THE ESSENTIAL GUIDE BY RAM CHARAN

SPECIAL REPORT The Case for Being Bolder with Satya Nadella, Hubert Joly, Sundar Pichai, Ed Breen, Larry Culp and more PLUS: Jim Farley on His $50 Billion Bet at Ford THE 2022 BEST & WORST STATES FOR BUSINESS: HEARTLAND REVOLUTION! LEADING THROUGH INFLATION

THE VOICE OF AMERICA’S CEO COMMUNITY | SPRING 2022

37,000 financial degrees or certificates awarded annually.

Nearly 40,000 annual STEM graduates. Millions in Fintech education investment.

#1 ranked state for higher education. 380,000+ financial services workers. 285,000+ IT workers.

WITH OVER 80,000 FLORIDA PROFESSIONALS WHO HOLD FINRA LICENSES, FLORIDA IS WHERE YOUR BUSINESS BREAKS THROUGH.

237,000+ high-tech workers.

4th largest high-tech workforce in U.S. #1 High-tech employment in the southeast. 120 commercial banks with $195 billion in assets. 18 international bank headquarters. 4th best test climate. 0% personal income tax.

FINASTRA Lake Mary, FL

EnterpriseFlorida.com

FEATURES

COVER STORY 20 LEADING THROUGH INFLATION

A playbook for every CEO and C-Suite leader looking to help their company prosper—or even survive—in the difficult, uncertain days to come. By Ram Charan

BEST & WORST STATES FOR BUSINESS

38 HEARTLAND REVOLUTION

Long derided as ‘flyover country,’ the nation’s industrial core is again taking flight, thanks to EVs, pragmatic politics, seismic shifts in manufacturing and a deep rethink of the global supply chain. China who?

By

Chief Executive Staff

SPECIAL REPORT: BEING BOLDER

46 INDUSTRIAL REVOLUTIONARY

With a $50 million wager on electric vehicles, Jim Farley has Ford Motor taking its wildest ride—and boldest bets— since the Model T.

By

By

Dale Buss

54 THE CASE FOR BEING BOLDER

How do the best CEOs approach strategy? A new book by three senior McKinsey partners shares insights based on in-depth interviews with 67 of the most successful business leaders of the 21st century.

By

TALENT

62

Carolyn Dewar, Scott Keller and Vikram Malhotra

BATTLING BURNOUT

The employee mental health crisis didn’t start with Covid—and it won’t end with it. A look at how (and why) CEOs are investing in their employees’ peace of mind.

By C.J. Prince

CEO PE SUMMIT

68 LEADING IN THE PRIVATE ARENA

Gathered for Chief Executive’s two-day PE-Backed CEO Summit, PE leadership veterans and experts discussed tactics for addressing the unique tensions of the role. Some takeaways. By Dale Buss

SPRING 2022 No. 314

CONTENTS

20 46 54 38

08

DEPARTMENTS

72 PLANE ADVANTAGE

80 LAST WORD

‘They’re My People’ CEO Vladimir Gendelman’s employees in Ukraine were shelled and shot at, and witnessed unimaginable horrors. Here’s what he did about it. As told to Dan Bigman

Chief Executive (ISSN 0160-4724 & USPS # 431-710), Number 314, Spring 2022. Established in 1977, Chief Executive is published bimonthly by Chief Executive Group LLC at 105 West Park Drive, Brentwood, TN 37027. Wayne Cooper, Executive Chairman, Marshall Cooper, CEO. © Copyright 2021 by Chief Executive Group LLC. All rights reserved. Published and printed in the United States. Reproduction in whole or in part without permission is strictly prohibited. Basic annual subscription rate is $99. U.S. single-copy price is $33. Back issues are $33 each. Periodicals postage paid at Brentwood, TN and additional mailing offices.

POSTMASTER: Send all UAA to CFS. NON-POSTAL AND MILITARY FACILITIES: send address corrections to Chief Executive Group LLC at 105 West Park Drive, Brentwood, TN 37027.

Subscription Customer Service

Chief Executive Group, LLC 105 West Park Drive Brentwood, TN 37027

EDITOR Dan Bigman

MANAGING EDITOR Jennifer Pellet

DIGITAL EDITOR C.J. Prince

ART DIRECTOR Gayle Erickson

PRODUCTION DIRECTOR Rose Sullivan

CHIEF COPY EDITOR Rebecca M. Cooper

CONTRIBUTING EDITORS Dale Buss, Ram Charan, Daniel Fisher, Marshall Goldsmith, Kelly Goldsmith, Patrick Lencioni, Jeffrey Sonnenfeld

EXECUTIVE EDITOR, STRATEGICCXO360 Emily DeNitto

DIGITAL PRODUCER Alessandra Cooper

VP, PUBLISHER, CHIEF EXECUTIVE Christopher J. Chalk | 847-730-3662 cchalk@chiefexecutive.net

DIRECTOR, BUSINESS DEVELOPMENT Lisa Cooper | 203-889-4983 lcooper@chiefexecutive.net

MANAGER, STRATEGIC PARTNERSHIPS Rachel O’Rourke | 615-592-1198 rorourke@chiefexecutive.net

CHIEF EXECUTIVE GROUP

EXECUTIVE CHAIRMAN Wayne Cooper

CHIEF EXECUTIVE OFFICER Marshall Cooper

CHIEF CONTENT OFFICER Dan Bigman

DIRECTOR OF EVENTS & PUBLISHER, CORPORATE BOARD MEMBER Jamie Tassa

VP, PUBLISHER, STRATEGICCXO360.COM KimMarie Hagerty

DIRECTOR OF MARKETING Simon O’Neill

VICE PRESIDENT Kendra Jalbert

HR MANAGER / OFFICE ADMINISTRATOR Patricia Amato

RESEARCH DIRECTOR Melanie Nolen

DATA SERVICES DIRECTOR Jonathan Lee

DIRECTOR, DIGITAL PRODUCTS Leigh Townes

ASSISTANT CONTROLLER Brittney Smith

STAFF ACCOUNTANT Marian Dela Cruz

MARKETING MANAGER Simone Bunsen

EVENTS & MEMBERSHIP MANAGER Rachael Gaffney

EVENTS COORDINATOR KP Wilinson

DATA ANALYST Denise Gilson

CLIENT SUCCESS MANAGER Victoria Campbell

CLIENT SUCCESS COORDINATOR Aftan Walls

STRATEGIC PARTNERSHIPS ASSOCIATE Lara Morrison

RESEARCH ANALYST Isabella Mourgelas

CHIEF EXECUTIVE NETWORK

PRESIDENT Rob Grabill

EXECUTIVE DIRECTOR Chuck Smith

DIRECTOR OF OPERATIONS JoEllen Belcher

MARKETING DIRECTOR Janine O’Dowd

DIRECTOR OF MEMBER SERVICES Brandon McGinnis

SALES SUPPORT ASSOCIATE Brittany Hochradel

P: 615-592-1380 E: subscriptions@chiefexecutive.net W: ChiefExecutive.net/magazine

4 CEO’S NOTE Ukraine Should Be a Wake-Up Call on China 6 RESEARCH Bullying Through Unprecedented Times 8 LEADERS 8 Can Home Be Your HQ? Two years of leading from wherever they happened to be has some CEOs ready to opt out of being

premises—for good. By Dale Buss 12 Law Brief \ Daniel Fisher The PFAS Paradox 14 On Leadership \ Jeffrey Sonnenfeld The Great Global Retreat 16 Coaching Yourself \ Kelly Goldsmith & Marshall Goldsmith Striving for Approval

on

Advancing Aviation Innovations are making private aviation easier to access, more efficient, faster and more comfortable. What’s not to love? By Dale Buss

CONTENTS

get the best of South Florida 10 airports 3 major international 7 private executives & business travelers 2000+ daily flights #1 place for your next business home 200+ corporate, regional & international headquarters AAA bond rating $25 billion in intl trade reach 4 continents in one day world class best business climate Business Facilities 17th Annual Rankings Report (mid-sized metro). business service ranked #2 providers For more information, visit lesstaxing.com or call 800-741-1420

UKRAINE SHOULD BE A WAKE-UP CALL ON CHINA

CEOS REACTED (mostly) admirably to the invasion of Ukraine (with the predictable exception of multiple French conglomerates). Some combination of a sense of justice, sanctions and public shaming forced companies to fold their tents and leave Russia at great expense and pain.

In retrospect, the stew of ingredients that went into Russia’s invasion now seem wholly predictive: the all-powerful dictator of a country with a proud history exploiting nationalism through visions of restored imperial glory; the creation of a cult of personality around an isolated and insulated leader; a corrupt political and economic system that rewards absolute loyalty to the leader; direct threats to a smaller neighbor under flimsy claims of reunification and liberation; a demonstrated willingness to suppress ethnic minorities; the brutal elimination of domestic political opposition and criticism; the destruction of an independent press; actual and de facto state control of critical industries and companies; and the freedom to act geopolitically with near impunity under an umbrella of nuclear weapons.

No Surprises from Here

As we look for lessons from the past few months, the most essential one is this: Every one of these same ingredients exists in China today. But when it comes to China, the stakes and the risks are far larger—and so is the complexity. That’s why it is imperative that CEOs and boards start thinking through how you will potentially navigate a post-China environment sooner than later—if you haven’t already. Anything else would be negligent toward your employees, communities, clients and investors.

