WASHINGTON CPA

2023 Legislative Session Preview Common Questions About Environmental, Social, and Governance (ESG)

66, Number 3 WINTER 2023

THE Volume

Delivering Results - One Practice At a time 888-783-7822 X1 www.APS.net Sherif Boctor Sherif@APS.net Tax Season Cessation Program Ready To Sell Your Practice? WE CAN HELP YOU! Scan Here Experiencing: • Stress? • Lack of Sleep? • IRS induced Nausea?

WINTER 2023

www.wscpa.org • memberservices@wscpa.org

Tel 425.644.4800

170 120th Ave NE Ste E101 Bellevue, WA 98005

BOARD OF DIRECTORS

Sara Bailey Chair

Andrew Brajcich Vice Chair

Joyce Lee Treasurer

Writu Kakshapati Secretary

Thomas Sulewski Immediate Past Chair

Kimberly D. Scott President & CEO

Sarah Funk Ed Ramos

Norman Haugen Bryce Rassilyer

Courtney Hirata Jillian Robison

Jamie Hueners Bonnie Tse

Lowel Krueger Joel Williams

CHAPTER BOARD CHAIRS

TBD Bellingham Area

Charles Meyerson Everett Area

TBD Olympia Area

Brittany Malidore Seattle/Bellevue Area

Anna Smith Spokane Area

Jessica Packer Tacoma Area

Anthony Adams Tri-Cities Area

Connie Olson Tri-Cities Area

Canada Segura Yakima Area

Wade Helms Yakima Area

MAGAZINE PRODUCTION

Jeanette Kebede Editor

Jennifer Johnson Art Direction

The Washington CPA is published by the Washington Society of Certified Public Accountants for its members. Views and opinions appearing in this publication are not necessarily endorsed by the Washington Society of CPAs.

The products and services advertised in The Washington CPA have not been reviewed or endorsed by the Washington Society of Certified Public Accountants, its board of directors, or staff.

The Washington CPA is published quarterly by the Washington Society of Certified Public Accountants, 170 120th Ave NE Ste E101, Bellevue, WA 98005. $12 of members’ annual dues goes toward a subscription to The Washington CPA

Periodicals postage paid at Bellevue, Washington and additional mailing offices.

Cover Graphics

illustration: © iStock/VictoriaBar

photo: © iStock/jeffbergen

POSTMASTER:

Send address changes to The Washington CPA, c/o WSCPA, 170 120th Ave NE Ste E101, Bellevue, WA 98005.

Barrier Busting: Uncovering Benefits for the Profession

2023 Legislative Session Preview

Common Questions About Environmental, Social, and Governance (ESG)

What Young Professionals Want From Your Firm

THE WASHINGTON CPA

Staying Ahead of the Inclusion Curve Conflicts of Interest Still Cause Trouble for CPAs Exploring Excel's Hidden Treasures: LET and LAMBDA Functions On the Cover Membership News Leadership Lens Washington CPA Foundation Upcoming CPE WSCPA Peak Firms Classified Ads Spotlights Departments 4 6 15 32 37 38 12 26 28 8 10 16 20 @WashingtonCPAs CONTENTS 3 www.wscpa.org The Washington CPA Winter 2023

•

The CPAs Care Tour 2023 is launching in January with charity volunteer events scheduled around the state. Join fellow CPAs in your area for hands-on volunteer opportunities that will make a difference in your community. Check out these events and stay tuned for upcoming dates and locations.

• January 21

• January 31

•

Visit and discover a library of free, downloadable content right at your fingertips. Includes white papers, webinars, product guides, case studies, industry analysis and much more, provided by experts and vendors within the accounting industry. Check it out at hub.wscpa.org.

Need to get away?

WSCPA Passport Card can help. Your WSCPA membership includes this free benefit (a $150 value). Access 3,000+ discounts online and in your neighborhood. Great for dining, travel and shopping. Find your next adventure at wscpa.org/passport

|

|

Woodinville

Homeward Pet

|

|

Vancouver

Clark County Food Bank

|

February 4 | Spokane

Habitat for Humanity

|

February 10 | Bellingham

Lydia Place

JUNE 13-14 SAVE THE DATE Plan to attend the WSCPA ANNUAL MEETING AND MEMBER EVENT More details coming soon!

Knowledge Hub - A Free Member Resource!

Registration is required as space is limited. Find your event and register at wscpa.org/events.

WSCPA

4 The Washington CPA Winter 2023 www.wscpa.org MEMBERSHIP NEWS

WBOA Announces CPE Summary Upload Feature Is Live

Submitting Your Required CPE for License Renewal Just Got Easier

The Washington State Board of Accountancy (WBOA) announced that a CPE summary upload feature has gone live on the WBOA service dashboard via SecureAccess Washington (SAW). Any licensee can now upload CPE from a pre-formatted CSV file into the state’s CPE Tracker, which is mandatory for license renewal.

The WSCPA is currently modifying our online CPE transcript program so that any CPE you have taken through the WSCPA (and/or external courses you have added via the WSCPA LCVista CPE Suite) can be exported in the proper format and then uploaded directly to the WBOA’s system.

The WBOA released the CPE Tracker in 2021. An upload tool, like the one released, was a part of the initial plan for the tracker when it was proposed. Unfortunately, due to time and technology constraints it was dropped from the initial release version.

“The WSCPA diligently shared our members’ struggles with the WBOA CPE Tracker at meetings with the WBOA and key staff. We are thankful that the State Board continued to work through the many technical challenges in order to make this tool a reality,” said Kimberly Scott, President and CEO of the WSCPA.

“This feature has been front of mind when we receive calls from members who are going through the renewal process and we are excited the feature will be made available immediately for all licensees to use when verifying their CPE.”

For those individuals who track their own CPE in Excel from a number of sources, the CSV format file is available via the QR code below, or through the WBOA CPE Tracker interface and can be used normally through Excel. The WBOA’s instructions for use of the CSV template, plus tips and tricks, can be found below as well.

Download CSV File

Instructions, Tips & Tricks

CPE 5 www.wscpa.org The Washington CPA Winter 2023 MEMBERSHIP NEWS

illustration: © iStock/Oleksandr Hruts, © iStock/ST.art

Investing in the Future of Our Profession

Sara Bailey, CPA

I hope you all had a wonderful holiday season and have had some time to unplug and rejuvenate while also reflecting on the many things for which you are thankful. As I reflect on 2022, I am grateful for my family and our health as well as for being part of such a wonderful community of CPAs. I’m excited to share some of the work we’ve been doing at the Society during the last few months.

In the summer issue of The Washington CPA, I wrote about some of the challenges our profession is facing and how the WSCPA is tackling these along with our membership group. During our annual board retreat last June, we revisited the Society’s strategic plan. We challenged each other on the role the Society should play in various challenges facing our profession and offered some bold ideas.

In order for our board and the WSCPA staff to hear diverse perspectives as a part of this strategic planning process, we held two additional think tanks—one with a group of prior WSCPA board members and a second with individuals from our Diversity, Equity & Inclusion Council and accounting students.

From these planning sessions we identified themes and significant ideas that came out of these sessions. The five main themes that emerged from the prior sessions where we believe the WSCPA can make a big impact were:

Pipeline and STEM;

Fifth-year support;

Expanding CPA resources;

Mentorship—especially focused on women and underrepresented groups, and

A CPA mega event.

STEM Mentorship CPA Resources Fifth-Year Support Phenomenal CPE CPA Pipeline Networking Big Ideas

•

6 The Washington CPA Winter 2023 www.wscpa.org

•

•

•

•

Pipeline and STEM

Making sure that students are studying accounting and are becoming CPAs (often referred to as “pipeline”) is a significant issue for our profession. There are multiple reasons for this, including a shift in the number of students seeking out higher education as well as continued competition from other professions. There is a need to market the profession to high school students and community colleges to reach students who are taking a non-traditional university path.

Do you know accounting is not a part of STEM? I was surprised several years ago when I learned accounting was not included in the areas encompassed by STEM (science, technology, engineering and mathematics). The AICPA has been working to institute this change at the federal level, but it will take an act of Congress (literally) for that to happen. Until then, the WSCPA is looking for ways to make changes in the state that will move these efforts along. Being included in STEM would provide additional federal dollars into the teaching curriculums and more exposure to kids about our profession. Pipeline and STEM is a critical area for our profession to focus on over the next decade.

