Also in this issue:

– Michael W. Dunagan: Protecting a Lien Holder’s Rights When a Bonded Title Is Applied For

– The CFPB and “Unfair” Subprime Auto Credit

– A Complete Guide to Safeguards Compliance

– Determining Whether a Worker is an Employee or an Independent Contractor

EXPERIENCE PEAK INVENTORY PERFORMANCE

BUY - Source vehicles nationwide confidently with trust and transparency

SELL - Access dealers nationwide who are looking for exactly what you’re selling

VALUE - Get the most up-to-date wholesale pricing in the market

DON’T MISS OUT ON INVENTORY WITH ACV

TIADA Board of Directors

PRESIDENT

Ryan Winkelmann/BJ’s Autohaus

5005 Telephone Road Houston, TX 77087

PRESIDENT ELECT

Eddie Hale/Neighborhood Autos

PO Box 1719

Decatur TX 76234

CHAIRMAN OF THE BOARD

Mark Jones/MCMC Corporate

264 Exchange Burleson, TX 76028

SECRETARY

Vicki Davis/A-OK Auto Sales

23980 FM 1314 Porter, TX 77365

TREASURER

Greg Phea/Austin Rising Fast 8024 IH 35 North Austin TX 78753

VICE PRESIDENT, WEST TEXAS (REGION 1)

Brad Kalivoda/Fiesta Motors

2599 74th Street

Lubbock, TX 79423

VICE PRESIDENT, FORT WORTH (REGION 2)

Greg Reine/Auto Liquidators

39670 LBJ Freeway Dallas TX 75237

VICE PRESIDENT, DALLAS (REGION 3)

Chad Lancaster/Chacon Autos

11800 E. Northwest Hwy Dallas TX 75218

VICE PRESIDENT, HOUSTON (REGION 4)

Russell Moore/Top Notch Used Cars

900 East Davis Conroe, TX 77301

VICE PRESIDENT, CENTRAL TEXAS (REGION 5)

Robert Blankenship/Texas Auto Center

6809 Suite B S IH35 Austin, TX 78744

VICE PRESIDENT, SOUTH TEXAS (REGION 6)

Armando Villarreal/McAllen Auto Sales, LLC

4215 S. 23rd St McAllen, TX 78503

VICE PRESIDENT AT LARGE

Lowell Rogers/11th Street Motors

1355 N 11th St, Beaumont, TX 77702

VICE PRESIDENT AT LARGE

Cesar Stark/S&S Motors 7699 Alameda Ave. El Paso, TX 77915

TexasDealer contents

Volume XXIII / Issue 4 / April 2023

TIADA EXECUTIVE DIRECTOR

Anderson

Austin, TX 78750 Office Hours M-F 8:30am – 4:30pm 512.244.6060 • Fax 512.244.6218 john.frullo@txiada.org Notice to all members concerning services and products: TIADA was established in 1944 to develop professional standards of service and conduct for the independent auto industry. Opinions expressed herein are not necessarily those of the TIADA management, the Board of Directors or the membership. Likewise, the appearance of advertisers or their indemnifications of TIADA does not constitute endorsement of the products or services featured. Editor: Stephen Pallas Magazine Ad Sales: Patty Huber, 512-310-9795 Did You Know? Registration for the 2023 TIADA Conference and Expo is now open! See pages 24-28 for more details. 5 Officers’ Message by Vicki Davis, TIADA Secretary 6 News & Notes 8 On The Cover: 5 Reasons Why Independent Dealers Need to Revisit Their Insurance Policies by Stephen Pallas 10 Upcoming Events 12 TIADA Auction Directory 15 Legislative Bulletin 19 Legal Corner: Protecting a Lien Holder’s Rights When a Bonded Title Is Applied For by Michael W. Dunagan 20 Local Chapters 24 2023 TIADA Conference & Expo 23 TIADA Membership Application 33 Can Theory Be a Substitute for Evidence? The CFPB and “Unfair” Subprime Auto Credit by L. Jean Noonan 36 TIADA Scholarship Application 37 A Complete Guide to Safeguards Compliance by Earl Cooke 43 Determining Whether a Worker is an Employee or an Independent Contractor by Robert N. Parnas, CPA 45 New Members 46 Behind the Wheel by TIADA staff

John Frullo 9951

Mill Rd., Suite 101

officers’ message

by Vicki Davis

A- OK Auto Sales (Porter) TIADA SECRETARY

Who Likes Change? Embracing Business Evolution

Change can be unsettling, but it’s a part of life and necessary for growth. Recently, we had to change our DMS, and although it was not my preference, we had to do it. Adaptability is key in business. Let’s discuss the various changes I’ve experienced since opening my business and how they’ve impacted us.

I remember receiving my first fax and being amazed. Nowadays, faxes are almost non-existent, replaced by email. Email has revolutionized the way we communicate with our customers. We can now send applications via email, making the process more efficient.

Initially, I was hesitant about having a website. However, it’s become an essential part of doing business, providing an online presence for customers to find us. Updating it regularly and posting images of our inventory is crucial. Personally, I prefer using actual pictures of our cars instead of stock photos.

Years ago, cash was king, but now debit and credit cards are the norm. I never thought that would happen. Similarly, social media is now a vital marketing tool. It took some time to adapt to it, but it’s been worth it. It’s challenging to determine which platform performs the best. It’s essential to experiment and find the one that works best for your business.

Texting has become a primary means of communication, and I’ve embraced it. It’s an efficient way to conduct business, from customers asking about a car to making payments. Cell phones have become a vital part

of everyday life, making it easier to work remotely, even from a hospital waiting room.

Over the past 31 years that we have been open, we have experienced numerous compliance changes, and I cannot even begin to recount them all. However, I am immensely grateful for TIADA and its exceptional staff, who have assisted Texas dealers with so much over the years. In light of the latest change, I would like to remind you not to forget to take your safeguard class. TIADA offers an excellent online course that you and your employees can take advantage of.

Change can be uncomfortable, but I believe that it pushes us out of our comfort zones and makes us better. We may not always welcome change, but we must embrace it and move forward, or we risk being left behind. I am confident that no one reading this wants to be left behind. Speaking of being left behind, I would like to remind everyone about our conference scheduled for July 23-25 at the stunning JW Marriott in San Antonio. Not only is this a beautiful property that you and your family will enjoy, but you will also have the opportunity to meet and converse with some of the best dealers in Texas. You can pick their brains on any subject that you need help with or have questions about. You will receive lots of valuable education, and the expo hall will be filled with every vendor you can imagine to help you with all your needs. If you have never attended before, I urge you to give it a try, and I guarantee that you will not regret it.

We may not always welcome change, but we must embrace it and move forward, or we risk being left behind.

5 April 2023 Texas Dealer

John Frullo Appointed TIADA Executive Director

by TIADA Staff

The Texas Independent Automobile Dealers Association (TIADA) is proud to announce the appointment of John Frullo as its new Executive Director. Frullo, a former Texas State Representative from Lubbock, and longtime advocate for small business, will assume the position effective March 20. After earning a Bachelor of Science in Accounting from the University of Wyoming, he went on to become a CPA and spent the next ten years working in the financial, operational, managerial, and regulatory aspects of various businesses. More recently, Frullo has owned and operated a successful and award-winning print, design, and promotional products company.

As Executive Director, Frullo will lead TIADA’s efforts to support and advance the interests of independent automobile dealers throughout Texas. He will oversee the organization’s operations, including legislative and regulatory affairs, education and training programs, and member services.

“I am thrilled to join the TIADA team and work alongside its members to promote and protect the independent

automobile industry in Texas,” said Frullo. “I am very familiar with TIADA and its mission from my time in the legislature. I have been extremely active within my own trade association, and I am very familiar with the important role associations play in the lives of their members.”

Frullo brings a wealth of experience to his new role, having served as a member of the Texas House of Representatives since 2010. He has been a strong voice for the automobile industry, working to promote economic growth and job creation in Texas. In addition, he has served as the Secretary/Treasurer and ultimately chairman of the board for the Printing & Imaging Association of MidAmerica.

“We are excited to welcome John Frullo as our new Executive Director,” said TIADA President, Ryan Winkelmann. “His experience and leadership will be invaluable as we continue to advocate for the independent automobile industry in Texas. We look forward to working with him as we continue to grow our influence.”

