NewsAccount

The Magazine of the Colorado Society of Certified Public Accountants

The Ride to the top

ct O / t Sep 1 201

Short Staffed in accounting or finance? We can bring you the right people. Whether your company needs a new CFO or additional accounting staff, we can help you find the right professional.

Rhonda K. Trimble, CPA

Thomas J. Trimble, CPA

Trimble & Associates, Inc. offers you: Over 25 years recruiting candidates at all levels ◆ 12 years experience in “Big 4” public accounting ◆ 23 years total public accounting experience ◆ Expertise in accounting, finance and business consulting ◆

If your business has hiring needs, please call us for a free consultation. Remember - You pay no fee unless you select a candidate through us. Potential candidates - call us if you’re seeking new challenges. Candidates never pay a fee, so email your resume to us at info@trimbleassociates.com. We may have just the right position for you. Whatever your business staffing needs, contact us today at 303-779-5800 or info@trimbleassociates.com Let us put our experience to work for you.

Trimble & Associates, Inc. ◆ Contingency Search for Accounting, Finance & Business Consulting 8400 E. Crescent Parkway, Suite 600 ◆ Greenwood Village, CO 80111 Phone: 303-779-5800 ◆ Fax: 303-779-0808 email: info@trimbleassociates.com www.trimbleassociates.com

2

NewsAccount September/October 2011

Giving Back Kicking off the national Beta Alpha Psi community service event, Project Homeless Connect in Denver, Aug. 11, were, from left, KPMG’s Kristen Piersol-Stockton, CSCPA chair Mike Bearup, Mile High United Way CEO Christine Benero, and Barry Amman, audit partner with KPMG, a primary sponsor of the event. See page 13 for more snapshots.

Contents Features 2 Forging Relationships Across Colorado Chair Mike Bearup reports on his 2011 Chair Tour visits with members.

4 The Ride to the Top Colorado’s Greg Anton becomes the next AICPA chair of the board on Oct. 19.

6 CDOR Update: What’s Up and What’s Ahead A new executive director, tax amnesty, and new online functionality top the list of happenings at the Department of Revenue.

8 Business Friendly Colorado Is Colorado a place where business can thrive? It depends on who you ask.

Departments 20 SEC Corner 22

State of the Industry

24

Classified Advertising

25 Movers & Shakers

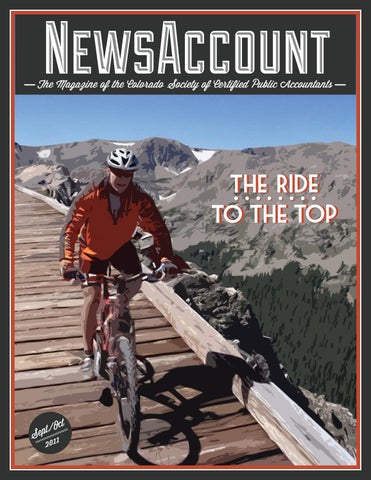

On the Cover Avid mountain biker and AICPA vice chair Greg Anton rides over Rollins Pass near Winter Park, Co. Read about Anton’s journey to AICPA leadership on page 4.

18 The Hazards of Unclaimed Property Knowing the unclaimed property laws in every state you do business in is critical to the sustainability of your business.

September/October 2011

www.cocpa.org

1

News Account A bi-monthly publication of the Colorado Society of Certified Public Accountants Vol. 57, No. 3 September | October 2011