It is naïve to downplay the importance of the meeting held just 20 days prior to the invasion between strongmen Putin and Xi. Though the specifics were kept secret, it would not be unreasonable to assume that the dictators—united by the threat by democracy to their power—vowed to support one another diplomatically, politically, militarily and economically in their respective regions of influence, beginning with the capture of Ukraine for Russia and Taiwan for China.

Their official public statement following the meeting laid out a new relationship with “no limits” and a strategic shift “that has far-reaching impact on both China and Russia and the world, and will not waiver in the past, present and future.” The communique also said the two leaders would “strongly support each other in safeguarding sovereignty, security and development interests [and] effectively deal with external interference and regional security threats.”

History teaches us, and Ukraine reminds us, that it is worth taking dictators at their word, and that authoritarian regimes, lacking checks and balances, public squares and passionate feuds are inherently weak, unstable and unpredictable, afraid of their people and prone to doing unpredictable, illogical things. Like invading neighbors.

The best you can do in the face of all this growing uncertainty is to let Russia remind you of what could happen in China. And start now.

—Marshall Cooper, CEO, Chief Executive Group

CHIEF EXECUTIVE OF THE YEAR 2022 SELECTION COMMITTEE

ADAM ARON

President and Chief Executive, AMC

KEN FRAZIER

Executive Chairman Merck & Co. 2021 CEO of the Year

DAN GLASER

President and Chief Executive, Marsh & McLennan

FRED HASSAN

Former Chairman, Bausch & Lomb; Partner, Warburg Pincus

MARILLYN A. HEWSON

Former Chair and Chief Executive, Lockheed Martin 2018 CEO of the Year

TAMARA LUNDGREN

President and Chief Executive, Schnitzer Steel Industries

BRIAN MOYNIHAN

Chairman and Chief Executive, Bank of America 2020 CEO of the Year

ROBERT NARDELLI Chief Executive, XLR-8

THOMAS J. QUINLAN III

Chairman, President and Chief Executive, LSC Communications

JEFFREY SONNENFELD

President and Chief Executive, The Chief Executive Leadership Institute, Yale School of Management

CARMINE DI SIBIO Global Chairman & CEO, EY Exclusive Adviser to the Selection Committee

TED BILILIES, PH.D. Chief Talent Officer, Managing Director, AlixPartners

CONTACT US

Chief Executive Group LLC 105 Westpark Dr., Suite 400 Brentwood, TN

Phone: 203.930.2700 Fax: 203.930.2701 ChiefExecutive.net

LETTERS TO THE EDITOR letters@ChiefExecutive.net

Advertising, Custom Publishing, Events, Roundtables & Conferences

Phone: 847.730.3662 Fax: 847.730.3666 advertising@ChiefExecutive.net

REPRINTS Phone: 203.889.4974

4 / CHIEFEXECUTIVE.NET / SPRING 2022

NOTE

CEO’S

REUTERS / POOL NEWSTOCK.ADOBE.COM

BULLYING THROUGH UNPRECEDENTED TIMES

Insights from Chief Executive Group’s CEO Confidence Index, a widely followed monthly poll of CEOs, including members of the Chief Executive Network (CEN), our nationwide membership organization that helps C-Suite executives improve their effectiveness and gain competitive advantages. For more information, visit ChiefExecutiveNetwork.com.

THE RANGE OF CHALLENGES U.S. BUSINESSES HAVE GONE through in the past two years is mind-boggling. But perhaps more impressive is how America’s CEOs have remained focused and determined to pull through. And not just for the sake of their business, but also for the well-being of employees and communities.

From a global pandemic to social unrest, to talent shortages, to supply chain disruptions, to record-high inflation—and now, a war in Europe. Today’s business leaders have gone through difficulties that very few others, if any, have in such a short span. Yet, you’ve remained optimistic.

When the Iraq war began in 2003, our leading indicator showed CEO confidence dropping to 4.97 on our 10-point scale where 1 is poor and 10 is excellent. This time, the war in Ukraine hasn’t deterred you. In the first days of March, less than a week after the invasion of Ukraine by Russia, our CEO Confidence Index registered a rating of 6.71 out of 10 when looking at business conditions 12 months ahead—and a 6.79/10 when assessing the current environment. Both numbers were up month-over-month.

Let’s be clear, though: CEOs are not shrugging the war off, but many point to the resounding unity of the West in its response to condemn Russia and Putin’s actions as a signal for a global recovery. With Covid now nearly in the rear-view mirror and demand remaining strong, CEOs are hopeful, and worries over inflation and the supply chain are outshined by hope that a year down the line, the pandemic and the host of challenges it sparked will be largely controlled.

As one CEO put it: “Consumers have funds and jobs and are spending. Pent-up demand, especially for travel and entertainment, will hit as the world opens up in the new ‘post-pandemic’ world.”

—Melanie Nolen, Research Editor, and Isabella Mourgelas, Research Analyst

CEO FORECAST OF BUSINESS CONDITIONS 12 MONTHS FROM NOW

ARKANSAS ECONOMIC DEVELOPMENT COMMISSION arkansasedc.com 33

CORPORATE BOARD MEMBER NETWORK boardmember.com/cbmnetwork 61

CEO AND SENIOR EXECUTIVE COMPENSATION REPORT FOR PRIVATE COMPANIES chiefexecutive.net/compreport 71

CEO 100 chiefexecutivenetwork.com/ceo100 51

CHIEF EXECUTIVE NETWORK chiefexecutivenetwork.com 53

COLORADO OFFICE OF ECONOMIC DEVELOPMENT & INTERNATIONAL TRADE choosecolorado.com 17

DELOITTE LOCATION SERVICES www.deloitte.com 18, 19

ENTERPRISE FLORIDA enterpriseflorida.com INSIDE FRONT COVER GREATER FORT LAUDERDALE ALLIANCE lesstaxing.com 3 JOBSOHIO jobsohio.com OUTSIDE BACK COVER

LEADERSHIP CONFERENCE chiefexecutive.net/leadershipconference 49

LOUISIANA Economicopportunitylouisiana.com/ 15

MELMARK melmark.org 34, 35

MICHIGAN ECONOMIC DEVELOPMENT CORPORATION michiganbusiness.org/pure-opportunity 11

MISSOURI ONE START MissouriOneStart.com 5

NICHOLAS AIR NicholasAir.com INSIDE BACK COVER, 74-78

SMART MANUFACTURING SUMMIT chiefexecutive.net/smartmanufacturingsummit 7

SQUEEZE MEDIA squeezemedia.com/ 47

TENNESSEE DEPARTMENT OF ECONOMIC AND COMMUNITY DEVELOPMENT tnecd.com 13

TEXAS ECONOMIC DEVELOPMENT CORPORATION businessintexas.com 31

TOYOTA WAY likerleanadvisors.com/ 45

WINDSTREAM ENTERPRISE windstreamenterprise.com 25

6 / CHIEFEXECUTIVE.NET / SPRING 2022 March Feb. Jan. ’22 Dec. Nov. Oct. Sept. Aug. July June May April March ’21

7.27 7.27 6.77

6.61 6.36

CHIEF EXECUTIVE RESEARCH

7.08 7.18 6.89

6.72

6.50 6.95 6.63 6.71

AD

INDEX

Chief Executive’s CEO Confidence Index is measured on a scale of 1-10.

Save $200 when you register online by May 13. Use code: CEOMay100 Learn more and register: ChiefExecutive.net/SmartManufacturingSummit DANILO AMORETTY Carhartt Senior Vice President of Global Product Supply and Operations Surviving the Great Supply Chain-Inflation Tsunami Smarter Design, Smarter Marketing SHANNON WASHBURN Shinola Chief Executive Officer TOM KELLY Automation Alley Executive Director and CEO Winning at Automation ASAP Winning the Talent War Now COREY STOWELL Webasto America Chief Human Resources Officer JEFF LIKER Bestselling Author of The Toyota Way Renowned global expert on Lean Manufacturing and Just-In-Time Just-in-Time to Tackle Today’s Supply Chain Crisis Inside Ford’s EV Revolution JOHN SAVONA Ford Motor Company Vice President, Manufacturing and Labor Affairs Tested Solutions For Today’s Most Urgent Challenges Featuring: Exclusive Behindthe-Scenes Tour Ford Rouge Electric Vehicle Center MAY 17-18, 2022 | DETROIT, MI SMART MANUFACTURING SUMMIT

LEADERS

CAN HOME BE YOUR HQ?

years of leading from wherever they happened to be has some CEOs ready to opt out of being on premises—for good. BY