Fifth-year support

We are all aware of the requirement for individuals to complete a fifth year of schooling to become CPA eligible. While we may have different opinions on the requirement itself, I think it’s universally agreed that providing additional support to students while they complete their fifth year is important. Many students in Washington complete their undergraduate degree in accounting and enter the workforce right away without being CPA eligible. If we can help bridge the gap between the undergraduate degree award and becoming CPA eligible, that makes a significant impact, not only to students, but also to employers who want to have CPAs on staff but find themselves with shrinking hiring pools of CPA-eligible candidates. The area of focus here is identifying creative ways for credits to be earned and maximizing on-the-job experience and training to translate to college credits earned.

Expanding CPA resources

Expanding CPA resources is all about continuing to create networks in our CPA community across the state to provide additional resources to CPAs that will encompass the entire working career of a CPA—from a student to a new professional, shifting to a new role or position, getting connected to potential employers, partnering with other CPAs, transitioning a business, etc. Providing additional resources to CPAs across the state is a critical component to make sure we continue to have a sustainable profession where CPAs feel supported and included as a part of a broader community.

Mentorship programs—especially those focused on women and underrepresented groups

Most people can name a mentor who was instrumental to them at some point in their life and career—a person who made a real difference. While many of these relationships tend to develop organically, sometimes that key mentorship gets missed if the things to build organically are missing or if there are competing priorities, such as being mentored by your boss where you may not be as comfortable bringing up certain issues. We also know it can be more challenging for natural mentor-mentee relationships to be built with someone who doesn’t look like you or understand your life experience—it is human nature to gravitate to someone who you can easily relate to. Mentorship for women and underrepresented groups is critical. Statistics show that as a profession, we lose more people from these groups as they move up the career ladder. That is not sustainable for our profession. By implementing a meaningful mentorship program, we can make a difference in the careers of women and those in underrepresented groups and help keep them in the profession over the long run.

Mega event

Finally, a free mega-event put on by the WSCPA. We are all familiar with how great the WSCPA does at putting on CPE events and the level of quality the programming is. Every year, the Society holds an annual meeting which is well attended; however, we really want to create THE event to attend for Washington CPAs across the state—a hub where everyone can flock to network and build relationships, take phenomenal CPE and create lasting memories.

We are so excited about these key areas and are working hard to develop actionable plans for implementation. We know these big ideas will require an investment, but we also know this investment is truly an investment in the future of our profession. We are blessed to have proceeds from the sale of our building and the flexibility that enables us to make real, impactful changes for our future.

Sara Bailey, CPA, is a partner at Moss Adams LLP and WSCPA Chair. You can contact Sara at sara.bailey@mossadams.com.

illustration: © iStock/rudall30

7 www.wscpa.org LEADERSHIP LENS The Washington CPA Winter 2023

Barrier Busting: Uncovering Benefits for the Profession

Kimberly Scott, CAE

Kimberly Scott, CAE

The challenges of the last few years have changed us individually and how we work. These changes will ripple into the future. The thought of addressing some of these changes may make you feel overwhelmed. Some changes may seem too monumental and paralyze your ability to decide where to start. Fortunately, some of these we can tackle together.

The WSCPA Board of Directors took on the challenge last year to review and update our strategic plan, focusing on goals to address the challenges we not only see now, but also those we envision will be facing us in the future. We included a wide range of participants in the process in order to gather diverse insights. Past Board members, Foundation Trustees, our Diversity, Equity and Inclusion Council and student members provided valuable input and feedback. (You can read more about the strategic planning process and the several areas of focus that were identified in Sara Bailey’s column on page 6.)

The key area of dedicated focus of the strategic plan, which is still being finalized, will not be a surprise to most of you. Many members have shared how challenging it is to find staff

8 The Washington CPA Winter 2023 www.wscpa.org FUTURE OF THE PROFESSION

to hire and how firms have been flexible in designing working arrangements to bring in or retain talent. This issue is likely to become escalated if it is not addressed. The enrollment in accounting programs at community colleges and universities has decreased. The percentage of accounting students deciding to sit for the CPA exam has also dropped. The “CPA pipeline” that brings new CPAs into the profession is absolutely a concern.

Focusing on barriers to the profession and barriers for staying in the profession appeared prominently in our strategic planning group discussions. This insight from our focus groups reminded me of a story about how removing barriers often results in a ripple effect of benefits.

Curb Cuts: A Barrier Busted

The story is about curb cuts, the dips in the sidewalk that connect to the street. Do you know how these began? They were implemented following World War II. Disabled veterans were returning home and finding difficulty maneuvering their sidewalks and streets. The idea of adding curb cuts was not met with overwhelming approval, as it was a very costly and time-intensive project that many saw as serving “just a few” people. However, as curb cuts are now standard, we know this investment was approved. Think about how many other problems these curb cuts solved that were not even considered at the time the solution was proposed. Removing one barrier now also provides benefits to strollers, shopping carts, bicycles, as well as a general ease in crossing the street. Removing the barrier did not make the sidewalk less valuable.

The Barrier: 150-hour Requirement

Turning back to the CPA profession, are there some barriers to becoming a CPA that could be removed, while still allowing for those entering the profession to be well equipped, and leave the profession unharmed? One example is the requirement to sit for the CPA exam at 120 hours. A student would still need 150 hours of education to obtain their license, but they could start the testing process while in school, shortly after learning their area of expertise, and when they are already used to studying and taking exams. Contrast this with the current reality many candidates face: trying to juggle taking the exam and full-time work. Statistics show that states where the 120-hour option already exists saw about a 25 percent increase in students starting the exam. The WSCPA has been working with the Washington State Board of Accountancy during the last year to make this change and we hope to see the rule officially change in early 2023.

The Barrier: The Stories We Tell

We are also working to identify barriers within the profession and our organizations to help us attract and retain CPAs. While this challenge is far more complex, there have been some great ideas from some thought leaders in the profession to get us started. Here is a simple example. We all know the value of the CPA, the doors it can open, the opportunities it can bring. However, we often tell or hear the stories about how horrible the working hours are, or how difficult it is to move up into leadership roles. Selling something when only highlighting—and maybe even exaggerating—the negative parts of it is an arduous task.

The Barrier: Awareness as a Leader

I challenge us to personally become more aware of the barriers we have as well. I believe as a leader we should be welcoming feedback, be willing to be respectfully contradicted, admit when we are wrong, and acknowledge openly when others are right. If we are not learning and being challenged, we probably have created barriers within our own work cultures.

Thank you for being a part of the Washington Society of CPAs as we welcome a new year and bust barriers for the good of the profession and both current CPAs and future ones!

Kimberly Scott, CAE, is President & CEO of the WSCPA. You can contact Kimberly at kscott@wscpa.org.

9 www.wscpa.org The Washington CPA Winter 2023 FUTURE OF THE PROFESSION

illustrations: © iStock/MicrovOne, © iStock/Svetlana Ikriannikova

2023 Legislative Session Preview

Mike Nelson

Mike Nelson

With the 2022 elections behind us, we adjust our focus to the 2023 Legislative Session. Democrats in Washington have expanded their legislative majorities in both the State House of Representatives and Senate. The party now holds a 58-40 lead over Republicans in the House and a 29-20 lead in the Senate.

In December the Senate and House finalized changes to committee structure, various committee rosters, and how the public will be able to interact with the process. Since the last two years have been virtual sessions this will be the first year that many of the legislators have been in person with each other and the public in any capacity.

10 The Washington CPA Winter 2023 www.wscpa.org ADVOCACY

photo:© iStock/zrfphoto

As we prepare for the launch of the session, WSCPA members will meet with legislators in Olympia during Hill Day on January 19 to discuss key matters expected to come before the legislature.

There are several issues that we are expecting to be addressed by the legislature when the session begins in January. This year is a “long” session which lasts for 105 days. The legislature will be enacting a new biennial budget for July 1, 2023 until June 30, 2025. Despite continued slowdowns in economic growth and worries about a potential recession, the state is still expecting tax revenues to grow slightly.

Margin Tax & More

As part of the expected budget a significant issue that the WSCPA Advocacy team has been tracking is recommendations from the Tax Structure Work Group (TSWG) or additional new tax proposals. The TSWG has been discussing how to make the tax system more progressive and fair. We expect to see several of the recently-discussed proposals related to budget to be introduced during the session.