Chair Column

Forging Relationships Across Colorado

Board of Directors Michael S. Bearup, Chair Scott E. Bush, Vice Chair Mark T. Solomon, Treasurer Sidny K. Zink, Immediate Past Chair Mary E. Medley, Secretary Directors Sheila M. Balzer, Stephen R. Corder, Ben T. Hrouda, Gary L. Mitchell, Lori D. Nelson, Christine Riordan Editorial Board Jack Allgood, James M. Boak, Frances J. Coet, Kay R. Dragon, Deanna C. Duell, Jennifer Emerson, Mira J. Finé, Georgia Z. Phillips, Patrick A. Lytle, Mark Paller, Jennifer C. Pitkin, Tawyna Ramirez, Ronald O. Reed, Scott K. Sprinkle, Barbara J. Tedesko, Mark A. Torrey, Gregory A. Truitt, R. Stephen Van Meter, Michael West Mary E. Medley, President/CEO Elizabeth M. Julin, Deputy Director Krista Flynt, Editor/Publisher Natalie G. Rooney, Contributing Writer NewsAccount (ISSN #10899952) is published bimonthly by the Colorado Society of Certified Public Accountants, 7979 E. Tufts Ave., Suite 1000, Denver, Colorado 802372847. NewsAccount is published in January, March, May, July, September, and November and reports information, news, and trends in the accounting profession. Articles, display advertisements, and classified advertisements are due 30 days prior to publication. The Colorado Society of CPAs assumes no liability for readers’ business decisions in reference to advertisements or other information included in this publication. Membership dues include a $9.90 one-year subscription to NewsAccount. Periodical postage paid at Denver, CO. POSTMASTER: Send address changes to NewsAccount, Colorado Society of Certified Public Accountants, 7979 E. Tufts Ave., Suite 1000, Denver, CO 80237-2847. Net press run = 8,850 copies; sales through dealers and carriers, street vendors, and counter sales = 0; paid or requested mail subscription = 8,450; free distribution by mail = 50; free distribution outside the mail = 0; total free distribution = 50; total distribution = 8,500; office use, leftovers, spoiled = 350; returns from news agents = 0; total sum = 8,850; percent paid and/or requested circulation = 99%.

(303) 773-2877 • (800) 523-9082 Fax: (303) 773-6344 E-mail: cpa-staff@cocpa.org NewsAccount is available in PDF format on line at www.cocpa.org.

2

Several past chairs reunited on June 24th at the 2011 Leadership Council meeting. From top left, clockwise: Greg Anton, Mike Bearup, Ron Seigneur, Mike West, Cheryl Wenzinger, Barbara Seacrest, Sidny Zink, and Lynne Lehr-Buck.

I

’m just back from the annual multi-city CSCPA Chair Tour, a whirlwind trip which gave me a chance to visit members around the state. Whether I was giving a formal presentation for CPE, or just mixing and mingling with members, I appreciated getting out of my office and hearing what’s on the minds of my CPA colleagues. Thank you to everyone who came out to greet me in Aspen, Boulder, Durango, Grand Junction, Colorado Springs, Pueblo, and Montrose. I look forward to seeing more of you when I visit northern and eastern Colorado soon.

On the Home Front A lot is going on in the CPA profession on the national side, but state-level issues are front and center on CSCPA members’ minds right now, specifically the situation at the Colorado Department of Revenue (CDOR). During chapter visits, this topic arose repeatedly, and many of you shared your personal experiences with the CDOR and expressed your frustration. It’s clear that this is a difficult situation for Colorado CPAs, their clients, and their companies. The good news is that CSCPA CEO Mary Medley continues to work directly with the CDOR on issues that affect Colorado CPAs. Members at various stops on the Chair Tour said they have used the CSCPA as a resource to successfully resolve problems. If you need assistance with an urgent client matter, e-mail Mary at mmedley@cocpa.org. This is clearly an important issue in the Governor’s office as well. Gov. Hickenlooper recently announced changes to focus on improvement. Barbara Brohl was named the new executive director of CDOR, and her first day was July 18. We are excited about working with Barbara as she assumes her new responsibilities.

The National and International Scene From a big-picture perspective, the Chair Tour gave me the opportunity to talk about some of the national, and even international, issues facing us as CPAs. International Financial Reporting Standards (IFRS) still don’t have a clear path toward adoption or convergence in the United States, which might make us think IFRS will never become a reality here.