6/22 6 Texas Dealer April 2023

news & notes

on the cover

by Stephen Pallas TIADA Director of Marketing and Communications

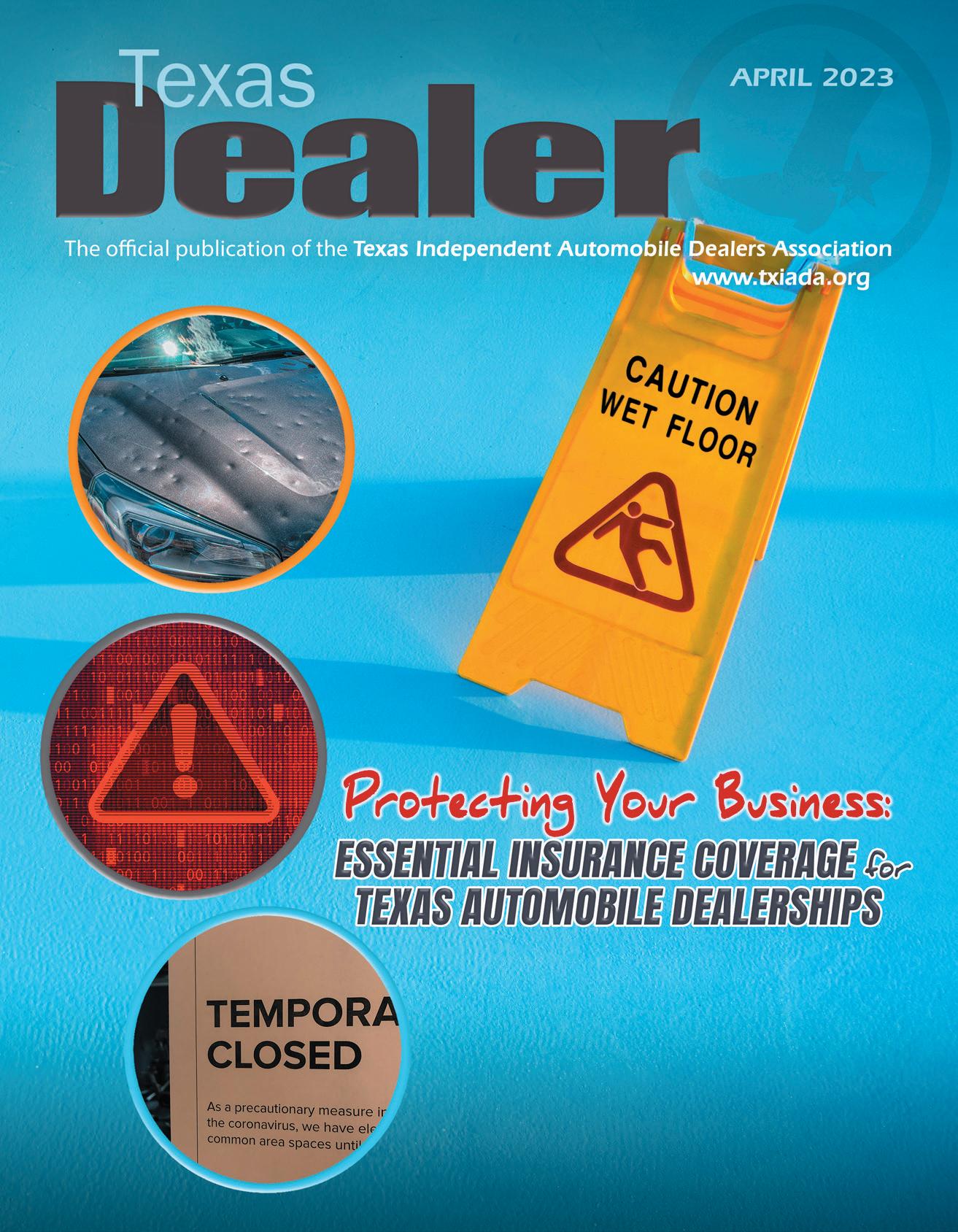

Independent automobile dealerships in Texas are a vital part of the state’s economy. They employ many people and help drive sales of vehicles, which, in turn, help the state generate revenue. However, auto dealerships in Texas face many challenges, including inventory management, marketing, and sales. A critical area that often gets overlooked is insurance. Many auto dealers in Texas

assume they have adequate coverage, but often, this is not the case. We spoke with several insurance company representatives, and they all conclude that it is essential to regularly revisit your policies to make sure they are up to date.

“Some things lend themselves to regular check-ups, and some things do not,” said Ann Mullen, who is the President of Mullen Insurance Agency, Inc.

Texas Dealer April 2023 8

Many auto dealers in Texas assume they have adequate coverage, but often, this is not the case.

“Insurance too often falls into the latter category. With the speed of today’s life and our day-to-day activity, it can be too easy to sign the renewal paperwork, write a check, and move on. That works very well for a lot of dealers for a lot of years. As long as your insurance needs remain unchanged, it is likely your current policy is providing the correct protection—likely, but not positively. And the scary part is that you will not realize where the coverage is lacking until you have a loss jeopardized by inadequate protection. If you have not recently done so, the best time to review your insurance is now.”

With that in mind, we’ve compiled five reasons why auto dealers in Texas need to review their insurance policies.

Liability Risks

Dealerships in Texas face significant liability risks.

Customers can slip and fall on the showroom floor or test drive vehicles, which could result in lawsuits. Additionally, customers can cause accidents while test driving vehicles, leading to potential liability claims against the dealership. Without adequate liability insurance, auto dealerships in Texas risk serious financial consequences.

Liability risks can arise from a wide range of situations that occur in auto dealerships, including showroom accidents, product liability claims, and even employee behavior. Liability coverage protects against these risks, ensuring that the dealership is prepared for any claims that may arise. Adequate liability coverage is essential for auto dealerships in Texas to ensure they can continue to operate and meet their financial obligations.

Property Damage Dealerships also have small or large inventories of vehicles that need protection. These vehicles can be damaged or destroyed by natural disasters, vandalism, theft, or accidents. If an auto dealership does not have adequate insurance coverage for these events, it could result in significant financial losses.

Property damage coverage can help protect against a wide range of risks, including fire, theft, and vandalism. With adequate coverage, auto dealerships in Texas can be confident in their recovery from unexpected events and continue to operate without experiencing significant financial losses.

This is especially important for

independent dealers in Texas, as Andy Harvey, Chairman and CEO of CP Insurance Associates observes, “Over the past 20 years, the Buy-Here-Pay-Here market has grown nationally,” he said. “However, Texas remains the largest marketplace for the BuyHere-Pay-Here dealer.” And that is a refrain we heard in several conversations with insurance professionals we spoke with.

“One common area of property protection that is overlooked by the buy-here-pay-here (BHPH) dealers is insurance coverage protecting the vehicles held as collateral for the installment contracts,” said Kirk Saunders, Director of Sales at American Risk Solutions. “If the borrowers do not provide the physical damage insurance as required by the installment contract, does the BHPH lender have the ability to utilize a Collateral Protection Insurance (CPI) policy to protect the vehicles held as collateral? Are the CPI policy and CPI borrower forms approved by the Texas Department of Insurance? Is the CPI rate adequate to cover the expected losses? These questions are vital to the risk management success of the BHPH lender.”

Cybersecurity

Independent dealers, like virtually all other businesses, also face cybersecurity risks. As dealerships increasingly use technology to manage inventory, sales, and customer data, they become increasingly vulnerable to cyber attacks. A data breach could result in the theft of customer information, including personal and financial data. Such a loss typically leads to lawsuits and/or regulatory penalties, which are likely more costly than the insurance necessary to protect dealers and their clients.

"...the scary part is that you will not realize where the coverage is lacking until you have a loss jeopardized by inadequate protection. If you have not recently done so, the best time to review your insurance is now."

April 2023 Texas Dealer 9

~Ann Mullen, Mullen Insurance Agency, Inc

Upcoming Events 2023

Cyber liability insurance helps to protect against these risks, ensuring that auto dealerships in Texas have the resources needed to respond to a data breach. Cyber insurance can cover the cost of legal fees, notification costs, and credit monitoring for affected customers. It can also help cover the cost of public relations efforts to mitigate the damage to the dealership’s reputation.

Business Interruption

Dealers may also experience business interruption due to unforeseen events like natural disasters, fires, or pandemics. Without adequate insurance coverage, an auto dealership could be forced to close its doors temporarily, resulting in lost revenue and potentially permanent damage to the business.

Business interruption insurance protects against these risks, providing coverage for lost income, ongoing expenses, and extra expenses that may arise during a period of interruption. With business interruption insurance, auto dealerships in Texas can continue to meet their financial obligations and recover from any unexpected events.

Employee Injuries

Dealers also operate with teams of people, and they could face

significant liability risks if an employee is injured on the job. Without adequate workers’ compensation insurance, an auto dealership could be forced to pay for medical expenses and lost wages out of pocket, which could be financially devastating.

Workers’ compensation insurance can help protect against these risks, ensuring that employees (and their employers) are taken care of in the event of an injury. It can cover the cost of medical expenses, lost wages, and rehabilitation services, helping employees get back to work as quickly as possible. Workers’ compensation insurance can also help protect auto dealerships in Texas from potential lawsuits related to employee injuries.

The insurance needs of independent automobile dealerships in Texas are complex and varied. Liability risks, property damage, cybersecurity, business interruption, and employee injuries are just a few of the many potential threats that auto dealerships face. It’s critical for dealers to review their insurance policies regularly to ensure they have adequate coverage to protect their businesses. By doing so, they can have peace of mind knowing that they are prepared for any unexpected events that may arise, allowing them to focus on what matters most: serving their customers and contributing to the state’s economy.

TIADA DEALER ACADEMY Online registration available. www.txiada.org May 8 Keeping Your BHPH Dealership Legal and Compliantl Courtyard Dallas Arlington South 711 Highlander Blvd. Arlington, TX 76015 817.465.5599 OTHER TIADA EVENTS April 24 Board of Directors Meeting Austin, TX July 23 Board of Directors Meeting JW Marriott Hill Country Resort San Antonio, TX 23-25 TIADA Conference and Expo JW Marriott Hill Country Resort San Antonio, TX

Did the ownership at your dealership change and you need to renew your dealer ’ s license? visit TexasDealerEducation.com Texas Dealer April 2023 10

W h y C h o o s e U s ?