As reported in the fall 2022 issue of The Washington CPA, one of those proposals is a margin tax styled after the Texas tax system. The TSWG voted 6-1 at their December meeting to include a margin tax recommendation to the legislature. This proposal still has a lot of unknowns around it and more clarifications will be needed.

Wealth tax proposals have also been discussed by Senator Noel Frame and legislators have expressed broad support for increasing property tax and rental credits, as well as expanding other programs like the Working Families Tax Credit. Additional increases or new tax proposals are expected to accompany these proposals, as any new tax credit or reduction would need tax revenues to offset them. There have been some discussions around modifying certain provisions of the estate tax system to limit qualified charitable deductions. This would bring more money into the state as many large estates have been leaving significant funds to charities in recent years.

Long Term Care Act

Beyond the many aspects of the budget documents and potential tax changes, the Long Term Care Act is expected to be discussed again this session. The start of this program was delayed from January 2022 to July 2023 and more tweaks are expected. According to the committee overseeing the implantation of the program, more exemptions were granted to the payroll tax portion of the program than were expected. Because of this there are various requests for the legislature to revise the exemption provisions of the program. One of the changes would be a timed exemption so that an individual who had been granted an exemption would be required to show on an annual basis that they have maintained their private coverage. If this, or other, modifications are made to the program, some of the individuals who had been granted exemptions to the

program would likely lose their exemption, increasing the tax base funding the program.

Capital Gains Tax

Another large unknown is when and what the State Supreme Court will decide about the capital gains tax that was passed in 2021. The Douglas County Superior Court ruled the tax was unconstitutional during the summer, but the State Supreme Court is scheduled to hear oral arguments in the case in late January. On November 30, the Supreme Court stayed the lower court ruling. This means that the Department of Revenue (DOR) can continue to prepare for and collect the tax on April 18 if the court has not issued a decision in the case by then. Regardless of the final court decision, the legislature will likely need to act. If the court determines the tax is unconstitutional, the legislature will need to account for the nearly $1 billion decrease in their current and projected future biennial budgets. All, or most, of the funds collected by the tax were earmarked to go into the Education Legacy Trust Account. This account helps fund K-12 schools, higher education financial aid, early learning and child-care programs. On the other hand, if the Supreme Court rules to allow the tax to proceed, depending on the specifics of their ruling, more guidance will need to be provided by the DOR and additional clarifications of the law will need to happen. The DOR sought legislation in 2021 to clarify certain aspects of the law but that was not pursued by the legislature while they awaited the Supreme Court’s decision. This would likely need to be revisited if the tax is allowed to move forward. There have also been some discussions that if the State Supreme Court does allow the tax to move forward, then there will be a legal challenge in federal court. If that does happen, the legal uncertainty around the tax will likely continue for a few more years.

Given the many uncertainties or nuances, if you or your firm expect to have clients who would be subject to the capital gains tax, the WSCPA will continue to schedule pop-up CPE programs covering the tax as updates unfold.

Throughout the legislative session we will continue tracking these major pieces and any new issues that develop. You can watch for updates via the All Things Advocacy blog and email.

11 www.wscpa.org The Washington CPA Winter 2023 ADVOCACY

Mike Nelson is the WSCPA Manager of Government Affairs. You can contact Mike at mnelson@wscpa.org.

Staying Ahead of the Inclusion Curve

Monette Anderson, CAE

During December 2022, I was fortunate to be able to attend two special events in the Diversity, Equity, and Inclusion (DEI) space. One was the WSCPA DEI Workshop facilitated by Kevin Henry. The other was the American Society of Association Executives Conscious Inclusion Summit. Both events involved workshop-style formats where attendees were encouraged to collaborate and share ideas.

I’ll highlight an overview of a couple of exercises that resonated with me, and encourage you to find these activities/resources and reflect on them yourself:

The Trusted 10 Exercise

Make a list of the 10 individuals that you most trust. Now examine your circle of 10 most trusted individuals and their top identity characteristics. Looking at your list of names, think about each individual’s gender, religion, ethnic group, sexual orientation, marriage status, political background, and nationality. Do those on your list mirror your own identity traits and values? Often this is the case. When you think about your work life, are you gravitating to people most like you? Who are you approaching on your team when there are high visibility or stretch assignments to assign?

Workplace Privilege

Deanna Singh, author of Actions Speak Louder: A Step-By-Step Guide to Becoming an Inclusive Workplace, led a session examining privilege in the workplace. While we started with statements like “I don’t have to work extraordinarily hard to ensure my ideas are heard in meetings, elevated during discussions, and advance to the levels where decisions are made” or “I can feel included in office culture, surrounded by people I feel comfortable with and who feel comfortable with me,” our group immediately began discussing other privileges we less often consider. Privileges such as access to flexibility regarding child-care arrangements, not having a long commute to place of employment, or having the confidence and status to initiate innovation in the workplace.

Exercises like these can be a reminder why it’s important to keep leaning into DEI work; there is inherent value in connecting with others, building bridges, and creating more inclusive workplaces for all. This encompasses race, gender, disability, religion, age, military status, sexual orientation, sexual identity, and family-care status.

Firms and businesses continue to deal with the reeling effects of the pandemic, the great resignation, the great retirement, accounting enrollment declines. Furthermore, college enrollment is predicted to fall by more than 15 percent after 2025, a trend being called “Enrollment Cliff.” These sociological factors are all working together to create a dire shortage of incoming CPA and accounting professionals to manage work that is likely to only get worse. These are all forcing the profession to seek out new recruitment sources and address the corresponding access and barriers impacting our incoming pipeline.

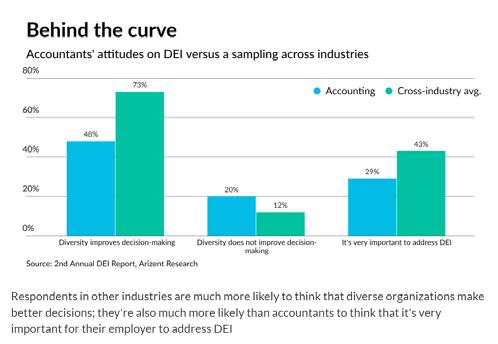

Arizent recently conducted a survey across a number of different industries, the ROI on DEI, which revealed that the accounting profession remains behind other industries in their perception of the value of DEI. A few stats reported by Accounting Today’s Daniel Hood in “Accountants and DEI: By the numbers,” an article published in October 2022, are concerning. (Refer to charts on following page.)

Additionally, accounting respondents were 25 percent less likely than their peers to feel that diversity improves decision making, and 18 percent less likely to feel it was important to address DEI.

What are the unintended consequences of the above attitudes and beliefs persisting in our profession?

• Recruitment of new candidates: According to Zety.com 2023 HR Statistics: Job Search, Hiring, Recruitment and Interviewing, 67 percent of both active and passive job seekers say that when they’re evaluating companies and job offers, it is important that the company has a diverse workforce.

• Retention of current staff: People are more than five times more likely to remain at inclusive companies according to Great Places to Work April 2021 article, “Why is Diversity & Inclusion in the Workforce Important.”

• Future investments: Inclusive organizations are 70 percent more likely to capture new markets as reported by Builtin’s October 2022 article, “54 Diversity in the Workplace Statistics to Know.”

• Lack of innovation: Dimins.com reports in their February 2022 article, “Why Diversity Matters in Decision Making,” that inclusive teams make better decisions 87 percent of the time.

12 The Washington CPA Winter 2023 www.wscpa.org DIVERSITY, EQUITY AND INCLUSION

Respondents in other industries are much more likely to think that diverse organizations make better decisions; they're also much more likely than accountants to think that it's very important for their employer to address DEI.

The accounting profession needs to increase diversity and inclusion efforts to remain competitive to their workers, customers, and reputation. It’s incumbent on all organizations to implement actionable steps, appropriate to their organization, to move us all forward. Organizations that don’t are sure to be left behind as investors, customers, and their employees demand it.

The WSCPA has been working to create a DEI Council of our members who will undertake some initiatives to continue to move the WSCPA, our members and the organizations they represent forward. We can’t wait to introduce them to you and share the important work they are undertaking in the coming months.