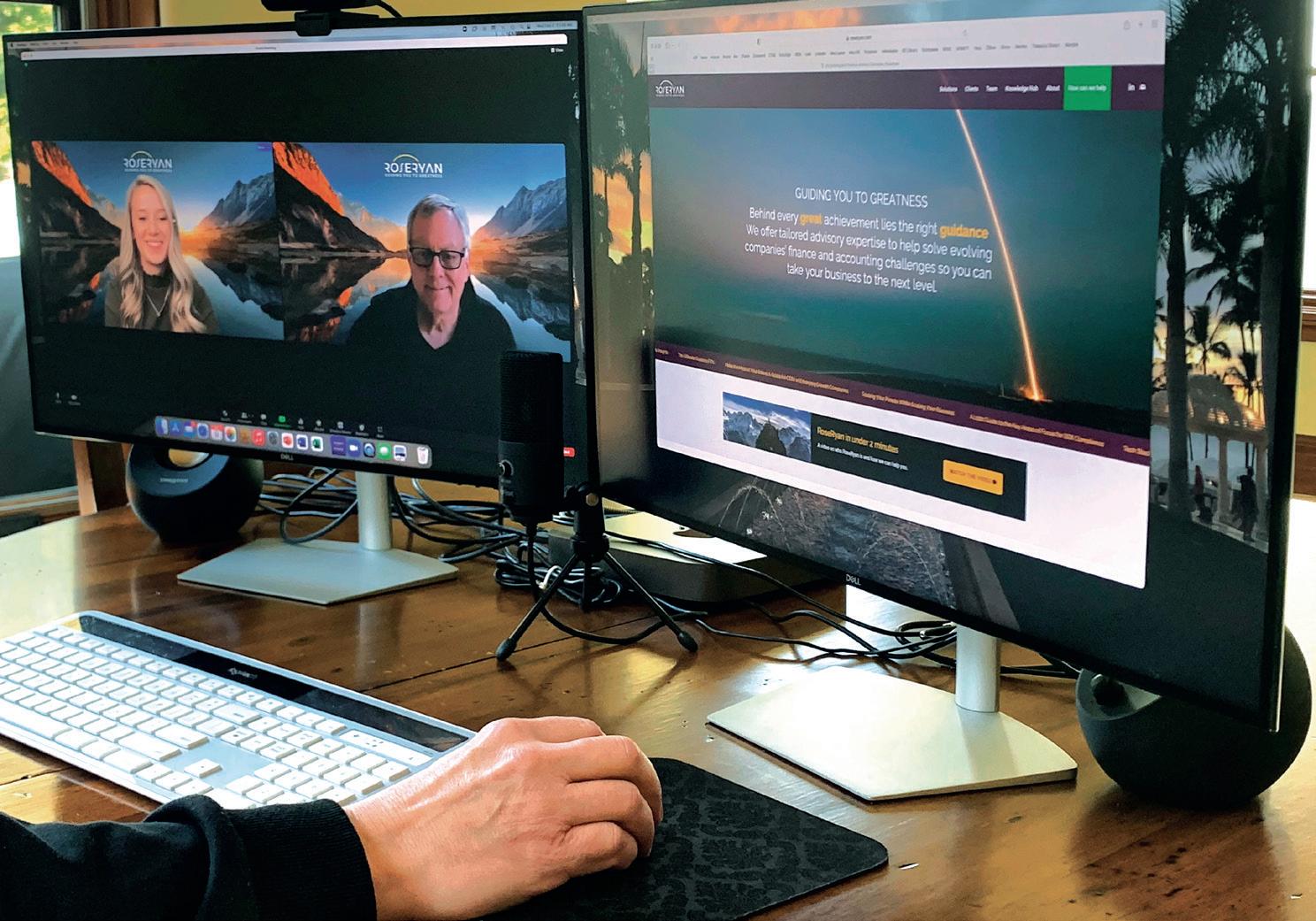

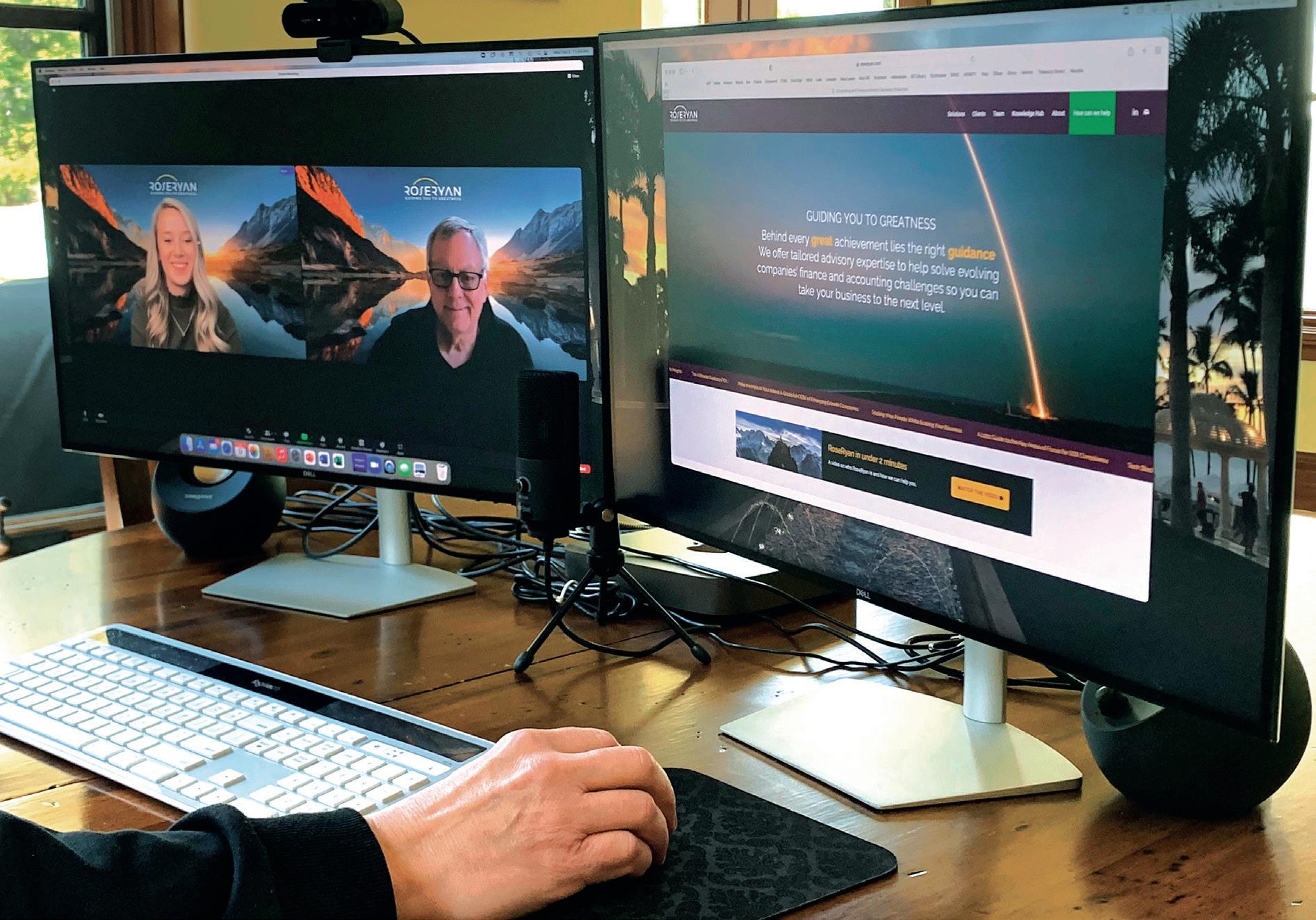

DAVID ROBERSON SPENT A MONTH running RoseRyan from Hawaii last year, and now the CEO is overseeing the entire accounting and financial services firm from a guesthouse in the backyard of his home in Silicon Valley. The website still cites an address on Bascom Avenue in nearby Campbell, California, but nobody works there anymore, and Roberson toils permanently amid redwoods, olive trees, roses and diffused sunlight a few yards from his patio.

“Historically, as CEO you had to be where the business was,” says Roberson, who was CEO of Hitachi Data Systems before joining RoseRyan as a vice president in 2018 and becoming chief a year later. “But these days, I don’t think anyone cares where you live, to some degree. I just hired a chief of staff, and she’s in Dallas, and she only asked: ‘What hours do you want me to work?’ I said, ‘Same as mine, and we’ll be just fine.’”

Is Roberson right? Company chiefs always have been rovers, routinely traveling to meet with customers, lenders, politicians, suppliers and employees at far-flung operations. Digital communications loosened their ties to the corner office. Then, the pandemic blew the lid off the entire arrangement, forcing a remote management structure for most companies—and proving in most cases that it could work.

Now CEOs and boards are facing the important question of whether top leaders should go back to the physical C-Suite, even as this same group is also grappling with restructuring execution and culture around permanent work from home by many or most of their employees.

DALE BUSS

“Culture is becoming increasingly important, and the workplace is where culture is manifested,” says Sanjay Rishi, Americas CEO of JLL Work Dynamics. “But it’s a retention tool for companies to give some level of flexibility, and the tone from the top is extremely important. There’s so much moving around that there’s no one answer to any of this.”

For some, domicile has become a big factor in CEO recruiting. “Physical relocations can still be difficult, and that prospect can deter an attractive candidate,” says Peter Crist, chairman of the Crist/Kolder executive-search firm. “And if that occurs, companies need to be quick to have that as an important early-conversation tactic.”

In broad ways, the issue has arisen before, but usually in terms of potential abuse. For example, in 2007, amid the automaker’s steep financial losses, senior Ford Motor executive Mark Fields gave up the use of a corporate jet for his frequent trips from the company’s Michigan home to Florida. (Fields overcame that controversy to become Ford’s CEO in 2014, only to face ouster in 2017.)