•40 Years Serving Texas Dealers

• 4.9 Star Avg. Customer Rating

• Independently Owned

V i s i t U s O n li n e f o r C u s t o m i z e d S o lu t i o n s & H e lp f u l I n s i g h t s

M

. .. . . .. .. . .. . . .... . ...... .. .. . .. ... . . .. .. . . . ... ... . ..... . . . . . . . . . . . . .. .. . . ...... .. ... .. .. . ... . . . . ... . . . ... . . . .. ... .. .. .. ... .. . ... . . ... .. .. .... .. . .. ....... ... .. . .. .. . . ... . . .... ... ... .... ... .. . ... . ... . .. . ... . . . . . .. ... ... . ....... . .. . .. .. .... . ..... ... .. . .. . . . ... . . . . . . ... . . . .... . .. . . .. . .. . .. .. .. . .... . . . . ... . .. ... ....... . . . . . .. . .. .. . . . .. . .. .. .... ... . . .. . . . . .. .. . ... .. . ..... . . . .. . .... . .. .. .. ... . . ... .. ... . . .. ... ... . . . ..... .. . .. . .... . .. .. . . . .. .. ... .. . . . ... ...... .. . .. .. . .. . .. ... .... .... . . . .. . ... .. ... . . .. . .. .. .. . .... ... ...... . . ... ... ... . . . .. . . . .. . .. .... . . .. ..... .... .. . . ..... . .. .. . .

U L L E N I N S U R A N C E

. C O M

V i s i t U s O n li n e f o r C u s t o m i z e d S o lu t i o n s & H e lp f u l I n s i g h t s W h y C h o o s e U s ?

L L E N I N S

M U

U R A N C E . C O M

TIADA Auction Directory

Abilene

ALLIANCE AUTO AUCTION ABILENE

www.allianceautoauction.com

6657 US Highway 80 West, Abilene, TX 79605 325.698.4391, Fax 325.691.0263

GM: Brandon Denison

Friday, 10:00 a.m.

$AVE : $200

IAA ABILENE*

www.iaai.com

7700 US 277, Hawley, TX 79601

325.675.0699, Fax 325.675.5073

GM: Shawn Lemke

Thursday, 9:30 a.m.

$AVE : up to $200 Sell Fee

Amarillo

IAA AMARILLO*

www.iaai.com

11150 S. FM 1541, Amarillo, TX 79118 806.622.1322, Fax 806.622.2678

GM: Shawn Norris

Monday, 9:30 a.m.

$AVE : up to $200 Sell Fee

Austin

ADESA AUSTIN

www.adesa.com

2108 Ferguson Ln., Austin, TX 78754

512.873.4000, Fax 512.873.4022

GM: Michele Arguijo

Tuesday, 9:00 a.m.

$AVE : $200

ALLIANCE AUTO AUCTION AUSTIN

www.allianceautoauction.com

1550 CR 107, Hutto, TX 78634

737.300.6300

GM: Brad Wilson

Wednesday, 9:45 a.m.

$AVE : $200

AMERICA’S AA AUSTIN / SAN ANTONIO

www.americasautoauction.com

16611 S. IH-35, Buda, TX 78610

512.268.6600, Fax 512.295.6666

GM: Jamie McCollum

Tuesday, 1:30 p.m. / Thursday, 2:00 p.m.

$AVE : $200

IAA AUSTIN*

www.iaai.com

2191 Highway 21 West, Dale, TX 78616

512.385.3126, Fax 512.385.1141

GM: Geoffrey Rabb

Tuesday, 9:00 a.m.

$AVE : up to $200 Sell Fee

METRO AUTO AUCTION AUSTIN

www.metroautoauction.com

2221 Hwy 21 W., Dale, TX 78616 512.282.7900, Fax 512.282.8165

GM: Brent Rhodes

3rd Saturday, monthly

$AVE : $200

Corpus Christi

CORPUS CHRISTI AUTO AUCTION

www.corpuschristiautoauction.com

2149 IH-69 Access Road, Corpus Christi, TX 78380 361.767.4100, Fax 361.767.9840

GM: Hunter Dunn

Friday, 10:00 a.m.

$AVE : $200

IAA CORPUS CHRISTI*

www.iaai.com

4701 Agnes Street, Corpus Christi, TX 78405 361.881.9555, Fax 361.887.8880

GM: Patricia Kohlstrand

Wednesday, 9:00 a.m.

$AVE : up to $200 Sell Fee

Dallas-Ft. Worth Metroplex

ADESA DALLAS

www.adesa.com

3501 Lancaster-Hutchins Rd., Hutchins, TX 75141 972.225.6000, Fax 972.284.4799

GM: Eric Jenkins

Thursday, 9:30 a.m.

$AVE : $200

ALLIANCE AUTO AUCTION DALLAS

www.allianceautoauction.com

9426 Lakefield Blvd., Dallas, TX 75220 214.646.3136, Fax 469.828.8225

GM: Robert Kersh

Wednesday, 1:30 p.m.

$AVE : $200

AMERICA’S AA DALLAS

www.americasautoauction.com

219 N. Loop 12, Irving, TX 75061

972.445.1044, Fax 972.591.2742

GM: Ruben Figueroa

Tuesday, 1:00 p.m. / Thursday, 1:00 p.m.

$AVE : $200

IAA DALLAS*

www.iaai.com

204 Mars Rd., Wilmer, TX 75172 972.525.6401, Fax 972.525.6403

GM: Bob Bannister

Wednesday, 9:00 a.m.

$AVE : up to $200 Sell Fee

IAA DFW*

www.iaai.com

4226 East Main St., Grand Prairie, TX 75050 972.522.5000, Fax 972.522.5090

GM: Julissa Reyes

Tuesday, 9:00 a.m.

$AVE : up to $200 Sell Fee

IAA FORT WORTH NORTH*

www.iaai.com

3748 McPherson Dr., Justin, TX 76247 940.648.5541, Fax 940.648.5543

GM: Jack Panczyk

Tuesday, 9:00 a.m.

$AVE : up to $200 Sell Fee

MANHEIM DALLAS**

www.manheim.com

5333 W. Kiest Blvd., Dallas, TX 75236 214.330.1800, Fax 214.339.6347

GM: Rich Curtis

Wednesday, 9:30 a.m.

$AVE : $100

MANHEIM DALLAS FORT WORTH**

www.manheim.com

12101 Trinity Blvd., Fort Worth, TX 76040 817.399.4000, Fax 817.399.4251

GM: Nicole Graham-Ponce

Thursday, 9:30 a.m.

$AVE : $100

METRO AUTO AUCTION DALLAS

www.metroaa.com

1836 Midway Road, Lewisville, TX 75056 972.492.0900, Fax 972.492.0944

GM: Scott Stalder

Tuesday, 9:00 a.m.

$AVE : $200

El Paso

AMERICA’S AUTO AUCTION EL PASO

www.epiaa.com

7930 Artcraft Rd., El Paso, TX 79932 915.587.6700, Fax 915.587.6700

GM: Luke Pidgeon

Wednesday, 10:00 a.m.

$AVE : $200

IAA EL PASO*

www.iaai.com

14651 Gateway Blvd. W, El Paso, TX 79927 915.852.2489, Fax 915.852.2235

GM: Jorge Resendez

Friday, 10:30 a.m.

$AVE : up to $200 Sell Fee

MANHEIM EL PASO

www.manheim.com

485 Coates Drive, El Paso, TX 79932 915.833.9333, Fax 915.581.9645

GM: JD Guerrero

Thursday, 10:00 a.m.

$AVE : $100

Save thousands on buy or sell fees at these participating auctions! * VALID FOR SELL FEE ONLY AT INSURANCE AA LOCATIONS ** ONLINE AUCTION AVAILABLE

Texas Dealer April 2023 12

Harlingen/McAllen

IAA MCALLEN*

www.iaai.com

900 N. Hutto Road, Donna, TX 78537

956.464.8393, Fax 956.464.8510

GM: Ydalia Sandoval

Tuesday, 9:00 a.m.

$AVE : up to $200 Sell Fee

BIG VALLEY AUTO AUCTION**

www.bigvalleyaa.com

4315 N. Hutto Road, Donna, TX 78537

956.461.9000, Fax 956.461.9005

GM: Lisa Franz

Thursday, 9:30 a.m.

$AVE : $200

Houston ADESA HOUSTON

www.adesa.com

4526 N. Sam Houston, Houston, TX 77086

281.580.1800, Fax 281.580.8030

GM: Brian Wetzel

Wednesday, 9:00 a.m.

$AVE : $200

AMERICA’S AA HOUSTON

www.americasautoauction.com

1826 Almeda Genoa Rd., Houston, TX 77047

281.819.3600, Fax 281.819.3601

GM: Ben Nash

Thursday, 2:00 p.m.