If you’re interested in learning more about DEI and available resources, join the WSCPA Diversity and Inclusion Resource Group in Connect, the WSCPA’s private community at connect.wscpa.org

Monette Anderson, CAE, is the Executive Director of the Washington CPA Foundation and WSCPA Director of Member Services. You can contact Monette at manderson@wscpa.org.

Charts shared with permission from Accounting Today. illustration:© iStock/bortonia

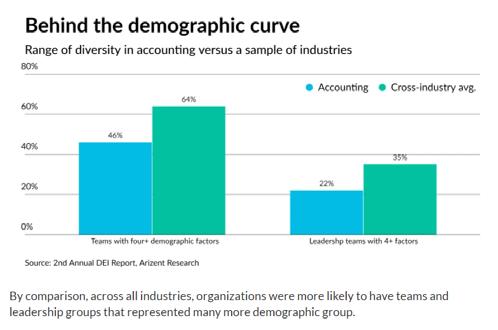

By comparison, across all industries, organizations were more likely to have teams and leadership groups that represented many more demographic groups.

13 www.wscpa.org The Washington CPA Winter 2023 DIVERSITY, EQUITY AND INCLUSION

Thank You

- TO OUR 2022 SPONSORS -

ACCOUNTING FOR A NEW AGE

Accountin g Where can take you? The Washington CPA Foundation is excited to be able to offer over $500,000 in scholarships for students in Washington State. Students entering junior year or higher in the fall of 2023. fifthyear, master's, and PhD candidates, as well as, community college transfers are encouraged to apply for this scholarship level. AWARD AMOUNT $5,000 - $10,000* * $10,000 scholarships for master’s / PhD candidates APPLICATION DEADLINE February 14 Win a $5,000 Accounting Scholarship! APPLY NOW! WSCPA.ORG/CPASEAS Help us give away over $500,000 in Accounting Scholarships! TIME COMMITMENT 15-20 hours Scholarship applications are reviewed in your home or office through our secure, online portal with a provided scoring matrix and guidelines. Contact Benjamin Warren at bwarren@wscpa.org APPLY NOW FOR A $2,000 ACCOUNTING SCHOLARSHIP! Where can accounting take you? FOUNDATION SCHOLARSHIPS BECOME A SCHOLARSHIP REVIEWER Apply by April 14 WSCPA.ORG/AA22 Are you are a 1st- or 2nd-year student (fall of 2023) who's interested in pursuing a career in accounting? 15 www.wscpa.org The Washington CPA Winter 2023

Common Questions About Environmental, Social, and Governance (ESG)

Your organization could accelerate its mission, transform its culture, strengthen brand value, and increase the bottom line by aligning business practices with environmental, social, and governance (ESG) principles.

As organizations rapidly pursue initiatives to support their values and meet the expectations of stakeholders, it’s crucial to implement, track, report, and assure standards that accurately define and measure your progress.

Implementing an ESG strategy can help achieve these initiatives, while driving further growth and brand loyalty. Other benefits could include being able to identify tax savings and cash flow opportunities, just to name a few. Here’s a breakdown:

Justin Neff, CPA and Colleen Rozillis

© iStock/Man

© iStock/OlgaKlyushina 16 The Washington CPA Winter 2023 www.wscpa.org BUSINESS STRATEGY

illustration:

As Thep,

What Is ESG?

The categories that comprise ESG—environmental, social, and governance—provide an opportunity for your organization to evaluate its impact on and position in an increasingly sustainable market.

Each category includes various aspects your organization can analyze to address the needs of various stakeholders: employees, shareholders, customers, and members.

The Framework of ESG

Your organization can determine other aspects that may hold greater importance depending on your unique brand, values, and goals. Here are examples of each category.

Environmental

Environmental factors relate to your organization’s interaction with the physical environment.

• Climate change

• Environmental policies and regulations

• Renewable energy utilization and procurement

• Raw material sourcing

• Water and waste management, recycling, reduction in waste, or reduction in single-use plastics

• Greenhouse gas emissions

• Land use

• Energy efficiency

• Responsible supply chain or contractor code of conduct

Social

Social factors relate to business practices that impact communities and society.

• Diversity, equity, and inclusion

• Employee health and safety

• Human capital development

• Privacy and data security

• Product quality and safety

• Gender, racial diversity, and LGBTQ+ representation within the workforce and leadership

• Pay equity

• Policies and procedures that support effective workplace culture

• Employee turnover and retention statistics

• Employee engagement survey results

• Community involvement and investments

Governance

Governance factors relate to the corporate structure and how an organization operates.

• Business ethics

• Corporate resiliency

• Board and leadership diversity

• Executive compensation and incentives

• Ownership structure

• Enterprise risk management

• Board oversight of policies

• Lobbying and political activity

Who in the Organization Should Be Involved with ESG?

Identify a leader to champion the creation and execution of your ESG strategy. The ESG champion should have enough authority across the organization to gather data, engage cross-functional teams, and influence strategy.

You’ll want stakeholders involved from your key internal services—finance, procurement, legal, human resources, DEI, IT, facilities, and risk management—as well as operational functions and those who support the board.

Bring in members of the management team who understand strategy, the bigger picture, and are excited to invest in a change management initiative.

How

Do You Start Creating an ESG Strategy?

Before beginning an ESG plan, conduct a readiness assessment. If you build an ESG strategy that isn’t suitably supported, there are potential risks to your organization’s reputation and strategy effectiveness.

The readiness assessment should identify your desired state and whether you have the organizational resources, skills, data, and capacity to get there; if not, what gaps exist, and what resources may you need to address those gaps?

Each organization’s capacity, culture, and skills will vary, but your ESG committee can help identify existing resources across the organization. If gaps remain, part of your ESG strategy can include initiatives to address them.

How Can Your Organization Create an ESG Plan? Approach creating an ESG plan by starting with your organization’s strategic plan: Where does ESG align with your overall vision, mission, and values?

Establish vision and purpose statements for your ESG initiative and develop both short-term and long-term goals that are relevant to your board, investors, stakeholders, staff, and leadership.

Each goal should be supported by target outcomes and initiatives that are clearly defined and measurable, have ownership assigned, and resources dedicated or budgeted where applicable.

How Can You Measure ESG Initiatives?

The most important part of your ESG strategy is deciding what and how to report your progress toward achieving outcomes. You’ll want to tell your own story and provide timely, relevant information to your stakeholders.

17 www.wscpa.org The Washington CPA Winter 2023 BUSINESS STRATEGY

For each outcome area, identify meaningful performance metrics. Performance metrics will vary for each organization based on your unique operations and the outcomes you’ve established. Assess the data you have available, identify any gaps you want to fill, and ensure that the data you report is reliable and accurate.

What Is ESG Reporting?

Consider creating a performance dashboard to report your ESG targets and metrics. A successful ESG dashboard will be a snapshot of status and trends over time, show performance against defined targets, and encourage dialogue about progress towards goals.

Providing a regular report to your board, on a quarterly or biannual basis, will help you to monitor progress and continue to refine your goals as your ESG strategy matures.

Many organizations also develop narrative ESG reports detailing their data, efforts, outcomes, targets, and other relevant information.

ESG reports can be powerful communication tools to your staff, board, investors, the public, and other stakeholders. They demonstrate transparency and awareness that your organization’s operational and business goals are in service of your values.

There are several existing frameworks and standards that can help guide your reporting efforts, but there’s no universally accepted framework at this time. Many companies also look to CPA firms to validate the reliability of their ESG disclosures through third-party assurance.

What Are You Already Doing that Could Qualify as an ESG Activity?

You may already be taking actions that could qualify as ESG activities. By improving your environmental footprint or diversifying your workforce to help meet sustainability or cultural goals, your organization could have opportunities to boost cash flow and reduce tax liabilities.

Here are a few example activities:

• Improve energy efficiency in buildings you own or operate

• Design, develop, or improve your products, process, techniques, formulas, or software to enhance your environmental practices

• Cultivate an inclusive workplace culture that supports career development and retention of a diverse workforce

• Invest in solar and other renewable energy projects or affordable rental housing

• Rehabilitate a historic building you own or operate

• Conduct annual board self-assessments and governance best practices training

Why Should You Consider Third-Party Assurance Over Your ESG Reporting?

Stakeholders, including investors, lenders, customers, and employees, value transparency, accuracy, and consistency of ESG issues and related risks at levels equal to a company’s financial reporting.