The pandemic fueled speculation about whether a company’s headquarters can simply be where a CEO lives and whether it still matters where some enterprises are formally “based.” Still, having companies and their C-Suite offices in the same place remains the norm. Just ask Kellogg’s. CEO Steven Cahillane’s purchase of a $6 million mansion in Chicago’s Lincoln Park neighborhood, followed by Chief Growth Officer Monica McGurk buying a $2 million home several miles north in Winnetka, Illinois set off rumors that

8 / CHIEFEXECUTIVE.NET / SPRING 2022

Two

the cereal maker was moving its headquarters to Chicago from iconic Battle Creek, Michigan. A company spokeswoman declined to comment on the issue to Chief Executive, but Kellogg’s has stated in the past that it’s staying put.

While having leadership on site remains the norm, the past two years of experimentation with remote work have raised the question of whether it’s necessary. For some, the answer is a resounding yes. “I’m opposed to commuter relationships or a distributed-management structure,” Crist says. “That always ends poorly, in my mind. The physical proximity of the top two or three players, maybe five, is really important.”

Hyliion CEO Thomas Healy believes it’s crucial for him to work on premises, where engineers and others are tinkering with the electric-locomotion systems for trucks being made by his Austin-based startup. He’s “primarily in the office,” Healy says, and so are his other top leaders, even as Hyliion allows most of its other 200 employees some work-from-home flexibility. “If I worked from home multiple days a week, or all the

time, that would disconnect me from the organization and create a divide between operations and the rest of the staff,” he says. Others, however, demur. Lizzie Horvitz founded Finch, a digital outfit that scores other companies’ products for ESG performance, during Covid and has never worked side-byside with any of her employees. After running the startup from her bedroom at her parents’ house in New York City and from a condo in Wyoming where she was skiing, she’s now steering it from her home in Denver. Horvitz has no plans to get a formal office.

“Never say never, but I wouldn’t want to have to let people go if they don’t want to move,” Horvitz says. “I don’t think we’ll be in the same place for the foreseeable future.”

Separate locales for leadership and team members is also the plan at Intradiem, a call-center software company headquartered in Alpharetta, Georgia. Halfway through Covid, CEO Matt McConnell sold his house in suburban Atlanta and permanently decamped to Atlantic Beach, Florida. “I’d already traveled a fair amount, so I already could work where I was,” he

CEO MAGAZINE / SPRING 2022 / 9

RoseRyan CEO Dave Roberson now leads his company from a guesthouse in the backyard of his Silicon Valley home.

says. “We announced in January that we’re a remote-first company and shifted to a remote-first culture, and we’re still defining it.”

For leaders weighing CEO domicile decisions, here are some factors to consider:

Size and place matter. The smaller the company, of course, the easier for a CEO to chuck the office. “We work with Fortune 500 and Russell 2000 companies, and I haven’t had one CEO suggest he or she is thinking about running the company remotely,” Rishi says.

And if a company is outside big-city corridors or tax-haven states, Crist says, directors now “might get pushback like, ‘My family isn’t going to go there.’ Only a small minority love Omaha or have family there.”

Beware the pitfalls. Every student of the workplace is examining companies’ post-pandemic performance to see whether less physical proximity and interaction translate into less or more productivity, and less or more innovation.

“Creating a culture when you’re a remote company is a real challenge,” says Joel Warady, CEO of Catalina Crunch, a snack company based in Indianapolis, who joined as CEO two years ago and has continued to run the company from his home in Chicago. He hadn’t even met most of his direct reports as of the first quarter of this year. “I don’t think any of us are experts at it. There’s a lot of trial happening.”

There is one big question especially for CEOs and directors: How does succession at the top work in an all-remote environment? “You need eyeball-to-eyeball interaction,” Rishi argues. “How can you do succession planning and mentorship and training when you’re remote? How do you tell how your top people react under pressure?”

Corral the C-Suite. Untethered CEOs must continually coordinate with top lieutenants with whom they used to share offices every day. “We met every week in person; now we meet every week on Zoom,” Roberson says. “Our meetings are just as

effective, and our business is thriving right now in a totally remote environment.”

Overcommunicate. Staying in touch with rank-and-file employees is arguably even more important now than it was during Covid, particularly for chiefs who decided on a permanent distributed-leadership model. McConnell alternates a virtual “town hall” meeting with all employees one week with a video he records the next week and puts out there for employee responses.

Warady is “a big user of text messaging, saying, ‘Do you have a minute?’, sort of like we used to be able to grab a cup of coffee with someone and just run ideas by them.” When he dials up direct reports, he says, “I try to spend the first 10 minutes of one-onones talking about personal things rather than business issues.”

Consider the legalities. Should a chief of a U.S.-based company want to work primarily in, say, Galway, Ireland, foreign tax rules are likely to kick in, and that may affect the entire company’s legal domicile, says William Wright of the Fisher Phillips law firm. “The consequences for a CEO sometimes can be very painful, so it needs to be thought about.”

Even toggling between U.S. locales can be tricky for CEOs. For example, one complication of the increasingly popular departure of company chiefs from New York City to Florida is that New York lodges city taxes against individuals who spend more than 183 days a year there. “You can’t just be saying, ‘I was in Florida,’” says Nishant Mittal, senior vice president and general manager of business travel at Topia, a software company with a program that helps executives track their whereabouts and expenses. “There needs to be clear and convincing evidence.”

As for where all of this is headed: Crist recognizes that the remote CEO model is legitimate. But be believes “there will come a time when proximity will be very important again. I can sense it in the dialogue I have with boards and CEOs. Whenever this stuff goes away, we’ll try to get back to what we would define as normal.” CE

10 / CHIEFEXECUTIVE.NET / SPRING 2022 LEADERS

“Creating a culture when you’re a remote company is a real challenge. I don’t think any of us are experts at it. There’s a lot of trial happening.”

NINA GROOMS LEE

Chief Product Officer, May Mobility

Chief Product Officer, May Mobility

“THE FUTURE OF MOBILITY WILL BE SHAPED IN MICHIGAN.”

Dreaming. Innovating. Growing. It's how Michigan talent is making an impact on the world in key industries. From tech to mobility to advanced manufacturing, there's a different kind of hustle here. Expand your business in Michigan and get access to support, camaraderie and new opportunities.

Make the move at michiganbusiness.org/pure-opportunity

LAW BRIEF \ DANIEL FISHER

THE PFAS PARADOX

ON A BRIGHT, SUNNY MORNING ON July 29, 1967, the aircraft carrier USS Forrestal was on station off the coast of Vietnam when an underwing rocket accidentally launched from an F-4 fighter-bomber, streaking across the deck toward another jet piloted by future U.S. Senator John McCain. Shrapnel from the exploding rocket ignited the fuel in McCain’s jet as well as another one next to it.

manufacturers and the local airport. It has even prompted litigation squared: Municipal water systems hit with lawsuits over PFAS contamination by their customers are installing expensive filtration equipment and then suing airports and even the U.S. military to recover their costs.

The governmentrequired “forever chemical” spawns an endless wave of litigation.

McCain and the other pilot escaped their planes, but the expanding pool of burning fuel set off a chain reaction of fire and explosions that eventually penetrated the Forrestal’s flight deck, killing 134 sailors and nearly sending the carrier to the bottom. Investigators blamed obsolete WW II–era bombs and water fire extinguishers that washed away more effective foam.

In the wake of the Forrestal disaster, the U.S. Department of Defense adopted MIL-F-24385, requiring the use of “aqueous film-forming foam,” or AFFF, based on fluorocarbon compounds originally developed by 3M in the 1940s. The following year, the Federal Aviation Administration adopted the same military specification for civilian airports, eventually ordering them to conduct live exercises twice a year, including spraying firefighting foam over the runways.

That lifesaving regulation is now responsible for a growing wave of litigation, including a proposed class action on behalf of virtually everyone in the U.S. Unfortunately, the fluorocarbons that transform ordinary water into an oxygen-blocking firefighting blanket also break down into compounds known as PFOS and PFAS, extraordinarily durable molecules that have leached into water systems and persist in human tissue for decades.

All of which raises the question: Can it be a tort to use a chemical that is required by government regulation? A federal judge in South Carolina overseeing thousands of PFAS lawsuits is pondering that question right now, as some defendants press the “government contractor defense,” arguing they can’t be sued for following the rules.

“The defense is basically ‘the government made me do it,’” says Brian Gross, a partner with MG+M in Boston who’s active in toxic-tort defense. “‘I didn’t have a choice. There was no wiggle room.’”

Plaintiff lawyers argue the law doesn’t specify PFAS, only fluorocarbons. But defendants say the exacting specifications in MIL-F-24385 left them no choice but to use the chemicals they are now being sued over. They’re hoping a precedent set in litigation over another Vietnam-era chemical, Agent Orange, will protect them this time. In that case, Dow Chemical and Monsanto won rulings dismissing plaintiff lawsuits because they made the herbicide to exacting government specifications.

One critical difference is that those companies made Agent Orange under contracts that spelled out the chemical formula. 3M has failed to dismiss similar litigation over military earplugs because the military bought a design that 3M developed on its own. Firefighting foam is somewhere in the middle.

Daniel Fisher, a former senior editor at Forbes, has covered legal affairs for two decades.

Advanced technology now allows scientists to detect PFAS down to parts per trillion. Plaintiff lawyers were quick to use that breakthrough to file lawsuits against everyone who touched the stuff, from chemical companies like DuPont and 3M to product

Another factor might help defendants, at least in lawsuits by individual plaintiffs. Because PFAS is everywhere and is only weakly associated with a variety of conditions, it will be hard for them to prove any one company’s products made them sick.