$AVE : $200

AMERICA’S AA NORTH HOUSTON

www.americasautoauction.com

1440 FM 3083, Conroe, TX 77301

936.441.2882, Fax 936.788.2842

GM: Buddy Cheney

Tuesday, 1:00 p.m.

$AVE : $200

AUTONATION AUTO AUCTION - HOUSTON

www.autonationautoauction.com

608 W. Mitchell Road, Houston, TX 77037

822.905.2622, Fax 281.506.3866

GM: Juan Gallo

Friday, 9:30 a.m.

$AVE : $200

HOUSTON AUTO AUCTION

www.houstonautoauction.com

2000 Cavalcade, Houston, TX 77009

713.644.5566, Fax 713.644.0889

President/GM: Tim Bowers

Wednesday, 11:00 a.m.

$AVE : $200

IAA HOUSTON*

www.iaai.com

2535 West. Mt. Houston, Houston, TX 77038

281.847.4700, Fax 281.847.4799

GM: Alvin Banks

Wednesday, 9:00 a.m.

$AVE : up to $200 Sell Fee

IAA HOUSTON NORTH*

www.iaai.com

16602 East Hardy Rd., Houston-North, TX 77032

281.443.1300, Fax 281.443.4433

GM: Aracelia Palacios

Thursday, 9:00 a.m.

$AVE : up to $200 Sell Fee

IAA HOUSTON SOUTH*

www.iaai.com

2839 E. FM 1462, Rosharon, TX 77583

281.369.1010, Fax 833.595.8398

GM: Adriana Serrano

Friday, 9:30 a.m.

$AVE : up to $200 Sell Fee

MANHEIM HOUSTON

www.manheim.com

14450 West Road, Houston, TX 77041

281.924.5833, Fax 281.890.7953

GM: Brian Walker

Tuesday, 9:00 a.m. / Thursday 6:30 p.m.

$AVE : $100

MANHEIM TEXAS HOBBY

www.manheim.com

8215 Kopman Road, Houston, TX 77061 713.649.8233, Fax 713.640.6330

GM: Darren Slack

Thursday, 9:00 a.m.

$AVE : $100

Longview

ALLIANCE AUTO AUCTION LONGVIEW

www.allianceautoauction.com

6000 East Loop 281, Longview, TX 75602 903.212.2955, Fax 903.212.2556

GM: Chris Barille

Friday, 10:00 a.m.

$AVE : $200

IAA LONGVIEW*

www.iaai.com

5577 Highway 80 East, Longview, TX 75605 903.553.9248, Fax 903.553.0210

GM: Edgar Chavez

Thursday, 9:00 a.m.

$AVE : up to $200 Sell Fee

Lubbock

IAA LUBBOCK*

www.iaai.com

5311 N. CR 2000, Lubbock, TX 79415 806.747.5458, Fax 806.747.5472

GM: Chris Foster

Tuesday, 9:00 a.m.

$AVE : up to $200 Sell Fee

TEXAS LONE STAR AUTO AUCTION**

www.lsaalubbock.com

2706 E. Slaton Road., Lubbock, TX 79404 806.745.6606

GM: Dale Martin

Wednesday, 9:30 a.m

$AVE : $75/Quarterly

Lufkin

LUFKIN DEALERS AUTO AUCTION

www.lufkindealers.com

2109 N. John Reddit Dr., Lufkin, TX 75904 936.632.4299, Fax 936.632.4218

GM: Wayne Cook

Thursday, 6:00 p.m.

$AVE : $200

Midland Odessa

IAA PERMIAN BASIN*

www.iaai.com

701 W. 81st Street, Odessa, TX 79764

432.550.7277, Fax 432.366.8725

Thursday, 11:00 a.m.

$AVE : up to $200 Sell Fee

ONLINE

C.M. COMPANY AUCTIONS, INC.

www.cmauctions.com

$AVE : $200

San Antonio

ADESA SAN ANTONIO

www.adesa.com

200 S. Callaghan Rd., San Antonio, TX 78227 210.434.4999, Fax 210.431.0645

GM: Clifton Sprenger

Thursday, 10:00 a.m.

$AVE : $200

IAA SAN ANTONIO*

www.iaai.com

11275 S. Zarzamora, San Antonio, TX 78224 210.628.6770, Fax 210.628.6778

GM: Paula Booker

Monday, 9:00 a.m.

$AVE : up to $200 Sell Fee

MANHEIM SAN ANTONIO**

www.manheim.com

2042 Ackerman Road

San Antonio, TX 78219

210.661.4200, Fax 210.662.3113

GM: Mike Browning

Wednesday, 9:00 a.m.

$AVE : $100

SAN ANTONIO AUTO AUCTION**

www.sanantonioautoauction.com

13510 Toepperwein Rd. San Antonio, TX 78233 210.298.5477

GM: Brandon Walston

Tuesday, 10:00 a.m. / Thursday, 1:30 p.m.

$AVE : $200

Tyler

GREATER TYLER AUTO AUCTION

www.greatertyleraa.com

11654 Hwy 64W, Tyler, TX 75704 903.597.2800, Fax 903.597.3848

GM: Wayne Cook

Tuesday, 5:00 p.m.

$AVE : $200

Waco

ALLIANCE AUTO AUCTION WACO

www.allianceautoauction.com

15735 I-35 Frontage Road

Elm Mott, TX 76640

254.829.0123, Fax 254.829.1298

GM: Christina Thomas

Friday, 10:00 a.m.

$AVE : $200

April 2023 Texas Dealer 13

Ensure your staff knows how to protect consumer information to Ensure your staff knows how to protect consumer information to comply with the FTC requirements, avoid inadvertent exposure of comply with the FTC requirements, avoid inadvertent exposure of your customer's information, government enforcement actions, your customer's information, government enforcement actions, lawsuits, and bad press. lawsuits, and bad press. Brought to you by TIADA. Powered by the Dealer Education Brought to you by TIADA. Powered by the Dealer Education Portal. Portal. Visit Visit dealereducationportal.com dealereducationportal.com Or scan the QR Code for info and registration Or scan the QR Code for info and registration S a f e g u a r d s S a f e g u a r d s C o m p l i a n c e C o u r s e C o m p l i a n c e C o u r s e Volume purchase discounts available for purchase of 10+ courses The course is flexible and on-demand to fit your busy schedule All users earn a certificate upon completion Sample policies and agreements are included at no additional charge Keep Your Dealership Compliant with the Keep Your Dealership Compliant with the FTC's Safeguards Requirements FTC's Safeguards Requirements O n l y $ 7 5 f o r t h e Q u a l i f i e d I n d i v i d u a l O n l y $ 4 9 E a c h f o r A l l O t h e r E m p l o y e e s V o l u m e D i s c o u n t s a t $ 4 0 f o r A n y C o u r s e Texas Dealer April 2023 14

legislative bulletin

Bills We Are Watching

The 88th Legislative Session is well under way. TIADA is busy following bills, meeting with members of the legislature, and making sure dealers’ voices are heard at the Capitol. Below you will find a few key bills we are watching:

HB 914 (Hefner) This bill would clarify that it is a criminal offense to issue a temporary tag fraudulently. TIADA is monitoring this bill. STATUS: TIADA is working to make sure members of the Legislature understand that license holders should not face criminal charges for minor offenses, such as issuing a second temporary tag to a customer when the tax office has not processed the title application. NOTE: Please apply for a 30-day permit, and you should never issue a second temporary tag. However, TIADA believes such a mistake by a dealer should not be criminal.

HB 718 (Goldman) This bill would replace temporary tags with metal plates assigned to a dealer. TIADA is monitoring this bill. STATUS: TIADA is working hard to ensure that members of the legislature are aware that this bill would burden dealers who would have to retrieve tags from customers, as some customers are irresponsible in returning to the dealership after the sale.

HB 1235 (Thompson) This bill would require an insurance company to pay for any diminution of value as a result of the accident. TIADA supports

by TIADA Staff

this bill. STATUS: TIADA is working to ensure members of the legislature understand that a crash results in more financial losses then just the cost to repair the vehicle.

HB 1933 (Lujan) This bill would create a process for a dealer to obtain a refund of taxes paid not later than the 30th day after the date of the sale. TIADA supports this bill. STATUS: TIADA is working to ensure that members of the legislature understand this will help dealers help unhappy customers who have buyer remorse or discover an issue with the vehicle after paperwork was submitted to the tax office.

HB 2902 (Gomez) This bill would require TxDMV to provide a warning to users of the temporary tag system that states “unauthorized reproduction, purchase, use, or sale of a temporary tag is an offense.” TIADA supports this bill. STATUS: This bill was introduced after dealers met with Representative Gomez during TIADA’s Day at the Capitol based on their conversation with her.

HB 4142 (Thompson) This bill would provide attorney fees for instances where a lienholder was left off an insurance settlement check when the settlement is paid for a party other than the debtor. TIADA supports this bill. STATUS: This bill was introduced at the request of TIADA.

TIADA’s legislative team will work diligently to keep you abreast of the issues and call on you to act when needed.

15 April 2023 Texas Dealer

March Madness

BRACKET RESULTS

Cars Driving about Best Song and

SB 528 (West) This bill would allow a metal recycler or used automotive parts recycler to purchase a vehicle for crushing or parting without obtaining title to the vehicle or notifying the lienholder if the vehicle is at least 12 years old. TIADA opposes this bill as introduced.