External assurance will give readers of your report additional confidence in the reliability of reported data and can enhance your brand and business reputation.

Third party assurance can also satisfy the reporting conditions of major customers as well as identify process improvements in the measurement and reporting of ESG metrics.

Justin Neff, CPA, is Partner, Sustainability Assurance Services with Moss Adams LLP. You can contact Justin at Justin.Neff@mossadams.com.

Colleen Rozillis, is Partner, Organizational Planning Consulting Services with Moss Adams LLP. You can contact Colleen at Colleen.Rozillis@mossadams.com.

ESG Strategy

18 The Washington CPA Winter 2023 www.wscpa.org BUSINESS STRATEGY

Member Benefit Provider

CPACharge has made it easy and inexpensive to accept payments via credit card. I’m getting paid faster, and clients are able to pay their bills with no hassles.

– Cantor Forensic Accounting, PLLC

Get started with CPACharge today cpacharge.com/wscpa *** PAY CPA

CPACharge is a registered agent of Synovus Bank, Columbus, GA., and Fifth Third Bank, N.A., Cincinnati, OH. AffiniPay customers experienced 22% increase on average in revenue per firm using online billing solutions

22% increase in cash flow with online payments 65% of consumers prefer to pay electronically 62% of bills sent online are paid in 24 hours

Trusted by accounting industry professionals nationwide, CPACharge is a simple, web-based solution that allows you to securely accept client credit and eCheck payments from anywhere. +

What Young Professionals Want From Your Firm

Understanding the wants and needs of today’s young professionals is key to building a sustainable talent pipeline for your firm of tomorrow.

Annie Mueller

Annie Mueller

Like many industries, widespread effects of the pandemic, changes in business conditions, and new career alternatives are creating a major talent shortage within the accounting profession. Struggling to fill open positions and deal with increasingly competitive recruiting tactics, CPA firms of all sizes are exploring new strategies for attracting and retaining talent. But which strategies actually make a difference to the young professionals that you so desire and require to build a firm that lasts for generations to come?

It’s easy—too easy, really—to make decisions based on generational stereotypes. Sure, in some areas, generational differences are stark, but the pandemic has shifted employee expectations so drastically that even long-standing stereotypes feel outdated today. Putting in the legwork to understand exactly how the next generation of accountants think, and what they want from their employers, is key to building a sustainable talent pipeline for your firm.

20 The Washington CPA Winter 2023 www.wscpa.org HUMAN RESOURCES

"Understanding the wants and needs of today’s young professionals is key to building a sustainable talent pipeline for your firm of tomorrow."

Understanding Generational Gaps

By 2025, Gen Z will comprise about 30% of the global workforce. Before then, the youngest of the millennials are dipping their toes in the workplace waters, while older millennials are rising through the ranks. Making sense of what these modern generations of workers care about when making career decisions has been anything but easy for most, which has led to widespread misunderstandings about how to attract and retain younger talent as well as division and dissatisfaction in the workplace.

“One factor causing this generational divide is the notion that young generations are looking for sexy jobs,” says Will Baker, marketing and CPA experience director at Once Accounting. “What they’re influenced by is doing something of value.” In fact, according to the 2016 Monster Multi-Generational Survey, 74% of Gen Z workers and 70% of millennials “rank purpose ahead of a paycheck.”

The Flexibility Factor

However, purposeful work isn’t the only thing young professionals are looking for. As a result of the COVID-19 pandemic, workplace priorities have forever changed. Now more than ever, flexibility and work-life balance have risen to the top of many young professionals’ career wish lists.

“Young professionals know they can be productive while working on their own terms, and they expect the ability to do so,” says Kiara Schuh, CPA, risk and financial advisory senior consultant at Deloitte. “We’re all adults who know our working styles and our capabilities. That’s just what makes a good professional.”

Of course, financial security—fair wages and good benefits—is important, too. However, it’s just another consideration, not the consideration, says Maria Tranchina, assurance associate at BDO USA LLP: “Paying the bills is important. But getting paid slightly more at a firm that doesn’t provide the flexibility you want isn’t, for most of us, a good trade.”

For that reason, putting the structures and tools in place to enable ongoing flexibility might deserve a higher priority than firms have historically given it. Firm leaders may want to consider these flexibility options:

• Let teams determine their own in-office schedules. “My team is very much on a ‘come as you wish’ basis for being in the office,” Schuh says. “Not every team is like that; some operate on a scheduled rotation.” The point is to allow teams to have the freedom to work in the ways that best meet their project’s—and people’s—needs.

• Keep mandatory in-person meetings to a minimum. We’ve all heard of Zoom fatigue, but in-person meetings can be just as fatiguing and disruptive, particularly for firms that have already adopted hybrid work environments. Consider requiring team members to only travel to the office for necessary meetings and engagements to prioritize their productivity and work-life balance.

• Measure productivity by results, not hours. Focus on your team getting the right things done rather than them putting in a certain amount of face time behind a desk.

• Don’t fall behind on technology. Baker advises delegating new tech implementations, which make greater productivity and flexibility possible, to younger staff to help build the skills they’re going to need in the future.

• Balance remote work with in-person socializing. Regular opportunities to socialize help build camaraderie that carries over to digital interactions. “In-person events, like happy hours, help facilitate that sense of community,” Schuh suggests.

Can You Offer Career Clarity?

Overall, young professionals take their career development seriously and are seeking firms that offer opportunities for varied and new experiences, ongoing guidance, and clear pathways to growth.

Young professionals don’t want to start slowly, says Stephanie Zaleski-Braatz, CPA, an audit manager at ORBA. “I see a lot of young professionals trying to step up to the plate earlier and get as much experience as they can in all aspects of their industry right off the bat,” she says.

Knowing that young professionals want to hit the ground running, Tranchina stresses that it would be very beneficial for firms to prioritize the continuing professional development of their new hires and focus on diversifying their experiences.

21 www.wscpa.org The Washington CPA Winter 2023 HUMAN RESOURCES

Having the ability and support to rotate through different specialties during their first few years with the firm appeals to new hires who haven’t fully determined their career direction. Schuh shares that “a huge factor” in her employment decision was the resources, training, and quality of experience she knew she would get.

Along with honing skills and gaining experience, young professionals want guidance and feedback. “Career path discussions are a huge help,” Zaleski-Braatz says. “It’s an opportunity for leaders to explain how we can help the firm grow and give examples of what other people at the firm have done to be successful.”

This guidance and feedback can range from formal, scheduled meetings to daily, ongoing interactions. “So often, it’s the power of simple conversations, sharing observations, and providing supportive feedback that matters,” says Nicole Szczepanek, CPA, a tax partner at Baker Tilly US LLP and a 2022 Women to Watch Award winner. “These daily interactions can make a difference in not only everyday experiences but in people’s career paths.”

“When young professionals jump ship, it’s often because they don’t know what their next step is,” Zaleski-Braatz cautions. “At some point, they’ll have moved through a variety of work and be ready to specialize in specific areas. The conversations about what their futures are at the firm can’t be overlooked.”

To better support a young professional’s career development, consider these ideas:

• Offer professional development opportunities. Over the past few years, young professionals have experienced major change and expect to go through more. They’re keen to add new skills, expand abilities, and be ready to adapt.

• Don’t squeeze support into a box. “As a leader, look for those everyday opportunities to support your team,” Szczepanek encourages. “It can come in different forms—review notes, a formal meeting, status updates, or going to lunch.”

• Support career milestones. From sitting for the CPA exam to gaining certifications, young professionals value practical help in reaching their career goals.

• Support personal milestones, too. The pandemic has reprioritized life outside of work. For Schuh, the ability to take a sabbatical and pursue a personal project is meaningful. “The firm is supporting me as a person, not just as a professional,” she says.

• Be supportive of the person. A revealing question to ask yourself: Can you support a young professional as a person and help them develop their career in the best way, even if that means they don’t stay with your firm?

Real Relationships Matter

Incorporating the kind of work-life flexibility expected by young professionals requires trust, on all sides. Additionally, providing genuine feedback and career support requires time and sincere interest. In both areas, there can be no progress without sincere, ongoing human connection. This is especially true with young professionals who value building relationships with the people they work with. Schuh says that a big factor in her decision to stay with her employer was the opportunity to connect with people: “From the beginning, I have felt invested in and very valued, which makes me want to stay because I feel like I really have someone in my corner.”

