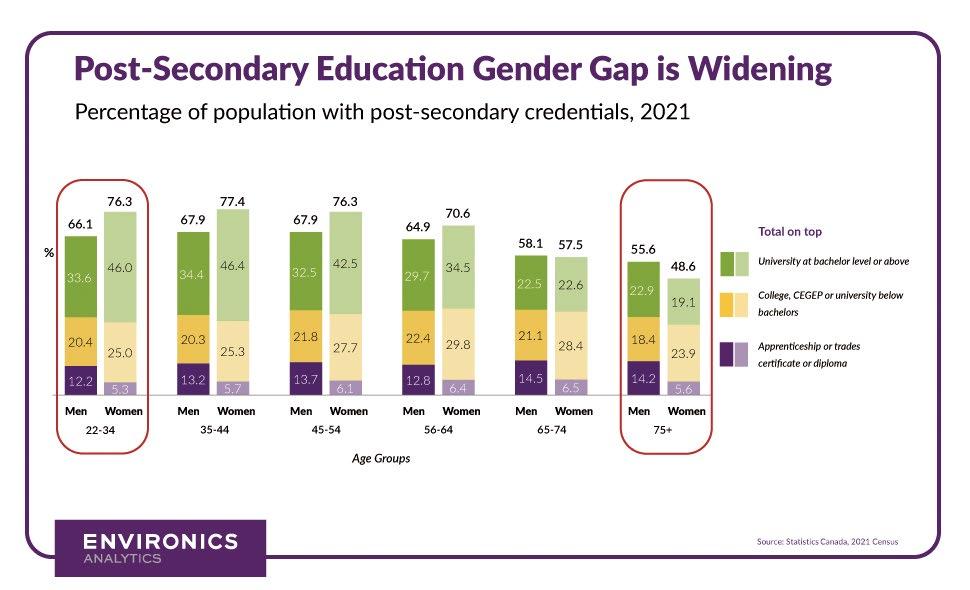

Education levels continue to rise, especially for women Newly released data shows that 67.1 percent of the population aged 25-64 now have a post-secondary degree or diploma compared to 64.8 percent in 2016 and 60.7 percent in 2006.

In 2021, 70 percent of women aged 25-64 had a post-secondary degree or diploma compared to 64.8 percent in 2006. Proportionally fewer men had higher education degrees (64.2 percent) and a smaller increase from 60.9 percent in 2006.

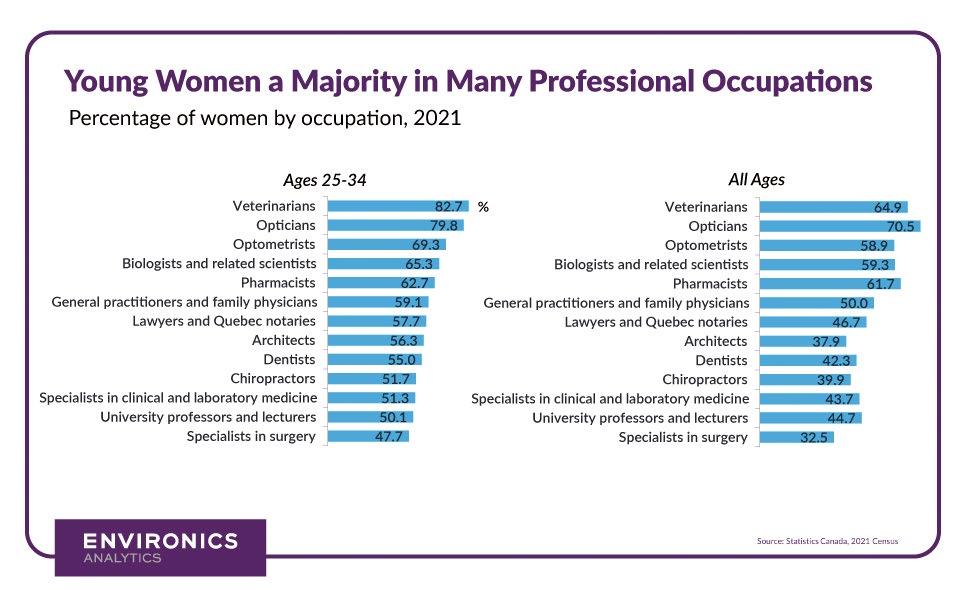

The gender education gap is much more pronounced when you focus on the younger population between the ages 25 and 34. Within this cohort, 76.3 percent of women had a post-secondary degree or diploma, compared with 66.1 percent of men. It’s worth noting that except for the trades, young women aged 25-34 are also a majority of degree holders at all levels, including the earned doctorate.

Stacked bar graphs showing the percentage of men and women in the Canadian population with post-secondary credentials based on the 2021 Census.