March Madness – Who Will Take the Title?

STATUS: TIADA is working with Senator West’s office to try and find a way to resolve his concerns about disposing of junk vehicles while still ensuring lienholders are protected from bad actors.

SB 224 (Alvarado, Whitmire) This bill would criminalize the possession of two or more catalytic converters that have been removed from two or more different vehicles because law enforcement often stops thieves with catalytic converters in their possessions but are unable to prosecute them due to the inability to trace them back to a particular theft. TIADA supports this bill. STATUS: Senate Criminal Justice heard SB 224 on March 21 and TIADA took the opportunity to drop a card offering its support to the bill. Senator Alvarado offered a committee substitute.

Thanks to everyone who played along and submitted their March Madness Bracket. Congratulations to the winner, Roberta Fisher from Fisher’s Auto Sales in Victoria , who scored 48 points out of the possible 52 points. Above is the final bracket where On the Road Again from our Texas’ own Willie Nelson prevails as the best song about cars and driving. 71% of all entries chose this song as the winner so it’s no doubt a popular one.

Your best source of upto-the-minute information on legislative issues that will affect your industry is the Legislative Action Center, found under Advocacy at the TIADA website, www.txiada.org. As always, we welcome the input of our members regarding legislative matters. TIADA’s legislative team will work diligently to keep you abreast of the issues and call on you to act when needed.

Born to be Wild On the Road Again On the Road Again On the Road Again On the Road Again On the Road Again I Can’t Drive 55 Little Red Corvette Low Rider Low Rider Mustang Sally Life is a Highway Little Red Corvette Life is a Highway Life is a Highway Fast Car Mercedes Benz Drive Hot Rod Lincoln Radar Love Cars Fast Car Cars Cars Highway to Hell Drive Highway to Hell Highway to Hell Highway to Hell Drive My Car Cadillac Ranch

Texas Dealer April 2023 16

PROUD MEMBER OF NATIONALCORPORATEPARTNER GOLD

Texas Dealer April 2023 18

Protecting a Lien Holder’s Rights When a Bonded Title Is Applied For

Dealer Question: I was just notified by the state that someone has applied for a bonded title to a vehicle that has been on my skip list for two years. How do I protect my lien, and will a bonded title wipe out my lien?

Response: We have seen an increase in recent months of dealers/lien holders receiving notice letters from the Texas Department of Motor Vehicles (DMV) regarding applications being filed seeking bonded titles to vehicles that lien holders have been trying to find.

While the issuance of a bonded-title certificate will create an administrative presumption that the bonded title is superior to your lien in the state’s motor vehicle title system, most courts recognize that your prior, unsatisfied lien is still valid. However, the issuance of bonded title in a situation where the applicant is attempting to wash a valid lien may actually provide the lien holder with a better and less costly remedy in recovering its loss than in fighting for possession of the collateral. The surety bond that must be filed with the bondedtitle application has to be issued by a licensed surety company and offers reimbursement for anyone damaged by the issuance of the bonded title.

The bonded title procedure was established by the legislature as a way to allow a person to obtain a title certificate to a vehicle when the original certificate is unobtainable and the applicant is the apparent owner of the vehicle. The procedure presumes that the prior owner and lien holder can’t be found and/or no longer have an interest in the vehicle. We’ve observed that that presumption is often incorrect.

The bonded title legislation addressed a problem many vehicle owners had faced in obtaining title certificates to their vehicles after indebtedness was paid off. The problem was particularly acute when the banking and finance industries were faced with massive shut-downs and consolidations in the late 1980s.

There has also been a persistent problem with other lien holders who go out of business or close down, and can’t be found when the time comes to get liens released. Also, owners often lose title certificates that have been given by lien holders upon pay off, along with the lien release on the certificate. If the lien holder, who properly fulfilled its obligations, is no longer in business when the owner needs the certificate, the bonded title process offers a solution.

by Michael W. Dunagan TIADA COUNSEL

Before institution of the bonded title procedure, the methods for obtaining a title to a vehicle without having a title certificate were (1) apply for and obtain a certificated copy original title (CCO), or (2) request a hearing from the county tax assessor to establish the right of ownership to the vehicle.

The problem with the former procedure is that the owner or lien holder must sign the application and represent that the original title certificate was lost (although this requirement hasn’t stopped many thieves who have no qualms about forging lien holders’ names and lien releases to applications). In examining a number of title histories to vehicles after CCOs were issued, we’ve come across fraudulent business cards or company stationery that appeared to be from the lien holder, naming the CCO applicant as an employee of the lien holder. The cards and stationery, while totally fictitious, were accepted as proof that the thieves seeking the CCOs were acting on behalf of the actual lien holders. Both the signatures on the applications for CCO and the signatures on the releases of lien were forged or totally fictitious. The law is clear that forged or fraudulent documents don’t transfer actual title.

legal corner

April 2023 Texas Dealer 19

The law provides that any registered owner or lien holder can recover from the issuer of the surety bond any expense, loss, or damage occurring because of the issuance of the bonded title.

Local Chapters

CORPUS CHRISTI

G.R. Moore

The Car Shack

(dates announced at www.txiada.org)

EL PASO

Cesar Stark

S & S Motors

Meeting – 3rd Friday (Monthly)

FORT WORTH

Jerry Smith

H J Smith Automobiles

(dates announced at www.txiada.org)

HOUSTON

Robert Edenfield

Mi Pueblo BRP

Meeting – 2nd Tuesday (Monthly)

SAN ANTONIO

Jose Engler

Irving Motors Corp

(dates announced at www.txiada.org)

A tax assessor hearing on an application for title at least offers an opportunity for questioning of the proof provided to show ownership and the invalidity of any recorded liens. Also, some tax assessors are reluctant to cause a new title to be issued without knowing more facts than the applicant often has available at the hearing, so that procedure was not always an efficient way to determine the true ownership of a vehicle.

The bonded-title procedure seemed to be a good compromise for allowing a person to get a title when the normal channels were not available, but at the same time offering financial protection for a real owner or lien holder whose interest was overlooked.

Under Section 501.053 of the Texas Transportation Code, a person may file a surety bond issued by a licensed surety company in an amount equal to one and one-half times the value of the vehicle. If the paperwork is in order, a title certificate is issued.

Usually, a notice of the filing of the bonded title application is sent by the DMV to the registered owner and lien holder prior to the time the bonded title is issued. The registered owner and/or lien holder are given the opportunity to oppose the process by filing a petition in a county or district court to seek a declaration of proper ownership (a costly and potentially time-consuming process.)

The law provides that any registered owner or lien holder can recover from the issuer of the surety

bond any expense, loss, or damage, including reasonable attorney’s fees, occurring because of the issuance of the bonded title. The bond is valid for three years from its effective date. What has become apparent is that the bonded-title procedure is being used in situations other than where lien holders have disappeared. It seems that more and more debtors are “selling” their vehicles to third persons, often posting them for sale using social media postings. The individuals who are “buying” the vehicles are often turning over

large sums to purchase the vehicle without obtaining title certificates or investigating whether there are outstanding liens. When the buyers later seek to title and register the vehicles, they are informed that they can’t because of outstanding liens. Most tax offices then give out information on alternative means to obtain title, including tax office hearings and bonded title procedures, and often give a list of surety companies that write bonds.

Texas Dealer April 2023 20

What has become apparent is that the bonded-title procedure is being used in situations other than where lien holders have disappeared. It seems that more and more debtors are “selling” their vehicles to third persons, often posting them for sale using social media postings.

We’ve also seen situations where vehicle-lien debtors obtain bonded titles to present to cash-for-title lenders to secure loans without having to pay off balances owed. The lenders then obtain new title certificates reflecting themselves as first lien holders.

If state motor-vehicle records indicate that a vehicle has a lien that is less than ten years old, the surety bonding company is responsible for insuring that the lien has been satisfied or released. We’ve found that some surety companies that issue the bonds often do no investigation as to the existence of liens or whether they’ve been satisfied.

Once a lien holder gets notice that a bonded title has been issued, it can obtain information about the applicant and the issuer of the bond from VTR.

We have assisted a number of lien holders recently in collecting

written-off balances on collateral long given up on. When a lien holder finds that a bonded title has been applied for, we suggest the following options:

If the bonded title has not been issued yet, the lien holder can certainly repossess its collateral under the usual repossession rules. Repossessing after a bonded title certificate has been issued, even though probably justified under the law, may result in costly repercussions, such as theft charges being filed. Remember that the police (and other law enforcement officials) will generally rely on the state’s title records and will probably not understand the complications of competing title interests. We often recommend the sequestration process to get a vehicle back via court order to avoid confrontations with law enforcement agencies on a repossession.

If a lien holder finds out that a bonded title has been issued, the legitimate lien holder should consider making a claim against the surety company that issued the bond, presenting evidence of the valid prior lien and the balance owed against the vehicle. Unlike a claim on a dealer bond, a court judgment is not required to recover. However, if the surety company balks at paying, it may be necessary to file suit. Attorney’s fees and court costs can be sought as additional damages.