“The role of mentoring and relationships has a huge impact in the attraction, development, and retention of talent,” Szczepanek stresses. “It takes effort. Relationships don’t happen from just sitting back. Firm leaders have to be actively engaged and set the tone for young professionals. It’s important to make sure they have the confidence to speak up, to ask for help, to reach out knowing that they also have a voice.”

On the other hand, Baker adds that being able to learn from someone is of great importance, whether you’re 25 or 55. “When older professionals exhibit a willingness to learn from younger staff, everyone benefits,” he says.

Indeed, continual back-and-forth communication, whether via digital platforms or in person, helps establish real relationships and loyalty. “From my first day, I had people messaging me and scheduling calls,” Tranchina says. “There was never a time when people weren’t effectively communicating and making me feel welcomed.”

There’s no single right way to build real relationships, but it’s made much easier by developing a welcoming firm culture and thoughtful systems that encourage interaction. To help young professionals build relationships at your firm, consider these tips:

• Encourage all types of mentoring. Both formal and informal mentorship helps young professionals learn through experience and meaningful discussion.

• Be deliberate about digital communication. Without daily, casual interactions of in-office work, you have to be more conscious about creating touchpoints through digital means.

• Mind your message. When communicating via digital platforms, body language is lost. Szczepanek advises that we all “think a little more specifically about what we say and how we say it.”

• Facilitate collaboration. Remote and hybrid work environments can hinder collaboration in a team, so it’s important to keep your teams talking. “Keep in mind that many young professionals that started during the pandemic didn’t get to work with people at the same level because of the circumstances,” Zaleski-Braatz says, stressing that it’s important to “find ways to work together more.”

22 The Washington CPA Winter 2023 www.wscpa.org HUMAN RESOURCES

•

Listen to their ideas. The youngest members of your workforce have plenty to learn, and plenty to offer. “If an individual has a good idea, and they’re passionate about it, they should have the opportunity to lead it,” Szczepanek suggests.

Ultimately, firms can attract and retain the dedicated, loyal talent they’re looking for if they’re willing to listen to and understand each generation’s own unique needs. Today’s young professionals value the stability of the accounting profession, but they’re not eager to join firms that aren’t focused on the future. That means offering purposeful work, work-life flexibility, personalized career development, mutual respect, and genuine relationships.

Annie Mueller is an experienced financial writer and principal of Prolifica Co. She works with clients from individuals to large financial companies and is a frequent contributor to various financial and business publications.

Reprinted courtesy of Insight, the magazine of the Illinois CPA Society. For the latest issue, visit www. icpas.org/insight.

illustrations: © iStock/VictoriaBar, © iStock/Natalia Vetrova photo: © iStock/jeffbergen

23 www.wscpa.org The Washington CPA Winter 2023 HUMAN RESOURCES

"There’s no single right way to build real relationships, but it’s made much easier by developing a welcoming firm culture and thoughtful systems that encourage interaction."

Hi, Hello! The WSCPA welcomed 517 new members this year.

3,043 members participated in WSCPA CPE programs and classes.

The WSCPA hosted more than 20 networking events across Washington State.

86 students recieved more than $500,000 in scholarships from the Washington CPA Foundation.

$19,940 was awarded to 3 organizations from the Washington CPA Foundation to increase diversity initiatives in the accounting profession.

The WSCPA advocacy team actively monitored or weighed in on 50 bills during the 2022 legislative session.

•

•

•

• 100GB

•

•

$600/yearvalue! Verifyle’s premium secure online document sharing and messaging service, VerifyleProTM™️, which includes unlimited use of digital signature tools with SMS identity verification is available at no cost to WSCPA members... A $600/year value!

Hindsight might be 20/20, but we had an amazing 2022 at the WSCPA!

Host up to 1,500 workspaces at a time

Detailed document log that shows you when the messages/files were viewed/downloaded

Unlimited file upload

size

of encrypted storage

to customize your account with your logo

The ability

Unlimited document signing for you and your guests (clients and colleagues) To take advantage of this free benefit: Sign up at verifyle.com/wscpa using the email on your WSCPA member account. A free benefit for WSCPA members! 24 The Washington CPA Fall 2022 www.wscpa.org MEMBERSHIP NEWS

Fall Events

Murder Mystery Masquerade

Murder Mystery Masquerade

25 www.wscpa.org The

CPA Winter 2023 PHOTO GALLERY

Not-For-Profit Conference

Washington

Select photos: © Shelly Oberman Photography, illustration: © iStock/Olga Kopylova

Conflicts of Interest Still Cause Trouble for CPAs

Duncan B. Will, CPA/ABV/CFF, CFE

Conflicts of interest have long been a major factor in professional liability claims against CPAs. Part of the problem is that potential conflicts of interest are hard to recognize or identify until something goes wrong. When clients are satisfied, they tend to perceive the CPA as a competent advisor who has their best interests at heart. It’s not until clients become disappointed that their perception of the CPA begins to change. The CPA appears to no longer be prioritizing the client’s best interests. Sometimes the CPA may even appear to have sacrificed the client’s best interests to benefit the CPA or another party to the client’s detriment.

One common claim scenario is that of the CPA advising both parties to a transaction, or helping the parties resolve a dispute. For example, the CPA will sometimes agree to represent both the husband and the wife in a divorce when they are still friendly and cooperative. Many times though, the relationship in a divorce will deteriorate rapidly, and the CPA is then caught in the middle.

The same is true for dissolutions or disputes between business partners. Disputes between partners or owners often result in the CPA’s advice becoming perceived by one of them as favoring the other.

Participating in business deals or investments with clients is another common scenario where everyone is happy while the investment performs well. But as soon as it takes a downturn or falls apart, the client’s perception of the CPA erodes.

Case Study

Consider the following case study (the names have been changed):

For decades, Paul Noble, the founder and managing partner of his CPA firm, had served as a trusted financial advisor to his clients. Like many CPAs, he also had his own personal financial advisor—stockbroker Rich Arrington. Noble frequently shared advice he received from Arrington with his firm’s clients and partners.

Chad Pennyworth, a junior broker at Arrington’s brokerage house, worked with some of Noble’s clients and took on many of Arrington’s accounts when Arrington retired. Noble trusted Arrington’s judgment in Pennyworth’s training and development. Though Noble did not refer any of his clients or acquaintances to Pennyworth, he did inform several of them that he had elected to work with him. Because of Noble’s reputation, many of his clients chose to engage Pennyworth as their own broker when they learned of Noble’s faith in Pennyworth.

Almost immediately after Arrington left, Pennyworth sold Noble some bonds, based on incorrect information that misidentified the bonds’ guarantor as the state, when the bonds were instead guaranteed by a financially challenged local school district.

Pennyworth acknowledged the mistake to Noble, and the brokerage firm agreed to repurchase the bonds from Noble’s portfolio, subject to a nondisclosure agreement, which Noble signed. Noble was pleased when a safer alternative was substituted for the bond investment a couple weeks later.

Two years later though, Noble was troubled when he read of the financial disaster that was all over the news: the local school district’s failure and worthlessness of the bonds the district had guaranteed. Pension funds and investors, including some of his clients, were hurt badly by the losses. Noble felt sorry for the investors but was relieved he had avoided a similar fate.

His relief turned to dismay, as some of his clients called to discuss the impact of the losses they sustained and their intentions to sue Pennyworth and the brokerage house.

RISK MANAGEMENT 26 The Washington CPA Winter 2023 www.wscpa.org

Noble’s hands had been tied because of the nondisclosure agreement. He had not warned his clients of the elevated risk of the bond investment, and his clients were now surprised to learn that he was not “in the soup” with them.

During the class action lawsuit against Pennyworth and the brokerage house which followed, Noble’s initial investment, the reversal of that transaction, and the nondisclosure agreement became public knowledge. Noble’s reputation was ruined. He was now seen as a greedy, self-interested collaborator. Ultimately, Noble and his firm were added to the list of defendants in the class action lawsuit. His former clients alleged that Noble and his firm had a duty to disclose the concerns regarding their investment, had ignored the apparent conflict of interest, and had prioritized their own interests over those of their clients.

Loss Prevention Tips

Recognize and communicate potential conflicts of interests. Project the scenario forward to anticipate what would happen if things were to go wrong. Juries tend to sympathize with clients — especially with the benefit of hindsight and the evidence laid out by a skilled attorney.