Pictured above: stacked bar graphs showing the percentage of men and women in the Canadian population with post-secondary credentials based on the 2021 Census.

Despite the overall increase in education levels, the number of adults with an apprenticeship certificate in the skilled trades decreased from 12.4 percent in 2006 to 10.8 percent in 2016 and to 9.9 percent in 2021. This is a result of fewer young workers replacing retiring baby boomers and contributes to a shortage of workers in some key trades.

And while you will find more women on university campuses, this trend hasn’t found its way to trade schools. Over 80 percent of all apprentice certificates among persons 25-34 are held by men, and the percent of women with an apprenticeship certificate declined slightly from 1.6 percent in 2016 to 1.3 percent in 2021.

The most popular fields of study for young women aged 25

to 34 were health professions and related programs (20.5 percent), business, management, marketing and related support services (19.6 per-cent), followed by education (6.5 percent) and social sciences (4.8 percent). As for males, the most popular fields of study were business, management, marketing and related support services (18.5 per-cent), engineering (10.6 percent), construction trades (8.5 percent) and computer and information sciences and support services (6.6 percent).

By 2021 employment was nearly back to levels in 2016

In the 2021 Census, Canada’s employment numbered 19.3 million, down slightly from 19.5 million in 2016, likely as a result of the pandemic. The overall employment rate in May 2021 was 57.1 percent, also down slightly from five years earlier. The employment rate was 60.9 percent for men and 53.4 percent for women.

According to the monthly Labour Force Survey, employment in 2021 was up from the prepandemic lows in April 2020 and numbers have been slowing increasing since the Census was taken in May 2021.

According to the Census, in May 2021 the unemployment rate was 10.3 percent compared to 7.0 percent in the May 2016 Census. The Labour Force Survey reported the unemployment rate hit a high of 13.8 percent in May 2020, one year before the census. Since the 2021 Census, the unemployment rate gradually declined and reached a near all-time low 5.2 percent in October 2022.

Employment growth was strongest in the service producing industries

From 2016 to 2021, employment gains were highest in professional, scientific and technical services (up 18 percent), health care and social assistance (14 percent) and construction (7.6 percent).

At the time of the Census in May 2021, employment in the accommodation and food services industries had not fully recovered from the pandemic lows and was 16 percent lower than in 2016. However, in the last 18 months since the Census was taken employment continued to grow.

Women gain in many professional occupations, but large numbers are in low paying jobs. Young women are now a majority and women are getting close to a majority overall in many professional occupations.

// 18 ❱ DMN.CA DECEMBER 2022

MARKET TRENDS

BUTENKOW

ISTOCK/

Pictured above: bar chart showing the percentage of women by occupation, ages 25 - 34 vs. all ages, according to the 2021 Census.

In 2021, the top jobs for women were retail salespersons and visual merchandisers (342,000), nurse aides, orderlies and patient service associates (299,000), registered nurses and registered psychiatric nurses (294,000), cashiers (280,000), and food counter attendants and kitchen helpers (251,000).

For men, the top jobs were transport truck drivers (356,000), retail salespersons and visual merchandisers (290,000), retail and wholesale trade managers (231,000), construction trades helpers and labourers (199,000) and material handlers (185,000).

Higher education pays off Employment and unemployment rates varied by the highest level of education. For the working age group 25 to 64, the employment rate was close to 79.4 percent and the unemployment rate was 7.1 percent for those with a postsecondary degree or diploma, compared to 65.8 percent and 11.5 percent for those with only a high school diploma and 51.1 percent and 15.1 percent for those who did not complete high school.

The median annual earnings for persons working full time-full year with a bachelor’s degree was $77,500 compared to those with a college degree ($60,800) and those with only a high school diploma ($51,200). However, it is noteworthy that those with an apprenticeship certificate of qualification in the trades had strong earnings. Their median annual earnings in 2020 ($70,000) were 15 percent more than those

with a college diploma, 37 percent more than those with a high school diploma, but 11 percent less than those with a bachelor’s degree.

Immigrants are highly educated but have lower employment rates and higher unemployment rates

In 2021, 49 percent of immigrants aged 25-54 had a bachelor’s degree or higher compared to 30 percent of the Canadian-born population. The proportion was even higher for recent immigrants (61 percent).

In May 2021, the employment rate for immigrants aged 25-54 was 82 percent compared to 89 percent for the Canadian-born population. The unemployment rate was 7.7 percent for immigrants compared to 4.2 percent for their Canadian born counterparts. The employment rate generally increased and the unemployment rate decreased the longer immigrants had been in Canada. For example, the unemployment rate for recent immigrants was 9.7 percent more than double the rate for immigrants before 1980.