Michael W. Dunagan is an attorney in Dallas, Texas who has represented the Texas Independent Automobile Dealers Association for over 45 years. He has written a number of books and hundreds of articles for trade journals and law reviews. His clientele includes dealers, banks, finance companies, auto auctions and credit unions.

C M Y CM MY CY CMY K EPI-TIADAhalf APR2023.pdf 1 3/13/23 12:06 PM Texas Dealer April 2023 22

April 2023 Texas Dealer 23

JULY 23-25, 2023 SAN ANTONIO, TX

FEATURED DEALER SPEAKERS

Kendra Brown

Brown Family Auto Sales (Houston, TX)

How to Identify and Eliminate Waste at your Dealership

Kendra will show you how to eliminate operational inefficiencies and streamline processes to make your dealership more organized and productive.

Jason March

March Motors (Jacksonville, FL)

Reducing Employee Turnover at Your Dealership

If you want to get everyone on board with your dealership’s mission, vision, and values, don’t miss out on Jason’s advice about having a shared philosophy that fosters employee engagement.

Marshall Zoerner

Freeman Motor Company (Salem, OR)

Building a High-Performing Sales and Management Team

Marshall knocked it out of the park in 2022 and is back at this year’s conference with up-to-date industry metrics to make sure you have — and retain — a well-trained staff, outlined expectations, and the best customer service.

FEATURED SPEAKERS

BILL ELIZONDO

5 Ways to Increase Opportunities for Better Collections Relationships

CYA: Cover Your Assets! (aka What Kind of Insurance Do I Need?)

Mastering the Single Point of Contact: Elevating the Customer Experience

BHPH MANAGEMENT

SPECIAL FINANCE & RETAIL

TOM KLINE

24 Texas Dealer April 2023

SEAN BAKER

KEYNOTE

TUESDAY GENERAL SESSION

Smoke leads Cox

Automotive’s economic industry insights team, which tracks the economy, new and used vehicle sales, supply, prices, retail and fleet demand, consumer credit and auto financing, and dealer sentiment to understand the key trends impacting both the wholesale and retail markets for vehicles informed by the proprietary data from all of the company’s businesses and platforms including Manheim, Autotrader, Kelley Blue Book, vAuto, Xtime, and Dealertrack.

For more than 28 years, Smoke has focused on translating data and trends into relevant, actionable insights for the industries that represent the biggest purchases that consumers make in their lifetimes: real estate and automotive.

NUMBERS T O K N O W

30+

COMPLIANCE MARKETING/TECHNOLOGY

VENDORS IN THE EXPO

HOURS OF EDUCATION

120

320

INDEPENDENT AUTOMOBILE DEALERS IN ATTENDANCE IN 2022

Jonathan Smoke

FTC’s Proposed Motor Vehicle Dealers Trade Regulation Rule How to Get More Customers in the Digital World / Como Conseguir Mas Clientes en el Mundo Digital FEDERAL TRADE COMMISSION NICOLA BRIANI 25 April 2023 Texas Dealer

Texas Dealer April 2023 26 PLATINUM

Thank You

April 2023 Texas Dealer 27 SPECIALTY ACV – Happy Hour Bar ADESA – Hotel Key Card ADVAntAgE AutomotiVE AnAlytiCS – Happy Hour Bar BACklotCArS – Happy Hour Bar CArS Com – Happy Hour Appetizers innoVAtion FinAnCiAl SErViCES – Happy Hour Appetizers eBAy – Lanyards mEtro Auto AuCtion – Meeting Directional Signage PrimAlEnD – Meeting Digital Signage BRONZE AFC AGORA Data, Inc. ALLDATA American Auto Protection AutoSweet AutoAction Software AutoRaptor Butler & Sanchez, LLC C&M Coaching CAR Financial Services Carbly CARCARE Promotions CARFAX CarPay CMOR Solutions Coverlay Manufacturing Cox 2M Glo3D, Inc Gomez Law PLLC Ignite Consulting Partners iPacket Kinetic Advantage Leucadia Solutions LHPH Capital Mid-Atlantic Finance Company NCC-National Credit Center North Texas Tollway Authority Peak Performance Teams PFS Auto Finance of Texas Profilocity Protective Asset Protection SearchLab Digital Inc. SGC Accounting SiriusXM Space Auto Spectrum VoIP T ax Refund Services – Tax Max TrueRI Verifacto Vision Dealer Solutions W. Walker Auction Group Waymer & Associates Insurance Williams & Stazzone Insurance Agency, Inc. GOLD SILVER Sponsors

Texas Dealer April 2023 28

Keeping Your BHPH Dealership Legal & Compliant

Dealer Academy

One of the quickest ways to ruin a dealership’s profit margin is to be hit with a fine from a regulatory agency, or to lose a lawsuit filed by a customer. This seminar will focus on the practical side of compliance that understands you have a business to run — and you want to run it right.

This seminar from TIADA attorney Michael W. Dunagan is the final answer in BHPH compliance. Mike speaks dealer, and with 45 years of experience representing hundreds of BHPH dealers, he knows your business inside and out.

Attend this workshop and learn all about:

• How to prepare for (and survive) an OCCC exam

• What to do when the Bankruptcy Notice arrives

• Repossessions: from A to Z

• Properly handling financing on repairs

• Real-life DTPA court cases

• Body shops, mechanics, towing and storage issues

A Lien Holder’s Legal Guide.

Time 9:00am - 4:00pm

Cost $249 Members, Each Additional $199 (must be from same dealership) $498 Non-members

Sponsored by:

• TxDMV Enforcement –Title Management Issues

• Most common advertising violations

• Your right to insurance proceeds

• Using the courts to get your car back

• Procedures to stay off the CFPB’s radar

• Techniques to avoid consumer lawsuits

• Specific lien-protection steps

• Federal regulations affecting BHPH dealers

• Alternatives to traditional insurance

• Most common OCCC customer complaints

• How to respond to an attorney demand letter

Monday, May 8, 2023

Arlington, Texas

Courtyard Dallas Arlington South 711 Highlander Blvd. | Arlington, TX 76015 817.465.5599

• Dealer issues in Comptroller audits To

April 2023 Texas Dealer 31

register visit Txiada.org or by phone at 512.244.6060

.

Presenter

Michael W. Dunagan, TIADA General Counsel, author of Dealer Financing of Used Car Sales and Texas Automobile Repossession:

Can Theory Be a Substitute for Evidence? The CFPB and “Unfair” Subprime Auto Credit

When I was a young attorney at the Federal Trade Commission, the FTC’s Bureau of Competition was bogged down with some massive antitrust litigation matters. A tongue-in-cheek memo was circulated internally, claiming that the Director of Competition was proposing doing away with the “evidence” requirement as a way of moving big cases. We all had a good laugh.

I now worry that the old satirical memo has resurfaced at the Consumer Financial Protection Bureau, and the CFPB didn’t understand it was a joke. Why? My concern is based on the CFPB’s legal theory in one part of a recent federal district court complaint against a subprime auto creditor.

We all know that dealers often sell contracts with high-credit-risk customers to creditors at a discount. This practice occurs when the finance charge and interest rate on the contract are not high enough for the creditor to cover its risk if it pays the dealer the face value of the contract. Without a discount, it’s difficult or impossible, in many cases, for dealers to obtain credit for those customers to buy a car.

This practice once gave rise to “hidden finance charge” litigation and regulatory changes. If a dealer passed on this discount to a customer by raising the sales price of the car, courts and regulators called this increased amount a hidden finance charge because it was really a cost of credit and not the cost of the car.

Regulators (originally the Federal Reserve Board but now the CFPB) made clear in Regulation Z that any amount added to the sales price of a financed purchase based on this discount must be disclosed as part of the cost of credit in the finance charge and annual percentage rate disclosures. That rule has been settled for a long time.

Reg. Z sets very clear rules for dealers who must sell a subprime contract to a finance source at a discount: If the dealer increases the sales price of the car based on the discount, that increase is a finance charge and must be disclosed as such and reflected in the APR.

If the dealer simply absorbs the discount, the discount is not a finance charge. Similarly, if the dealer treats discounts as a cost of doing business and

Featured Presenter

L. Jean Noonan Partner Hudson Cook, LLP

increases the prices of all its cars, no consumer pays more because of a discount in his or her specific deal, and thus there is no hidden finance charge.

These rules brought much-needed clarity to the credit cost disclosure issue and make sense both legally and as a policy matter. The CFPB retained these rules when it assumed responsibility over the regulations implementing the consumer financial protection laws. But the CFPB now seems to find its own rules inconvenient.

In a recent lawsuit, the CFPB and the New York attorney general allege that Credit Acceptance Corporation (CAC) has misled consumers as to the cost of credit and charged them substantially more than the stated APR. It does this, according to the complaint, by “hiding” part of the finance charge in the cash price.

These allegations are difficult to prove. If a car dealer advertised and sold a car for one amount for cash and a higher amount for credit, the difference in prices would clearly be a finance charge. But most auto sales involve negotiation. Identical cars can sell for different amounts at the same dealership, whether due to customer negotiation, dealer inventory considerations, or other factors. When inventory is low and demand is high, the dealer sometimes holds out for a better selling price. Other times, the dealer may be willing to accept any reasonable offer to move the car off the lot. If cars often sell for less than the sticker price, proving the “cash price” can be a challenge.