“PFAS is ubiquitous,” Gross says. “It makes specific causation difficult.” CE

12 / CHIEFEXECUTIVE.NET / SPRING 2022 LEADERS

THE CHARGE

WE’RE POWERING A NEW ERA OF AUTOMOTIVE MANUFACTURING TENNESSEE WILL SOON BE HOME TO FORD’S BLUE OVAL CITY—THE LARGEST, MOST ADVANCED, AND MOST EFFICIENT AUTOMOTIVE PRODUCTION CAMPUS IN ITS 118-YEAR HISTORY. welcome to tennessee

LEADING

TENNESSEE IS

ON LEADERSHIP \ JEFFREY SONNENFELD

THE GREAT GLOBAL RETREAT

COCA-COLA CEO Roberto Goizueta’s motto was “Think Global, Act Local.” Confused by this message, one of his successors, Doug Daft, changed it to “Think Local, Act Local.” Does either apply now?

In 1965, media philosopher Marshall McLuhan coined the term “the global village.” That was 40 years before New York Times columnist Tom Friedman celebrated global interdependency in his 2005 book, The World Is Flat. In fact, in 1996, Friedman even more optimistically proclaimed that no two nations that both had McDonald’s franchises would wage war. Sadly, that wasn’t true in Africa, the Middle East or Central Europe back when he wrote it, and the 110 McDonald’s restaurants in Ukraine and 860 McDonald’s in Russia underscore just how naive the sentiment remains today.

BlackRock CEO Larry Fink recently remarked on the fizzling of the era of globalization in his firm’s annual report. “The Russian invasion of Ukraine has put an end to the globalization we have experienced over the last three decades,” he wrote.

supplies, semiconductors, antibiotics, battery components and other vital materials, business leaders like Fink are calling for a return to more self-reliance. At a Yale CEO Caucus held in March, 73 percent of multinational CEOs agreed with the statement, “I am rethinking my company’s global strategy given geopolitical turbulence.” Seventy-six percent agreed with “I am concerned about my company’s dependence on global supply chains.”

At the same time, the importance of global markets and the dependence upon natural resources outside this nation cannot be denied. Stanley Black & Decker CEO Jim Loree complained this fall that supply chain clogging almost tripled his trapped in-transit inventory.

Thus, the implications are: Regional free-trade pacts: “Engage with your allies,” advises Lance Fritz, CEO of Union Pacific. “Trade supports 41 million jobs in the U.S., a great source of economic might for us and a great counter [to the] global behavior of China and Russia… The Indo-Pacific economic framework is a great starting point.”

Jeffrey Sonnenfeld is senior associate dean, leadership studies, Lester Crown professor in management practice at Yale School of Management, president of the Yale Chief Executive Leadership Institute and author of The Hero’s Farewell. Follow him on Twitter @JeffSonnenfeld.

This sudden shift in sentiment has come as something of a shock to business leaders and CEOs, given that the promotion of business economic interdependence beyond simple mercantile colonization has been a steady drumbeat since economist David Ricardo’s theory of comparative advantage. His 1817 classical treatise formalized the theory of comparative advantage. Ricardo argued that free trade between two or more countries can be mutually beneficial, presuming all bring their most efficiently produced goods and services to global markets—not anticipating predatory tactics, wars, political restrictions and pandemics.

A backlash was most dramatically demonstrated in the mass street protests at the 1999 World Trade Organization’s conference in Seattle, called the Battle of Seattle. That 60,000-person protest was a coalition of labor organizations, media activists and NGOs. Now, in the aftermath of supply-chain disruptions, the loss of access to secure energy

Redundancy: With just-in-time source moving to just-in-case with both duplication and flexibility for rerouting paths, Yale operations expert Sang Kim warns, “Since most supply chains are optimized for efficiency, there is not much room for significant errors, which are magnified in the stretched, globalized supply chains that we have today… Building flexibility, such as rerouting production capacity to certain goods at the expense of others, is a more cost-effective solution.”

Reconceptualizing realities: To generations who did not lead during Cold War times, it may be hard to recognize that global brands may no longer be the bridge to world harmony, as economic globalization advocates once proselytized.

At the 1997 funeral of Coke CEO Goizueta, a fervent globalist, the recessional featured the Grammy-winning song “I’d Like to Teach the World to Sing (In Perfect Harmony),” recalling smiling young people of different nationalities, each holding a Coke. Their chorus chants, “It’s the real thing.” Really?

14 / CHIEFEXECUTIVE.NET / SPRING 2022 LEADERS

CE

Accepted for decades, the interdependency of nations is now in question.

COACHING YOURSELF \ KELLY GOLDSMITH & MARSHALL GOLDSMITH

STRIVING FOR APPROVAL

WE ALL STRIVE FOR approval in one way or another.

As human beings, from our time in caves, through our experience with royalty, through our careers in modern organizations, we have learned that our success is directly related to gaining the approval of key stakeholders—often the people in power.

As young people, we seek approval from our parents before we even learn to speak. We strive for approval from our peers. We need approval from our teachers as we take test after test after test.

Yet, when we Google “need for approval,” the results often describe a psychological disorder. They suggest that seeking approval is somehow dysfunctional. When is it normal and useful to prove ourselves to others, and when it a waste of time—or even worse?

Not surprisingly, the renown consultant and author Peter Drucker provides a great answer. Drucker said, “We are here on Earth to make a positive difference, not to prove how smart or right we are.”

it doesn’t.

Yet, after years and years of proving ourselves, it can be hard to stop.

Right Doesn’t Warrant Might

Kelly Goldsmith is a professor of marketing at Vanderbilt University’s Owen Graduate School of Management.

Marshall Goldsmith has been ranked as the world’s #1 leadership thinker and coach. His 44 books include the New York Times bestsellers What Got You Here Won’t Get You There, Triggers and MOJO

My [Marshall’s] book, What Got You Here Won’t Get You There, is primarily focused on the challenges of successful leaders who focus too much on proving themselves (such as “winning too much” or “adding too much value”). They “oversell” themselves.

One former CEO I coached noted, “When I became the CEO, my suggestions became orders”—even when they made no sense. When asked what he learned from coaching, he replied, “Before trying to prove my point, do not just ask, ‘Am I correct?’ Also ask, ‘Is it worth it’?’”

He went on to say, “When I asked myself these questions, I often concluded, am I right? Maybe. Is it worth it? No.”

trying to prove you are right, and ask: “Is my comment going to do more good than harm?” Be ready to let it go.

In our work with coaches, we often find professionals who have the opposite problem. They undersell themselves. They hold back and “hide their light under a bushel.” They may think, “I should not need to prove myself. My good work should speak for itself.” If this were true, no company would need a marketing department!

When we work with people who undersell themselves, we ask: If you were more influential, would the world be a better place? Then we ask: ‘Are you uncomfortable trying to prove yourself and becoming more influential?

After getting two votes for “yes,” we given them a challenge: “Which is more important to you, making the world a better place or your own comfort?” They quickly realize that, in some cases, proving themselves is necessary to help make the world a better place.

Credibility has to be earned twice: 1) being excellent at what we do and 2) being recognized for our excellence. Being excellent at what we do and not being recognized for it is equivalent to writing an amazing book that no one reads.

At the individual level, building credibility requires both doing great work and being recognized for what you do. The same principle applies to your organization. Your company’s credibility requires both doing great work and being recognized for what you do.

As coaches, we have two suggestions for you as a CEO:

1) Coach your people who “oversell.” Help them learn to fight the instinct to prove themselves when it is not making a positive difference for the organization.

As a CEO, learn to take a breath before CE

2) Coach your people who “undersell.” Help them learn that gaining approval for themselves and their work can help them make a positive difference for the organization.

16 / CHIEFEXECUTIVE.NET / SPRING 2021 LEADERS

Proving ourselves to others makes us more effective leaders—except when

PROXIMITY TO MARKETS

Colorado’s central geographic location creates an ease of doing business not only in the U.S. and American markets, but also means Europe and Asia are equally accessible. Colorado’s Mountain Time zone allows for same day communication with both U.S. coasts, Europe, South America, and Asia.

Colorado is a hub for advanced and emerging industries including aerospace, quantum technologies, biotechnology and

EDGE INDUSTRIES Colorado o ers big city amenities throughout the state, with the highest number of resident participation in the arts, miles of hiking and biking trails, skiing, dining options,

major sports teams and

that

every

adventure.

OF LIFE Visit choosecolorado.com to learn how Colorado can be your next business location.

more. CUTTING

five

more

makes

day an

QUALITY

How Is ESG Impacting Location Selection?

BY MATT SZUHAJ, TARA NICHOLSON AND MALVIKA PRADHAN

DEMOGRAPHIC DATA, THE POLITICAL ENVIRONMENT and environmental considerations have long been part of the location selection calculus. However, over the past several years, Environmental, Social and Governance (ESG) criteria have become critical to assessing the sustainability of investment decisions for many corporations.

• Companies are thinking more about the environmental impact of their location decisions—prioritizing access to public transport and bike paths, analyzing how much plane travel will be routinely required, considering the importance of LEED-certified buildings, weighing the impact of their operation on the local environment.

• When selecting locations, companies are now carefully considering how local regulations could impact the company’s reputation and weighing the potential risks associated with geopolitics on the global stage.