Embrace “active ethics.” The CPA should recognize that his or her own personal interests can be adverse to client interests and should not agree to sign nondisclosure agreements without first protecting vulnerable clients. Moreover, disclosing a conflict of interest, while helpful, does not resolve the problem, even if clients acknowledge and sign the CPA’s disclosure regarding the potential conflict of interest. Clients could later argue that their consent was not “informed” by a third party (such as an attorney). Do not get too comfortable with disclosure as a form of protection. In the end, the issue will be whether there is a perception that the CPA’s loyalty to his or her clients waned.

Recognize that there are risks associated with providing referrals. Clients often link the CPA who gives a referral to the professional who ultimately performs the services. In instances where it may be perceived that a CPA is offering a referral, the CPA should be careful to name three or more qualified candidates to perform the service and encourage the client to perform their own due diligence in assessing the suitability of the professionals’ qualifications.

Duncan Will leverages his more than 30 years of experience in accounting, including public accounting, forensic accounting, consulting, and audit and tax compliance. He advises policyholders through the CAMICO Loss Prevention hotline and writes articles on a wide range of topics.

illustrations: © iStock/Steppeua, © iStock/Jiraporn Meereewee, © iStock/murmurbear, © iStock/Panuwat Srijantawong

RISK MANAGEMENT

27 www.wscpa.org The Washington CPA Winter 2023

"...everyone is happy while the investment performs well. But as soon as it takes a downturn or falls apart, the client’s perception of the CPA erodes."

Exploring Excel's Hidden Treasures: LET and LAMBDA Functions

David H. Ringstrom, CPA

Many Excel formulas are quite manageable, but sometimes a formula can end up spanning two or more rows in Excel’s formula bar. Such formulas are tricky to audit and to edit because they often repeat calculations in two or more places. In this article you’ll see how the LET function will enable you to document formulas and eliminate repetitive calculations in Excel 2021 and Microsoft 365. What’s more, you may have complex formulas that are hard to reuse in other spreadsheets because of their complexity. I’ll show you how the LAMBDA function in Microsoft 365 enables you to create custom reusable worksheet functions. Before we get to LET and LAMBDA let’s first review how to name worksheet cells, which works in all versions of Excel, as groundwork. As you’ll see we’ll calculate the volume of a box several different ways so that you can compare and contrast the techniques.

Building the Spreadsheet

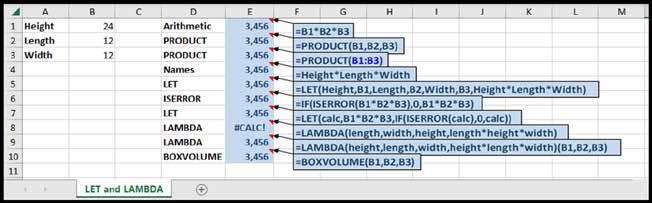

Enter the data shown in cells A1:E4 of Figure 1 into a blank spreadsheet, or download the spreadsheet using the QR code just above this section.

The PRODUCT function multiplies either individual values or ranges of values together in the same fashion as carrying out direct multiplication. This serves as foreshadowing for how LAMBDA functions work, as you will be able to pass information in a similar fashion to your custom worksheet functions. Next enter the formula =FORMULATEXT(E1) in cell F1 and then copy the formula down to cell F3 to display the formulas in cells E1:E3. FORMULATEXT returns #N/A if the cell you reference does not contain a formula, and returns #NAME? in Excel 2010 and earlier.

Most Excel formulas utilize cell addresses in this fashion, as most Excel users are not aware of the concept of naming cells. You can use names interchangeably with cell references, the difference being that names within formulas make it easier to comprehend formulas. The LET function uses a similar concept, although the names only exist within the context of that specific formula. LAMBDA functions utilize parameters, which again serve a similar function.

Figure 1:

28 The Washington CPA Winter 2023 www.wscpa.org

Naming Worksheet Cells

Let’s compare three different approaches for assigning names to cells:

• Select cell B1 and then choose Formulas | Define Name. The Define Name dialog box surmises that you want to assign the text in A1 as a name for cell B1, which you can override if needed, and then click OK

• Select cell B2 and then click into the Name Box, which appears just above the top left-hand corner of the worksheet frame. Type the word Width into the field and press Enter.

• Select cells A3:B3, choose Formulas | Create from Selection

Left Column will be preselected, when means when you click OK Excel will assign the text in the left column of the cell the right column. Click OK to confirm this action.

We could have used Create from Selection to assign all three names at once, but we’ll be using the Define Name command to create LAMBDA functions. Names that you assign to cells will appear in the Name Box when you click on a given cell. Further, you can navigate to a specific name anywhere in a workbook by clicking the arrow in the Name Box and then selecting any name from the list.

Next enter the following text and formula:

Cell D4: Names Cell E4: =Length*Width*Height

You can enter this formula in a couple of different ways:

• Type an equal sign and then navigate to each cell. Excel will display the name instead of the cell reference as you write the formula.

• Press F3 in Excel for Windows to display the Paste Names dialog box or choose Formulas | Use in Formula (unfortunately neither of these options are available in Excel for Mac).

• Type an equal sign and then start typing the first part of a name you have assigned. You can select the name from the AutoComplete list, type out the name in full, or press the Tab key to finish out the name once you’ve entered enough characters to create a match.

Names can be comprised of as little as a single letter. Names must begin with a letter or underscore, cannot contain spaces, and can contain numbers if the name does not correspond to a cell reference. For instance, TAX2023 is not a valid name but TAX_2023 is.

Copy the formula in cell F3 down to cell F4 so that you can compare the approaches. As you can see, names enable you to determine what a formula refers to with a glance, as opposed to chasing down each cell reference. Further names

within formulas are absolute references, meaning if you copy the formula down or across the formula will always refer to the named cell(s), unlike cell references where the row number and or column letter changes unless prefaced by an $ to create an absolute or mixed reference.

Introducing the LET Function

The LET function enables you to establish up to 126 variables, along with one calculation. The calculation needn’t reference all the variables, although typically it will. Variables are established in name pairs, where you assign a name and then a value. Variable names exist only in the context of the individual formula, so as you’ll see we can use Length, Width, and Height within our LET in a different context from the names that we assigned earlier. Enter the following information:

Cell D5: LET Cell E5: =LET(Height,B1,Length,B2,Width,B3,Height*Length *Width)

The formula breaks down as follows:

• Name1: Height is our first variable name

• Name_value1: Cell B1 contains the value that we’re assigning to Height

• Name2: Length is our second variable name

• Name_value2: Cell B2 contains the value that we’re assigning to Length

• Name3: Width is our third variable name

• Name_value3: Cell B3 contains the value that we’re assigning to Width

• Calculation_or Name4: Enter a calculation after you have established the Name and Name_value pairs.

The rules for names within the LET function are like assigning names to worksheet cells: names cannot correspond to a cell reference, must begin either a letter or underscore, and cannot contain spaces. These names will not appear in the Name Box or the Name Manager. The LET function will return #NAME? if your calculation includes a name that you did not assign within the formula or that you misspelled.

Although LET is useful for documenting formulas, an even better use eliminates repetitive calculations within formulas. Enter the following into the respective cells:

Cell D6: ISERROR

Cell E6: =IF(ISERROR(B1*B2*B3),0,B1*B2*B3)

The IF function has the following three arguments:

• Logical_test: a calculation that returns TRUE or FALSE. In this case ISERROR is determining if B1*B2*B3 results in an error such as #VALUE! when a user enters text or a space into cells B1, B2, or B3.

29 www.wscpa.org The Washington CPA Winter 2023 EXCEL SPREADSHEETS

• Value_if_true: In this case if ISERROR returns TRUE we want to return a zero.

• Value_if_false: If ISERROR returns FALSE then we want to carry out the calculation B1*B2*B3

This simple example illustrates how often we end up repeating the same calculation one or more times within a formula. This can make formulas harder to comprehend and harder to edit as well, which raises the specter of spreadsheet errors if edits are not carried out consistently through the formula. This brings us to how LET eliminates repetitive calculations. Enter this formula into cell E7: =LET(calc,B1*B2*B3,IF(ISERROR(calc),0 ,calc)). Now let’s break the formula down:

• Name1: calc is the generic name that I use for calculations such as this.