This is where the CFPB and the New York AG get creative. Why bother with the work of alleging actual facts (let alone proving them) if you can simply assume the conclusion of a hidden finance charge by claiming that CAC creates an “incentive” for the dealer to hide the finance charge in the cash price?

What Does the Law Say?

It is useful at this point to take a quick look at exactly what the CFPB’s own regulation and official interpretation have to say. In explaining what a finance charge is, Reg. Z says it includes the following:

Charges imposed on a creditor by another person for purchasing or accepting a consumer’s obligation, if

33 April 2023 Texas Dealer

feature

the consumer is required to pay the charges in cash, as an addition to the obligation, or as a deduction from the proceeds of the obligation.

This means that if the dealer makes the consumer pay CAC’s discount fee, that fee is a finance charge. The official interpretation explains further: Costs of doing business. Charges absorbed by the creditor as a cost of doing business are not finance charges, even though the creditor may take such costs into consideration in determining the interest rate to be charged or the cash price of the property or service sold. However, if the creditor separately imposes a charge on the consumer to cover certain costs, the charge is a finance charge if it otherwise meets the definition. For example: (i) A discount imposed on a credit obligation when it is assigned by a seller-creditor to another party is not a finance charge as long as the discount is not separately imposed on the consumer. Now we see clearly that a dealership that discounts

someone pays me cash for services, has the person incentivized me to cheat on my taxes? And if I do, is my employer or customer who paid me responsible for the penalties I incur from the IRS if I get caught? If the Highway Department builds a smooth, straight, and wide road, has it incentivized me to speed? And if I do, is the Highway Department responsible for my speeding ticket?

But the theory quickly gets weirder. What if I don’t cheat on my taxes or speed, but some other people might think about cheating or speeding. Is the employer or customer or the Highway Department still liable because it created a so-called incentive?

Incentives—or temptations—are everywhere. But incentives are not a substitute for evidence of law-breaking. We have laws and rules to discourage wrongdoing. When the wrongdoing could happen by a business associate, we have ways to control misconduct. Contractual provisions and sanctions are common tools for telling an associate you are serious about compliance. Provisions prohibiting a dealer from passing on to a consumer, directly or indirectly, a discount provided to an assignee are common in dealer agreements. Even without the risk of losing a finance source, a dealer has plenty of reasons to play by the rules. After all, the Truth in Lending Act and Reg. Z give consumers the right to sue dealers for hiding a finance charge in the cost of financed goods.

The CFPB and New York AG complaint has lots of charts and graphs that purport to illustrate how this incentive might work.

certain auto finance contracts it sells is allowed to spread those costs across its inventory as a cost of doing business. But if the dealer imposes the discount fee separately on the consumer, it is a finance charge. This official interpretation sets out a sensible rule that dealerships have been able to follow. But the CFPB and the New York AG do not think they should have to follow it.

What Does the Complaint Say?

The agencies were no doubt aware that proving both that dealers were imposing the discount on consumers “separately” and that CAC knew this had happened would be hard. But the agencies came up with a shortcut! They claimed that CAC “incentivizes” dealers to inflate the cost of the vehicle, and the inflated amount is a hidden finance charge. In effect, the agencies want to claim that giving a dealer an incentive to increase the car’s sales price is the same as proving the dealer broke the law. And because CAC provided the incentive, CAC is the guilty party. Hmmm. That’s a scary legal theory, if it works. If

But these explanations are based on the government’s wishful thinking about what dealers’ prices should be, not reality. The complaint even has a neat formula that the agencies claim produces the “true” cash price for each car. But that formula assumes that a single “true” cash price exists and ignores the price negotiated between the dealer and the consumer. If a dealer sells identical cars for cash to you and to me for different prices, which of us paid the “true” cash price?

Conclusion

There are other issues in the CAC complaint, but this is the one I’m watching with concern, if not outright dismay. CAC is fighting the charges, so we may get to see what the court has to say. I hope a court never decides that dispensing with an “evidence” requirement is a fine way to move along big cases.

L. Jean Noonan is a partner in the Washington, D.C., office of Hudson Cook, LLP. Jean can be reached at 202.327.9700 or by email at jnoonan@hudco.com. This article appeared in Spot Delivery®. Reprinted with express permission from CounselorLibrary.com. Jean will be a featured speaker at the TIADA Conference on Tuesday, July 25, 2023. To register for this year’s conference, visit www.tiadaannualconference.com.

34 Texas Dealer April 2023

A u t o De a l e r S o l u t i o n s

ATTENTION STUDENTS!

$1,000 Marvin Norwood Scholarship DEADLINE

May 13, 2023

{Applications and/or any required documents received after May 13, 2023 will NOT be accepted.}

Criteria and Guidelines

1. Each applicant must be entering or currently enrolled in an accredited college or a trade school. Proof of enrollment must be included with this application.

2. Each applicant must provide a letter from their TIADA member sponsor that includes the sponsor’s address and phone number.

3. Each applicant must complete the application form.

4. A copy of high school transcripts is required for applicants who are college freshmen. If applicant is currently enrolled, provide college transcripts with official university imprint.

5. Provide a detailed description of participation in any academic, honorary, civic or extracurricular activities in college. In addition, a detailed description of high school activities is required from college freshmen along with a college acceptance letter.

6. Compose an essay of no more than two typed, double-spaced 8 ½” x 11” pages. The essay should discuss the applicant’s relationship with their TIADA scholarship sponsor, current education goals and future aspirations as it relates to the applicant’s subject/training area.

7. Provide at least two (but no more than three) letters of recommendation, no older than one year, from college/high school faculty, employers or other appropriate sources (not related).

Date:

Name:

Address:

SCHOLARSHIP APPLICATION

DOB:

City: State: Zip:

Email:

(You will receive an email confirmation of receipt.)

Telephone Number:

High School Last Attended: Address:

City: State: Zip:

Dates of Attendance:

Date of Graduation:

Other High Schools Attended (Names and Addresses):

College(s) you are attending or plan to attend for admission:

Parents Name(s):

TIADA Member Name (Sponsor):

TIADA Member Company Name:

TIADA Member Address:

City: State: Zip:

Sponsor Signature

Should you have any questions, please contact TIADA at 512.244.6060. Please return the completed application with all required documents to:

TIADA

Attention: Scholarship Applications 9951 Anderson Mill Rd. Suite 101, Austin, TX 78750

Texas Dealer April 2023 36

A Complete Guide to Safeguards Compliance

by Earl Cooke TIADA Director of Compliance and Business Development

The deadline for full compliance with the Federal Trade Commission’s (FTC) “Safeguards Rule” was December 9, 2022, however the FTC gave dealers an additional 6 months to make the new deadline June 9, 2023. Just prior to the old deadline, numerous dealers reached out to TIADA for guidance. If you have not already implemented the requirements of the Safeguards Rule, please start implementing them immediately and do not wait until June as it will be here faster than you expect. Although the FTC is unlikely to check for compliance at most dealerships, this rule can be enforced in other ways. The most common enforcement methods will likely be plaintiffs’ attorneys and Texas’s Attorney General bringing action under the Texas Deceptive Trade Practices Act. Texas Attorney General Ken Paxton has already filed lawsuits against other companies alleging failure to implement reasonable security practices and failure to provide notice of the breach. Additionally, complying with the Safeguards Rule will help you prevent data breaches which are becoming all too common. In fact, recently fraudsters pretended to be two different state agencies and sent out phishing emails to dealers.

The Safeguards Rule requires dealers to implement policies and practices based on their size and complexity, which has resulted in some larger dealer groups spending over a million dollars to be ready for the Safeguards Rule. Many of the larger dealers are ready, and based on the calls I have received, smaller dealers without IT and in-house counsel are having the most difficulty figuring out what they need to do. To help smaller dealers, I spoke with the technical staff of several large groups for practical guidance and have incorporated their advice into this article. With that in mind, in this article, I will discuss implementing the Safeguards Rule on a budget, as everyone can comply with the requirements regardless of their size.

There are several written policies that you should have in place. Templates to develop those policies are available from TIADA through its on-demand Safeguards Qualified Individuals Course, which runs just $75. Those policies are a written Dealership Privacy Policy and Information Security Standards, an Employee Agreement to comply with policies and information security standards (which may also be incorporated into your employee handbook), and a Vendor Agreement. You should add to those templates based on your internal practices. The one thing you should not do

is just go out and buy a generic policy without ensuring your policies match your businesses practices because the FTC was clear in its recent settlement with Passport Automotive Group that “a document that looks nice in a file folder won’t paper over illegal practices.”

Additionally, an unfollowed policy not required by law will create an obligation for you that is detrimental to you in a lawsuit. With that in mind, TIADA drafted these policies only to incorporate what every dealer must do. It is recommended that you add to these templates to create a more robust policy depending on your size. A great free resource to add to these sample policies by incorporating internal practices is https:// frsecure.com/resources/. Also, take this time to consider updating your internal practices to be more robust in areas that make sense.