• The broader social environment is increasingly considered a critical location factor as companies prioritize where they want to be based on the level of openness and diversity.

The reason for this intensified focus on ESG criteria? The talent companies are looking to hire and retain are increasingly focused on corporations’ policies and accountability. People want to work for companies that prioritize corporate sustainability goals, and they are voting with their feet.

In addition, locations selected using ESG criteria will be more resilient to the adverse impacts of both climate change and the nature crisis, which are key considerations for organizations that will only grow in importance. An approach to incorporating the philosophy of ESG into location selection methodology can be the framework of Transformational Drivers comprising three pillars—Planet, People and Progression. Assessing locations’ performance on the Transformational Drivers in addition to the traditional critical location factors (costs and conditions) studied provides a more nuanced view of a market’s mid- to long-term suitability for investment. Some examples of this combined analysis are:

• Planet (Climate Change Adaptation) + Operating Costs: Locations could see their cost advantage being eroded due to the financial implications of poor mitigation and adaptation to climate risks, for example, increased capital costs, increased utility costs, loss due to business disruptions, damages to property, investments to mitigate the danger to personnel, etc.

• Planet and Progression + Operating Conditions (Risk): It is important to assess a location’s risk of natural disasters and its vulnerability, as well as adaptation to climate change, since the risks are linked. As per the IPCC Sixth Assessment Report, multiple climatic and non-climatic risks can interact, resulting in compounding overall risk and risks.1 For example, climate change can increase the frequency and intensity of floods, while poorly planned urban development can render a location vulnerable to flash floods caused by climate change-induced heavy rainfall.

• People and Operating Conditions (Talent Availability): A location that performs regarding People can, in turn, improve the quality and availability of its labor pool, a key traditional critical location factor, by not only attracting qualified talent but also enhancing the quality and sustainability of its existing workforce.

• People and Progression + Operating Conditions (Risk): Assessing the location’s performance on both the People and Progression drivers, as well as its Risk profile, will allow an organization to gain insights into its potential political and social stability, since increasing discrimination against groups of people could lead to unrest.

Planet: This pillar allows an assessment of the location’s ability to mitigate and adapt to the impact of both climate change and the biodiversity crisis. This is relevant for footprint decisions due to the detrimental impact on human wellbeing, as well as financial costs (both day-to-day and one-time) of the physical risks associated with climate change. For example, a 2021 Swiss Re report predicts that global property catastrophe premiums are set to increase up to 41 percent (USD 183 billion) by 2040 due to climate risk, with USD 110 billion coming from advanced markets.2

Locations that have successfully combined climate resilience and environmental considerations with development will be able to offer a better quality of life, making them attractive relocation destinations for talent. An organization that chooses to invest in such locations will not only likely be able to successfully attract talent for in-office roles but also be able to demonstrate tangible action on an issue important to today’s workforce—sustainability. This could form a key piece of the organization’s employer branding strategy.

When measuring a location’s performance regarding Planet, it will be helpful to answer the following questions:

• What are the acute and chronic risks faced on account of climate change? What measures have been taken to mitigate and adapt to these risks?

• Is there a strategy or roadmap to transition to green infrastructure and renewable energy? What is the stated horizon, and how has the implementation progressed?

• Does the location face a risk of water scarcity? Does the community have access to safe drinking water and sanitation, both of which are crucial to human health and well-being?

• What is the air quality given that it has a documented impact on health and wellbeing? An estimated 7 million people die each year due to air pollution3

• With green cover serving as a carbon sink, as well as being an indicator of social equity, how well is the location conserving its biodiversity and green space?

THOUGHT LEADERSHIP PROVIDED BY DELOITTE CONSULTING LLP

People: Talent guides real estate decisions. By measuring a location’s performance on key social issues, we can gain insights into long-term attractiveness for talent. The community an organization chooses to invest in not only impacts its ability to meet its diversity, equity and inclusion goals but can also form a part of its employer branding, helping it distinguish itself when competing for talent.

When measuring a location’s performance regarding People, it will be helpful to answer the following questions:

• How inclusive is the community? To what extent are the LGBTQ+ community, ethnic minorities, immigrants accepted? What is the level of religious tolerance?

• What is the level of economic inclusion? How easily are economic opportunities available to social groups?

• How does the location fare on gender equality?

• Since access to education and healthcare are some of the primary non-financial metrics to evaluate social well-being and equality, how does the location fare on these metrics?

A focus on people is essential, not only to be able to attract talent but also from a branding perspective. A women-focused brand, for example, would find it challenging to justify investment in a location that discriminates against them through restrictive healthcare regulations.

On occasion, organizations have sent a clear message regarding their stance on pressing diversity, equity and inclusion issues through their location decisions, such as a large financial services organization choosing not to locate in American states that had passed restrictive gender identification regulations.

Progression: While the metrics measured in the first two pillars provide information at a given point in time, the third pillar, Progression, assesses trends. This provides critical insights into the governance aspect of ESG by measuring the scope and effectiveness of regulations and policy interventions. This, in turn, will help organizations to identify the location’s trajectory, spot fundamental shifts in underlying dynamics and assess whether the location will be able to support their growth and long-term strategy.

When measuring a location’s performance regarding Progression, it will be helpful to answer the following questions:

Sources:

1. https://www.ipcc.ch/report/ar6/wg2/resources/spm-headline-statements/ 2. https://www.swissre.com/risk-knowledge/building-societal-resilience/growing-riskinsurance-industry-crucial-role.html

• How much progress has the location made in building climate resilience and mitigating risk?

• What are the dynamics underpinning attitudes towards various demographics, and how have they been evolving?

• Have levels of social tolerance and trust in institutions varied, and in what way? What are the underlying causes, and will they result in lasting change?

• Are innovations and technologies being adopted to strengthen the location’s performance regarding environmental and social issues?

When assessing progression metrics, it is important to keep in mind that certain locations have made significant progress prior to the time periods being assessed. In such instances, their progress will now only be incremental. To ensure an accurate analysis, such locations must not be unfairly penalized. For example, Singapore has seen only a marginal improvement in its 10-year performance in the area of sanitation and drinking water as compared to Malaysia. However, it is important to note that Singapore had already significantly improved the quality of this metric in prior years, to the extent that now only marginal improvements are possible.4

Locations should be compared at a regional level on account of the difference in the availability, granularity and reliability of data. It is also important to note that given the continuously evolving nature of the ESG landscape, new data and perspectives will soon be available, allowing for an increasingly nuanced analysis.

In order to compete for talent and make informed location decisions, traditional factors alone will not be sufficient. An organization must supplement its ESG policies with an understanding of transformational factors to remain competitive in the evolving global landscape.

Matt Szuhaj (maszuhaj@deloitte.com) is a managing director at Deloitte Consulting LLP in the Real Estate & Location Strategy practice.

Tara Nicholson (tnicholson@deloitte.com) is a senior manager at Deloitte Consulting LLP in the Real Estate & Location Strategy practice.

Malvika Pradhan (mapradhan@deloitte.com) is a senior consultant at Deloitte Consulting LLP in the Real Estate & Location Strategy practice.

3. https://www.who.int/health-topics/air-pollution#tab=tab_1

4. https://epi.yale.edu/epi-results/2020/component/h2o

As used in this document, “Deloitte” means Deloitte Consulting LLP, a subsidiary of Deloitte LLP. Please see www.deloitte.com/us/about for a detailed description of our legal structure. Certain services may not be available to attest clients under the rules and regulations of public accounting. Copyright © 2022 Deloitte Development LLC. All rights reserved.

20 / CHIEFEXECUTIVE.NET / SPRING 2022 TOOLBOX

LEADING THROUGH INFLATION

PLAYBOOK

BY RAM CHARAN

ALMOST 50 YEARS AGO, as a young professor, I was hired by General Electric to design and teach a unique course to their managers at its fabled Crotonville training center. The subject was one of the most painful, difficult challenges that any business leader can face: operating a profitable, growing concern in a time of strong inflation.

For GE, it was an urgent mission. In the rampant inflation of the early 1970s, the firm’s highly coveted AAA credit rating was in peril as the company bled cash. They were hardly alone. Inflation was crippling nearly every company in the world, while also stalling the ability of the middle class to get ahead economically, let alone stand their ground. It was still nearly a decade before Fed Chair Paul Volcker’s crushing regime of interest-rate hikes would break the inflationary fever in the early 1980s.

Now, inflation is back. Every day, we hear of companies raising prices—from Starbucks and Coca-Cola to Procter & Gamble and Nestle. It isn’t just big consumer brands. A recent survey found that 61 percent of small businesses in the U.S. had raised prices for their goods and services in January—the highest percentage since 1974.

Thanks to a unique confluence of events—including an extended period of near-zero interest rates flooding the world with cheap money, Covid-driven government spending boosting consumer demand, and supply chains strained and broken by disruptions in production, transportation and talent shortages—the U.S., and much of the rest of the

CEO MAGAZINE / SPRING 2022 / 21

A

for every CEO and C-Suite leader looking to help their company prosper—or even survive—in the difficult, uncertain days to come.

CEO VOICES

SHERRILL MANUFACTURING CEO Greg Owens is trying to figure out how to price steel tableware being produced at his company’s factory in New York. But his mind is off the coast of California, bobbing on a container in the Pacific Ocean along with rivals’ forks and spoons from China.