• Name_value1: B1*B2*B3 shows that name values within LET can be inputs or calculations

• Calculation_or_Name2: IF(ISERROR(calc),0,calc) shows that we can use the word calc as a placeholder for B1*B2*B3. This means that if we need to edit the formula later, we only must edit the Name_value1 argument instead of making multiple edits.

Keep in mind that I used the IF/ISERROR combination as a vehicle to explain LET. The IFERROR function is a better alternative for managing many common errors. Enter this formula in cell F8: =IFERROR(B1*B2*B3,0) IFERROR has two arguments: value, which represents a calculation, and value_if_error, which represents an alternate value, text, or calculation to use if the value argument returns an error.

Introducing the LAMBDA Function

The downside of LET is that you must write each formula from scratch repeatedly. Conversely, the LAMBDA function enables you to formalize the formula so that you simply pass information to a custom worksheet function instead of constantly reinventing the wheel. There are four stages to writing a LAMDBA formula:

1. Writing the formula in a worksheet cell.

2. Passing test values to the formula in the worksheet cell.

3. Formalizing the LAMBDA by using the Define Name command.

4. Utilizing your custom worksheet function in your worksheet.

Enter the following, which I’ll warn you in advance will result in a #CALC! error in cell E8 if you’ve entered everything properly:

Cell D8: LAMBDA

Cell E8: =LAMBDA(length,width,height,length*height*width)

Let’s break down the formula first, and then I’ll explain why it returns #CALC!:

• Parameter_or_calculation: Our first parameter is height.

• Parameter_or_calculation: Our second parameter is width.

• Parameter_or_calculation: Our third parameter is length.

• Parameter_or_calculation: Our calculation is height*width*length.

The reason that the formula returns #CALC! is that we haven’t provided any values for it to reference, which we’ll do on the next row:

Cell D9: LAMBDA

Cell E9: =LAMBDA(height,length,width,height*length*width) (B1,B2,B3)

Notice that you can copy the formula from row 9 down to row 10 and then add the test values (B1,B2,B3) to the end of the formula, which when you press Enter should return 3,456. Once you have tested your LAMBDA, you can now formalize it:

1. Click on cell E8 and then copy the entire formula within the formula bar, including the equal sign. If you use cell E9, copy everything except the test values at the end, meaning (B1,B2,B3)

2. Choose Formulas | Define Name

3. Enter a name such as BOXVOLUME in the Name field.

4. Enter “Computes the volume of a box” in the Comment field.

5. Paste the formula you copied in step 1 into the Refers To field.

6. Click OK

Now enter the following:

Cell D10: BOXVOLUME CELL E10: =BOXVOLUME(B1,B2,B3)

You can now use the BOXVOLUME function anywhere in this workbook. You can transfer the function to other workbooks by copying one or more cells that contain named LAMBDA functions, such as BOXVOLUME , or copying or moving a worksheet that contains such formulas. Remember, LAMBDA functions only work in Microsoft 365 and will return #NAME? in earlier versions of Excel. I’ve only had space to show you to the tip of the iceberg here regarding what’s possible with LAMBDA, but hopefully you can imagine the possibilities.

Introducing the Name Manager

Now let’s choose Formulas | Name Manager. This dialog box enables you to manage names that you’ve assigned in your workbooks and will enable you to manage LAMBDA functions you create as well. The Name Manager enables you to add, delete, or edit new names and LAMBDA functions. One downside of using names in formulas is that deleted names cause formulas to return #NAME?. To see this in action:

EXCEL SPREADSHEETS 30 The Washington CPA Winter 2023 www.wscpa.org

1. Click the Delete button within the Name Manager to delete the Height name.

2. Click OK to confirm the deletion and then click Close

3. The formula in cell E4 will now return #NAME? instead of 3,456. Notice that the formula in cell E5 is not affected because LET maintains its own context for names.

To repair the formula in cell E5 you may either update the formula to use a cell reference or create the name again. Doing so will cause the formula to return 3,456 again.

I hope that I have helped you expand your Excel toolbox. Some years ago I coined the phrase “Either you work Excel, or it works you!” Utilizing features such as naming cells, and functions such as LET and LAMBDA are surefire ways to turn the tide and ensure that you’re not getting pushed around by Excel and are working more effectively.

EXCEL SPREADSHEETS 31 www.wscpa.org The Washington CPA Winter 2023

David Ringstrom (www.davidringstrom.com) is the author of Exploring Microsoft Excel’s Hidden Treasures: Turbocharge your Excel proficiency with expert tips, automation techniques, and overlooked features. David has worked as a spreadsheet consultant for over 30 years and has taught over 2,000 live webinars. illustration: © iStock/VectorMine, Photo: © iStock/AndreyPopov

Upcoming CPE

A selection of WSCPA CPE events scheduled January - April are listed.

To view the thousands of courses and complete details, please visit the CPE & Event Catalog at wscpa.org/cpe.

WSCPA Blue Ribbon CPE Hosted and hand-selected by the WSCPA

DATE COURSE TITLE CREDITS

1/20 Prix Fixe: Creating a Risk Awareness Culture WEBINAR 1

1/23 Tax Advisors Update, Bellevue 8

1/23 Tax Advisors Update WEBCAST 8

1/24 Tax Advisors Update WEBCAST 8

1/27 Prix Fixe: Make Technology Your Secret Sauce WEBINAR 1

2/3 Prix Fixe: Engagement Letters, Disengagement Letters and More WEBINAR 1

2/10 Prix Fixe: Nonprofit Liquidity Management WEBINAR 1

2/17 Prix Fixe: Improving the Appearance, Functionality and Design of Your Home Office or Hybrid Workspace WEBINAR 1

2/23 Member Exclusive: Not-for-Profit Tax Update WEBINAR 1

3/3 Prix Fixe: The Top Liability Issues Facing the CPA Profession Today WEBINAR 1

3/7 2023 Washington State CPA Ethics by Jim Rigos WEBCAST 4

3/8 Member Exclusive: International Women's Day - Women in Leadership Panel WEBINAR 1

3/14 CFO Series: Be the Best WEBCAST 8

3/16 Revenue Recognition: Mastering the New FASB Requirements WEBCAST 8

3/17 Leases: Mastering the New FASB Requirements WEBCAST 8

3/24 Prix Fixe: Market Your Practice Year Round WEBINAR 1

3/30 Governmental Auditing Update WEBCAST 4

4/11 CFO Series: Numbers Rule the World WEBCAST 8

4/21 Prix Fixe: SOC Reporting WEBINAR 1

4/25 CFO Series: Preparing for Growth WEBCAST 8

4/28 Prix Fixe: R&D Tax Credit: How Can Agriculture Qualify? WEBINAR 1

32 The Washington CPA Winter 2023 www.wscpa.org

Governmental Accounting & Auditing Conference April 25-26, 2023

Online CPE

International Tax Conference May 11, 2023

Women's Leadership Summit May 2023

DATE COURSE TITLE CREDITS

1/20 2022 Data Analytics for Accountants & Auditors WEBCAST 8

1/20 2022 Financial Statement Preparation, Compilation and Review Update WEBCAST 8

1/20 2022 The Essential Guide to Partnership & LLCs Tax Return Preparation WEBCAST 8

1/23 2022 Business Fraud Update and Managing the Risk of Fraud WEBCAST 8

1/24 2022 Not-for-Profit Accounting, Auditing & Tax Update WEBCAST 8

1/25 2022 Single Audit and Uniform Guidance Issues Update WEBCAST 8

1/27 2022 Handling IRS Audits and Collections Today WEBCAST 8

1/30 A CPA's Guide to Living With the New Cybersecurity Maturity Model Certification and Crypto Currency WEBCAST 8

1/30 2022 A CPA's Guide to Crypto Currency WEBCAST 4

1/30 2022 Living With the New Cybersecurity Maturity Model Certification WEBCAST 4

1/31 2022 Data Analytics for Accountants & Auditors WEBCAST 8

1/31 2022 Governmental Accounting & Auditing Update WEBCAST 8

2/1 2022 Annual Tax Update WEBCAST 8

2/1 S Corporation Taxation: Comprehensive-Form 1120S WEBCAST 8

2/2 Entity Choice: Tax Considerations of Making Profits Available to Owners WEBCAST 2

2/2 Entity Choice-Federal Tax Consideration of Sale of Business WEBCAST 3