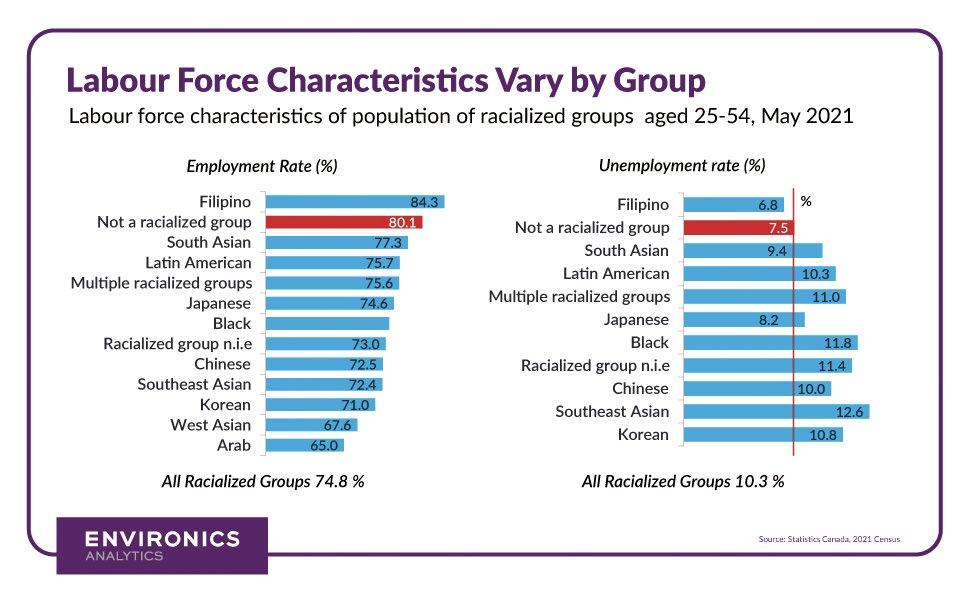

Wide variation in labour force characteristics among racialized population groups There are wide variations in terms of employment and unemployment across the various racialized groups. Overall, the employment rate for the racialized population aged 25-54 was 75 percent compared to 80 percent for the non-racialized population. The unemployment rate for the racialized population was 10.3 percent compared to 7.5 percent for the non-racialized population.

Pictured above: bar chart showing the employment rate

and unemployment rate among racialized groups of the Canadian population according to the 2021 Census.

The population in racialized groups account for 27 percent of the labour force but had higher representation in certain types of occupations. In particular, they accounted for 40 percent of the work-force in STEM occupations (science, technology, engineering and mathematics). They also account for 37 percent of health occupations and 36 percent of occupations in manufacturing and utilities.

Education levels are up for Indigenous People but gaps remain Overall, in 2021, 74 percent of Indigenous persons aged 25-64 had completed high school compared to 89 percent of nonindigenous persons. The rates were 78 percent for the indigenous population living off-reserves but only 55 percent for the on-reserve population. Nearly half of Indigenous persons had a postsecondary degree or diploma — 52 percent off reserve and 32 percent on reserve, compared to 68 percent of the non-indigenous population.

In 2021, the labour force participation rate for the Indigenous population aged 25-64 was 70.6 percent compared to 81 percent for the non-Indigenous population. The rate for the offreserve Indigenous population was 73.3 percent compared to a rate of 56.5 percent for the on-reserve population. The unemployment rate was 16.4 percent for the Indigenous population on reserve and 12.7 percent for the Indigenous population off reserve, compared with an unemployment

rate of 8.4 percent for the nonindigenous population.

Implications for businesses and marketers

The rising education levels revealed in this Census release is a trend marketers will need to watch. For starters, it means marketers need to fact-check their statements as Canadians will be better equipped than ever to evaluate product claims and select the best value for them and their families.

Well-educated young women will need to be a particular focus of marketers. As these women begin their professional careers and families, they will no doubt demand products and services that reflect their more independent and sophisticated lifestyle. And they will be looking for help in juggling their shopping as part of a busy schedule.

With the low growth in the labour force population, immigrants and the Indigenous population will continue to be important sources of labour supply for all organizations. Public- and private-sector employers need to reach out to Indigenous youth to help them gain the education and training required to become members of tomorrow’s workforce. In the case of highly-skilled immigrants, more needs to be done to get quicker approval of credentials.

Over the next decade, the population of young adults between 20 and 29 years old — an important source of entry level labour force — will decline.

Organizations will need to look for new ways to attract this young workforce for their job openings.

// 19 DMN.CA ❰ DECEMBER 2022

DOUG NORRIS, PhD is Senior Vice President and Chief Demographer at Environics Analytics.

MARKET TRENDS

Sustainable Digital Infrastructure: Modernizing Financial Institutions

BY ANDREW EPPICH