“It will be a turbulent first and second quarter as those ships land, and there will be big price discounting in our market,” he says. The company’s premium Liberty Tabletop brand “can’t be three to four times the price of everyone else’s. Consumers’ willingness to buy things on a whim and not care what it costs has sort of gone away.”

Much like the pandemic right before it, inflation has jumped to the forefront of the minds of CEOs such as Owens. Cost increases have become a raging monster, fed by everything from Covid shutdowns to supply-chain dislocations to a mad chase for scarce labor to the war in Ukraine.

Here’s how 10 company leaders are dealing with the quandaries being created by the new era of inflation:

globe, finds itself in an economic situation not seen in a generation or more. Will central banks be able to get a handle on inflation before it gets out of control? Will supply chains unsnarl? Will people costs flatten?

It is too soon to tell, but my gut says no—at least not for a few years. That is why there is no more urgent need for business leaders right now than to get ahead of the inflation bogeyman. Corporate leaders of the past few decades have been spared the tremendous difficulties that come with trying to drive a business in an inflationary period. Few executives likely have any memory of how to do it at all. Now they will be on the front line. It’s one thing to talk about inflation at the macro level and another to keep your business healthy as the world as you know it comes unglued. The key challenge is to grasp the reality, change your organization’s psychology, and act and react quickly to the direct hits to you, your customers, ecosystem partners and the entire value chain. The dire effects of inflation happen quickly, and a recession—which could soon result from Fed action to rein in an overheating economy— compounds its effects.

Inflation consumes cash, eats margins and lulls managers into a false sense of security as inflated revenues rise. A company’s situation can erode very quickly, leading to takeover or bankruptcy. Those who are fast to react and flexible in their approach can not only survive but prosper in this challenging environment as they seize opportunities afforded by less nimble and smart competitors. Those who react slowly or choose the wrong strategy and tactics will be weakened and may even go bankrupt. The ultimate goal is to emerge from a period of inflation and recession stronger.

REAL-ESTATE INVESTMENT FIRM FIND A MIDDLE GROUND

Stephen

Bittel,

CEO Terranova, Miami Beach, Florida

Rental housing prices are skyrocketing. My development colleagues are building multifamily residences as fast as they can, but rents still have risen by 30 percent in our market. That’s gigantic. No one is getting 30 percent pay raises.

The most worrisome feature is construction costs. Material is up and labor is up, spread evenly across the job. Every subcontractor wants more money. All of the publicly available

Preparing a company to battle this sudden rise of inflation is one of the most difficult tasks that will ever confront the CEO and management. Not only must the company be prepared structurally and financially, it must also change its dominant psychology. How management thinks about inflation and the company’s responses to it will determine whether the company thrives and how it gets ahead of the competition.

Chief Executive asked me to revisit my work from 45 years ago and redesign it for the current moment, when customers rule, the world is digitally interconnected and information is viral.

Whether you are a CEO, a member of the board of directors or the CFO or CHRO, this article is about what everyone must do to manage in an era of global inflation and slowing economic growth. It lays out a brief framework for how the entire company must shift its psychology, strategies, tactics and resources to minimize the effects of this corrosive economic environment, while watching for the opportunities that will arise as competitors fail to meet the challenge.

Keep in mind that inflation can retreat as quickly as it pounces. Any aggressive action the Fed takes to tame it is likely to cause another sudden shift, this time to a radical slowdown in the economy. The mechanisms and agility you develop to adapt to high inflation will be equally useful to adjust to the next big shift. With either scenario, make no mistake: The time to act is now.

22 / CHIEFEXECUTIVE.NET / SPRING 2022

The Inflation-Era CEO

A successful chief executive’s dominant psychology in good times is aggressive, optimistic and oriented toward one goal: profits, EPS or EBITDA. In my experience, many CEOs do not pay deep attention to the balance sheet—working capital, cash, borrowing, financing and refinancing and Capex. No one will face greater challenges in managing successfully in an inflationary environment than CEOs. They must not only oversee a major shift in the way the company does business but also a major shift in the psychology and focus of every manager.

The priority must now become growth of real volume, real revenue, not inflationary revenue. A balance sheet in this environment may require—because of cash flow needs—giving up cash-inefficient customers or market share. That means focusing on certain segments of your market that are more profitable and letting others go. Even the more profitable segments will generate less cash than before, so you need to think about how this will impact capital allocation. This can be difficult for some CEOs to deal with psychologically. So, a reminder: The goal is not market share gains for the sake of market share gains, but cash-efficient market share gains that are durable.

To start, the CEO should consider taking the top team for an off-site to discuss and learn the lessons of what inflation has done throughout history, especially in the 1970s in America and Brazil. The goal is to help everyone transition their thinking to a world where the cost of capital and the cost of doing business are both going up at the same time. As a result, you will have two choices: to absorb the impacts or rethink your business model. Pricing, receivables, inventories, narrowing the product scope if necessary, selecting your customers far more carefully—all of these possibilities are now on the table.

Be prepared: You may need to deliberately shrink or exit cash-inefficient businesses and become smaller and more focused. The way the company measures performance, like market share gain and pure revenue

THE 5 PRIORITIES FOR THE COMPANY

Keep your eye on some essential priorities. The most important thing is continued cash flow generation, forecast on a very conservative basis. With that, make your cash outflow forecast on most likely risks. Out of the net cash flow, the company should prioritize efforts in the following way:

1. CONTINUITY OF THE BUSINESS . What is required for the longevity of the business and winning against competition? It could mean advertising money, short-term innovation to justify higher product pricing, certain kinds of marketing expenditures or certain kinds of expenditures for reducing costs and breakeven points. Whatever capital expenditures or operating expenditures—Capex or Opex—are necessary to preserve the future, while not destroying the present. That’s the number one priority.

2. DIGITALIZATION OF THE BUSINESS. This is existential. If you don’t digitize, you die. You must never lose focus here, no matter what happens. Your ability to react quickly depends critically on real-time data and analytics. Pre-Covid, people were slow to do this. During Covid, those who had done the work prospered, and those who did not were hurt. In an inflationary period, connecting your enterprise digitally so you have real data on your customers and their spending is mandatory. You must increase your speed of reaction to change.

3. FIXING BOTTLENECKS. Eliminate friction and bottlenecks everywhere, especially in the supply chain. The drag on the business from slow cycle times and inventory in the pipeline will become more expensive as inflation grows.

4. INNOVATION—BUT MORE FOCUSED INNOVATION. Overall, you must not lose the innovation mindset in the company. Understand what the consumer is willing to pay more for and focus your efforts there. It’s okay to be incremental unless something big comes in your sector that you can’t ignore. The greatest innovation mistake companies made in the 1970s was not to increase the price but rather shortchange the product (remember the shrinking candy bars?). That strategy backfired and hurt many brands for decades. Your products and services must remain fresh and new and show that they are of high value to justify a high price.

5. CAPEX FOR BUILDING CAPACITY IF YOU NEED IT, AND NOT IGNORING MAINTENANCE. Many people postpone maintenance. Don’t. It will come back to haunt you at the wrong time. Think about how inflation will change not just your company—but your industry—and work backward from there.

CEO MAGAZINE / SPRING 2022 / 23

discussion about inflation has caused them to raise prices.

But we went back to them and said, “Please explain these increases to us.” The result is that they took lower margins, are working harder on labor and trying to buy materials better. They said fixed prices would bankrupt them, so we worked out a middle ground. We don’t want them to be bankrupt, and we want to get our jobs done quickly.

TIRE RENT-TO-OWN CHAIN TIGHTEN UP OVERTIME

Larry Sutton, CEO RNR Tire Express, Tampa

Tire manufacturers couldn’t possibly have projected what was going to happen, so that created a supply shortage. We’ve had four price increases over the last year from all of our vendors, and we have been told to expect three or four more.

But it is what it is, and we’ve got to run our business regardless of what happens or why it happens. We’ve taken part of the pricing hit ourselves because we have a loyal customer base. More than 40 percent of our business comes from previous customers, and it’s climbing every year, approaching 50 percent soon.

They got us where we are, so we’re not going to take the entire cost increase and pass it on. We suck up half of it.

We also put our guys on a different overtime program so we could be more careful and not let people work 50 hours, and not have people turning in 50 hours when they only did 40. Our guys will work seven days a week if you let them, and we were pretty loosey-goosey with that.

growth, may have to be reprioritized and changed. You will have to know the real volume versus the revenue because increases in price disguise and distort that volume. To protect real profitability, you’ll need to revisit key contracts—and change those that lock you into a situation that could lead to a cash shortage. You will need to do all of this and create two or three scenarios right now for 2023. Revisiting long-term contracts for inflation is a very difficult task. It requires courage, logic and excellent relationships with customers. But it must be done.

For public companies, there will be a contraction of multiples in the stock market as inflation comes along. Investors will discount for lower growth and segregate those that have high debt, those that cannot manage their working capital and those that did capital allocation in the context of zero percent interest rates, as interest rates potentially rise beyond 7 percent or 8 percent.

Your market cap will be based increasingly on your real volume, real margins and your real cash flow. If you can top your competition on that basis, you will attract more capital and more investors. So, it is essential that you focus on the market cap and work backwards. What is the right level of debt, of margins, of receivables, of costs—and real prices?

For private companies, which lack the opportunity to be scrutinized by outside analysts and investors, it is even more important to dive into these details.