Your dealership must designate a single qualified individual to oversee the program. The Qualified Individual can be an employee of your dealership or can work for an affiliate or service provider. The person doesn’t need a particular degree or title. What matters is real-world know-how suited to your circumstances. Ask yourself these two simple questions to help determine whom you should make your qualified individual:

Is this the person I would want to oversee the protection of my own personal information?

Is this the person I would want to help my business in the event of a breach?

The FTC recognizes that the Qualified Individual selected by a small business will likely have a background different from someone running a large corporation’s complex system. If your company brings in a service provider to implement and supervise your program, don’t think you are off the hook because the FTC has already stated that “the buck still stops with you. It’s your company’s responsibility to designate a senior employee to supervise that person.”

You need a process for ensuring software is updated, a process to learn of new & known security risks, and a way to manage passwords. You should make sure to set updates on software to update automatically. Learning new security risks is easy. One way you can do this is to subscribe for free to the Cybersecurity and Infrastructure Security Agency,

feature

37 April 2023 Texas Dealer

which will provide you with email updates on security risks as they are discovered. Passwords should be long and strong. According to the FTC, “that means at least 12 characters. Making a password longer is generally the easiest way to make it stronger. Consider using a passphrase of random words to make your password more memorable, but avoid using common words or phrases. If your service does not allow long passwords, you can make your password stronger by mixing uppercase and lowercase letters, numbers, and symbols.” You should consider using a password manager. One password manager is Microsoft Edge, a free application for Windows 10, but numerous others are available for free or at little cost. Just make sure to use a strong password to secure the information in your password manager.

A process for ensuring consumer information is encrypted at rest and in transit. Encrypt sensitive information that you send to third parties over public networks

(like the internet) and encrypt sensitive information stored on your computer network, laptops, or portable storage devices used by your employees. Consider also encrypting email transmissions within your business. Don’t forget to consider any information your employees hold on their smartphones or other devices they may use in addition to devices owned by your dealership. Strong encryption is built into modern versions of the Windows and OS X operating systems, and it’s also available for some Linux distributions. Both Microsoft and Apple guide how to go about ensuring this is enabled.

The following policies and procedures should be developed , and if you hold information on more than 5,000 consumers, they must be written:

A security risk assessment, which, more simply put, is just taking time to consider where information is stored and possible breaches of that information. Let’s face it; you can’t

formulate an effective information security program until you know what information you have and where it’s stored. After completing that inventory, conduct an assessment to determine foreseeable risks and threats — internal and external — to the security, confidentiality, and integrity of customer information. Among other things, your risk assessment must include criteria for evaluating those risks and threats. Think through how customer information could be disclosed without authorization, misused, altered, or destroyed. The risks to information constantly morph and mutate, so the Safeguards Rule requires you to conduct periodic reassessments in light of changes to your operations or the emergence of new threats.

An Incident Response Plan, which is included in TIADA’s Qualified Individual Safeguards Course. If you want more details on what to do in a data breach, please consult the November 2022 issue of Texas Dealer because Anne Marie Lee-Edwards, who used to help large companies when they experienced data breaches, and is now general counsel for AutoSavvy, produced a great article in that issue to help dealers.

Implement

Multi-factor Authentication. The Rule requires at least two authentication factors: a knowledge factor (for example, a password), a possession factor (for example, a token), and an inherence factor (for example, biometric characteristics). The only exception will be if your Qualified Individual has approved in writing the use of another equivalent form of secure access controls. One method is by setting up multi-factor authentication when the computer is first accessed. While there are better methods of doing this than setting it up for the computer, such as requiring it for every program, those methods are more costly and appropriate mainly for larger

6lanes CONSIGNMENT SALE 750+ units!!! EVERY THURSDAY 9am BUY ONLINE HERE www.theauctionplatform.com DAAOKC.COM 1028 S PORTLAND,OKC 405/947/2886 FEATURING ally Auto/SmartLane Santander Chrysler Capital Avis Budget Group Hertz Corp Auto Finance Holman Remarketing solutions Exeter Thrity Car Rental United Auto Credit Prestige Express Cars & Trucks New and Used Car Dealerships Banks,Credit Unions, Location Services Mercedes Benz of OKC Many More!! 38 Texas Dealer April 2023

dealers. Microsoft Azure is a free/low-cost option for meeting this requirement that is easy to implement. You can learn more about that product at https://azure. microsoft.com/

Perform Safeguards Security Awareness and Training. You can do training in-house or outsource to a third party. When TIADA first saw this requirement, they recognized that many dealers do not have the expertise or time to do in-house training, so we started working on an on-demand option for dealers. For more information on our course offerings, turn to page 14. The courses allow you to pause and pick up where you left off. The Qualified Individual course takes about an hour to complete, and the course for all other employees takes about 30 minutes. The training requirement is ongoing, so you should take the course at least once a year.

Secure Data Destruction, including disposing of customer information in physical and electronic forms. Remember to consider the data on vehicles and WIFI, as this is often overlooked. Remember that the rule requires the deletion of customer information two years after the last time the information is used in connection with providing a product or service to the customer unless the information is required for a legitimate business purpose. If you need help figuring out how long to keep

the information, please reach out to TIADA or visit the blog section of our website and look at articles around the first of the year because every year, we publish a list of how long you must keep information.

One area that is sometimes not considered is customer information maintained in vehicles. There is some debate within the industry about whether or not a dealer is required to wipe data from vehicles. Still, when drafting compliance programs, the best practice is to comply with questionable requirements when unsure if you can do so without too much burden to your operation. If you decide you can comply with this, clear information from your customer’s trade-in vehicle, dealership’s loaners, and repossessed vehicles. Before selling a vehicle or allowing another person to use it, wipe data, including unpairing all Bluetooth devices, resetting the garage door opener, resetting telematics services, and logging out of cloud accounts. Remind customers to clear connections between their devices and the vehicle. The manufacturer’s owner manual should provide the necessary information to clear or wipe data. The vehicle may have a factory reset option that returns the settings to their original state. Alternatively, some services will provide step-by-step instructions and certification that the information has been cleared instead of using the owner’s manual. Finally, no matter what you decide to do with information on vehicles, you may want to have

6/22 39 April 2023 Texas Dealer

the customer sign a statement saying they understand it is their responsibility to wipe the data from the vehicle involved.

Regularly monitor and test the effectiveness of your safeguards. Test your procedures for detecting actual and attempted attacks. For information systems, testing can be accomplished through continuous monitoring of your system. If you don’t implement that, you must conduct annual penetration testing and vulnerability assessments, including system-wide scans every six months designed to test for publicly-known security vulnerabilities. In addition, test whenever there are material changes to your operations or business arrangements and whenever there are circumstances you know or have reason to know that may have a material impact on your information security program. Information on vulnerability testing and how to select a provider was provided by the Senior Architect at MCMC in the October 2022 issue of Texas Dealer. This is one area in which finding a low-cost solution takes work, as it requires hiring a professional.

Establish a system to ensure vendor compliance with their requirements to protect the data you share with them. You should send a questionnaire to vendors and review their controls. Make sure your contract indemnifies you from any data

breach due to the vendor. Develop a tracking mechanism that lists all vendors, contractors, or subcontractors and identifies those that have access to business/confidential, sensitive, and protected information. Depending on your size, this can be as simple as an excel spreadsheet with the information and is regularly updated.

You should send your vendors a questionnaire to help evaluate their compliance with their contractual obligations to you. There are several free options for creating your own questionnaire. Checklists are available from Security Scorecard and Content Snare for free and numerous other resources. You can use those checklists to develop one for yourself quickly.

You need to make sure you learn of any data breaches from vendors. There are several ways to do this, and a combination might be best. One is to monitor websites such as the Texas AG’s website for companies that experienced data breaches. You should also contractually require your vendors to notify you of any data breaches. Overall, the Safeguards Rule requires a lot of effort. Keep in mind you do not have to be a tech guru to implement many of the above requirements. There are numerous resources out there to help even those of us who are not techies and as always keep in mind that TIADA is here to help you if you need it. Please don’t let yourself get overwhelmed and remember Desmond Tutu’s famous words of wisdom: “there is only one way to eat an elephant: a bite at a time.”

ENSURE GROWTH, PROFITABILITY & LONG TERM CUSTOMER LOYALTY WITH OUR BEST-IN-CLASS SUITE OF PRODUCTS PreferredDealerSolutions.com | kevin@preferreddealersolutions.com | 616-238-9220 •Collateral Protection Insurance •Vehicle Service Contracts •GAP Waivers •TIADA Approved CPO Program •Full Claims Administration •Limited Warranties 40 Texas Dealer April 2023

©2023 NextGear Capital, Inc. 1173900 *Certain conditions apply. All rights reserved. All Advances made in California by NextGear Capital are made pursuant to NextGear Capital’s California Finance Lender License, #603G505. How good is a credit line if you can’t use it wherever you need it? Not very, according to most dealers. That’s why NextGear Capital floor plans are accepted at over 1,000 in-lane and online auctions and can also be used for trade-ins and off-street purchases.* Learn more at nextgearcapital.com

Determining Whether a Worker is an Employee or an Independent Contractor

It is critical that business owners correctly determine whether the individuals providing services are employees or independent contractors. Business owners should always consult their tax and/or legal advisor regarding these matters.