Not having a working capital/cash goal is perilous now, because the most insidious part of inflation is what it does to working capital, trapping cash in receivables and inventories. Almost all customers will do their very best to extend their terms of payment—from 60 days to 90 days to even 180 days or more—and in an inflationary period, this cash trap is costly. Working capital— and these customer relationships—must be managed closely.

The CFO and CEO need to think through how they will handle this. They should discuss whatever else could be coming in the next eight quarters and how they’ll adapt, including how the company will handle cash generation and capital allocation under various inflationary scenarios—and not just for the first year, but sequentially, cumulatively, for three years.

The CFO can do stress-testing for a variety of scenarios for liquidity purposes. For most companies, this exercise will not be easy, because for most companies, there are too many demands on cash. The board and CEO should create a framework for priorities to determine how cash should be allocated.

Ask your CFO sharp questions, such as: If the inflation rate goes from X to Y, what would that do to our cash position and competitive position? If inflation continues, what are the risks to liquidity, if any?

You may also want to commission an outside study of how inflation will impact the company’s end-to-end value chain. No two companies will be impacted exactly the same way by inflation, but since so many companies are linked to one another, it’s critical to understand how it will impact everyone in your ecosystem.

As part of this, it is essential to understand how pricing increases

24 / CHIEFEXECUTIVE.NET / SPRING 2022

and accounts receivables will affect many companies as a backdrop to your company’s own operations. This extends beyond the changes themselves to the architecture of the changes—who is leading, who is lagging—not just in your sector but in the context of many sectors and subsectors.

Cash management is the keystone of managing in inflationary times, and you need to have a clear picture of where the cash is coming from and where it is going. Board members and executive leadership should have input into ways to reduce costs and lower their cash break-even point and their cash consumption. They should share any information they have about B2B customers whose financial position could adversely affect the company’s business.

Pricing policy is second only to cash management as a priority. An understanding of the pricing mechanisms in place and the availability of a dashboard that gives any member of the executive team or board an instant update at any time makes the task easier and allows everyone to keep a closer watch on financial developments. This is especially true for cash-strapped companies in low-margin businesses, particularly those that have high debt with restrictive covenants.

No matter what, you must continue to build the future even as you focus intensely on the day-to-day immediacies. A disciplined approach to people development and innovation will position the business to leap ahead once inflation subsides—which, in my view, could be five years. How would you become a better company with a better ranking in your industry? That’s an essential question to always keep in mind.

Communication Is Key

The CEO’s first and most important task is to communicate, communicate, communicate. Once is never enough. Repeat the seriousness of the challenge confronting the organization and the urgency with which that challenge must be met with total candor, honesty and credibility, both internally and externally. The CEO is both an educator, ensuring the senior team understands the challenge and consequences of failure, and a social engineer, overseeing the coordination of the various functions so information flows freely and quickly from every silo, acting as a lever for the culture. Management must counter confusion and anxiety created by the media, particularly social media. This is of great importance.

When communicating, there are three essential principles to follow: Did the recipient receive the message the way it was intended? (Measure that.) Did you get the recipient’s reaction to your message? (Be sure.) What new behavior of the recipient did you discover? (Find out.) True communication is not a one-way PowerPoint presentation in which the recipient absorbs less than 20 percent of the message.

The CEO can start by rallying the team. Say, “We’re going to win in this new environment,” and communicate how you’re going to win. Yes, you’re going to take some costs out. Yes, you’re going to change some KPIs. And you’re going to have to have information

R&D: A NEW ROLE FOR INNOVATION

R&D, USUALLY FOCUSED ON the lon g term, tends to have a dominant psychology that sees itself apart from the day-to-day problems that besiege the company in an inflationary environment. R&D wants stable employment to prevent the disruption of ongoing projects, and it doesn’t want to be the pawn of finance. But the new circumstances leave no room for complacency anywhere within the company.

Most R&D resources fall into one of three categories: long-term, “blue sky” projects that may yield important breakthroughs, projects aimed at making incremental changes in products or processes, and projects aimed at using new technologies to change product attributes or processes. A fresh look at the allocation of total R&D resources going forward three to five years is the first step in adjusting to the new environment.

The first priority of R&D in this economy is to focus innovation efforts—above all else—on the continuity of the business, on the products and services that will justify the higher prices that you will demand in the market.

In consultation with the CEO and CFO, R&D leaders must decide which resources and projects are to be preserved and which jettisoned. Remaining projects should be rank-ordered in terms of importance to the company in the post-inflation, post-recession world. And a determination should be made about partnering with other companies on some projects in order to free up research talent to concentrate on critical projects.

Work with marketing to determine which projects can be slowed and which need to be sped up to take advantage of market opportunities and competitive changes. Be alert to opportunities to bring in new talent that will enable the company to profitably diversify product offerings or find more efficiencies in operations.

CEO MAGAZINE / SPRING 2022 / 25

REAL ESTATE DEVELOPER TARGET MIDDLE AMERICA

Mitch Provosty, CFO, RREAF Holdings Dallas

Most of our five verticals—including multifamily dwellings, older beachfront hotels, extended-stay hotels and entire town centers—get to reprice their rents annually, and hotels can do it daily; we have no buildings with 20-year leases. So, we’re not at risk of having our costs go up and not being able to adjust our rents. We adjust our rents to market, and they perform well for us.

There has been some concern that increasing rates and rents will outpace what our tenants can afford. But we’re not at the top of the food chain—we’re not the most expensive properties out there.

That’s especially true for our beachfront hotels: They cater to middle America. They’re on everyone’s beach: Pensacola, Cocoa Beach and Panama City [Florida]. Our customers there are getting squeezed by inflation, but in the end, they’re going to get salary increases.

TABLEWARE MANUFACTURER KEEP COMPETITIVE

Greg Owens, CEO, Sherrill Manufacturing, Sherrill, NY

We’ve put through an average price increase of 25 percent; some products going up by 60 percent, others by 8 percent. Five years ago, we tried to stay 5 percent to 10 percent above the most expensive Chinese-made tableware and 50 percent above the lowest. But even after they recently increased prices by 25 percent, our prices now are double and triple the opening price point for tableware on Amazon.

Consumers aren’t dumb. We have

come to you unfiltered from the ground so that you know what is happening with customers and with your cash position. Make sure this message is clear—no filtering, no hiding bad news. Assure employees that you are not just being defensive and making shoot-from-the-hip decisions on narrowing the focus and cutting costs. You must continue to communicate about innovations, new products and new ideas, too.

Working in conjunction with the CFO and CHRO, the company’s internal communications people should create a website or dashboard accessible to all employees and updated at least fortnightly that presents an analytical picture of the company, its competitive position and the steps it is taking to execute its strategy. It should also include macroeconomic news, such as Federal Reserve policy statements and actions and relevant international news, including price increases in various companies and industries, to educate employees and partners, giving them the context of your company’s moves. It may be appropriate to establish a hotline to respond to employee concerns and queries.

Externally, people in charge of internal and external communications need to adopt an attitude of more transparency to reduce anxiety within the company and build a relationship of trust with media outlets.

Communications staff should be proactive in establishing links to both national and local media, demonstrating that the company is methodical, solid and has a realistic view of the environment in which it is operating. The media is confused about the economy, so the communications people should work with reporters and editors to demystify the company’s situation and how the company sees the current economy and be able to clearly show how the company is working through these challenges.

At public companies, the firm’s IR people must learn in detail from the CFO and others how the company’s performance indicators will be affected by inflation and an economic slowdown and must convey that information accurately and fully to investors. Any misstep that hints at cover up or distortion will be disastrous in the investment community.

Unfortunately, most IR people’s understanding of what is going on in their industries and more globally is very inadequate right now. That does not allow them to communicate clearly what—or why—the company is doing what it is doing in the context of the larger world.

The IR person must be able to do this, to communicate clearly and unambiguously to the investment community about how the company is positioning itself. They need to build a record of outcomes from the company’s actions, showing, for example, where price increases stuck and where they didn’t, and be able to explain the company’s next moves as a result of that.

IR should be attuned to the investment community and able to seek out big investors who understand the company’s situation and its prospects in the post-inflation world and are willing, as a consequence, to invest in the company.

The trust part of investor relations is very important now. Be

26 / CHIEFEXECUTIVE.NET / SPRING 2022

sure your IR people are spending 80 percent of their time with the buy side. Buy-side people need to know that an inflationary period is here and what you’re going to do. Your IR person has to be savvy to extract information from investors about what is really happening in the industry. The subsectors investors are moving toward will tell you how inflation is playing out across the industry and economy.

It is imperative to have your IR person— and perhaps you, as CEO, as well—reach out to critical investors to understand their assumptions about the economy and the industry they operate in. Ask them for their views. Then educate them on yours. Say: “I’d like to give you our worldview of the industry under inflation.” Getting at the reality of what the buy-side people are thinking will be the most important thing an IR person can do to help the company.

Sales and Marketing

Pricing must not be controlled by the sales force. The dominant psychology of the sales and marketing departments in good times is to capture as many customers as possible and make every sale that is possible, often without thinking too hard about whether the sale is profitable or the customer is sound. They have a psychological aversion to raising prices, the result of frequent customer pushback and demands for discounts.

To help manage the situation, two innovations are needed in the structure of your company:

1. A pricing unit, which is forward-looking, gathering data and building models. This should be a cross-functional unit that reports directly to the CFO and marketing leaders.