NewsAccount September/October 2011

Nonetheless, the issue continues to make its presence known in unexpected ways that CPAs need to consider. For example, we're seeing situations where a European company, which reports in IFRS, buys a Colorado company and expects that employees will be conversant in IFRS. These companies must then train their employees to be knowledgeable about IFRS. Another possibility that brings IFRS to the forefront is the scenario of a Colorado company with global operations. The global subsidiary is already reporting in IFRS, and entries must be booked in consolidation to convert from IFRS to U.S. GAAP. CPAs who have IFRS skills are increasingly being sought out for these and similar reasons. What else do we need to be thinking about as CPAs? On the national level there’s the growing debate over the need for differential private company financial reporting standards and a separate accounting standard-setting board. We need to educate ourselves and make our opinions heard by the profession’s leaders. If you work with the financial statements of private companies, or use private company financial statements, I encourage you to make your opinion known. Visit www.aicpa.org/privategaap for more information.

Making Connections As I spend time with members and think about my own work each day, I’m reminded that our profession is all about relationships and their value. When we asked CPAs at the Leadership Council meeting what the CSCPA needs to keep providing no matter what, the answer came back loud and clear — connectivity. The face-toface connections that come from chapter events, CSCPA roundtables, CPE courses, and social events such as the Young Professionals’ golf tournament are important to you as members. Events like these bring us together, providing us with the ability to build relationships in a world that’s increasingly digital. The CSCPA also is focused on the importance of relationships outside the profession. There is so much that goes on behind the scenes at both the CSCPA and AICPA that doesn’t make headline news but affects you every day. Both organizations make sure to jump in when well-meaning legislation would have unintended but significant negative impact on our profession. It’s through the relationships your professional organizations have carefully formed with legislators, regulators, policy makers, and other constituencies that we are able to have our opinions heard and considered on issues important to our profession. As a professional, I can’t imagine doing without the CSCPA. I hope you see the value too. You may have heard me say this before, and it’s increasingly true: “The CSCPA’s got your back so you can do your business!” s Contact Mike Bearup at mbearup@cocpa.org.

Learn about the new mobility laws which make it easier for you and your firm to practice in other U.S. states and jurisdictions. Go to www.CPAMobility.org, a free joint tool of the AICPA and NASBA.

September/October 2011

www.cocpa.org

3

CSCPA 7979 E. Tufts Ave., Ste. 1000 Denver, CO 80237-2847

The Ride to the Top

Colorado’s Greg Anton En Route to AICPA Chairmanship Over the AICPA’s nearly 125-year history, 99 individuals have taken the helm. Already, three of them — Clem W. Collins, Marvin L. Stone, and A. Marvin Strait — have hailed from Colorado, a state small in population with a big presence on the accounting profession’s national stage. On Oct. 19, the CSCPA’s Gregory J. Anton, CPA, founding partner of Anton Collins Mitchell LLP, will become the fourth Colorado CPA to chair the AICPA board of directors, putting the Centennial State in the national spotlight once again. Born and raised in a Boston suburb, Greg Anton grew up next to a small lake, boating, fishing, and sailing. He also lived just five miles from a local ski area. It wasn’t much by Colorado standards, 300 vertical feet and one chair

4

lift, but he learned how to ski and liked it well enough to head to the University of Northern Colorado in Greeley after high school. Greeley was good to Anton, even though he discovered the university was so far from the mountains he did not ski as much as he hoped to while in college. “On the UNC brochure it looked like Long’s Peak was just beyond campus,” he laughs. “They tricked me.” Since he wasn’t spending much of his time skiing, Anton had plenty of time to pursue his education, prepare for his future in the accounting profession, and meet his wife, Julie.

Future CPA Anton took his first accounting class while he was in high school. “I was fortunate

NewsAccount September/October 2011

to have a high school teacher who was actually a business person,” he says. “As a result, the class had a business focus to it instead of being a bookkeeping class, which was typical for that day.” Also, his father had opened and operated a family business. Anton became intrigued with how it worked. He wasn’t sure what his major within the business school would be, “but I was learning how integral the language of business (accounting) is to success in business.” Then, a cousin who was an accounting major told Anton to go to the university’s career services office and see who was hiring. “All of these CPA firms were coming to recruit. It was the perfect combination of wanting to get involved in business, and accounting was an avenue to do so. Account-

ing gave me the ability to put myself in a position to have a job when I graduated.” Right out of college, Anton went to work for Seidman and Seidman, which became BDO USA, LLP, but he always had a vision for his own business. “I never imagined it would be a CPA firm, but that’s the path that led me to business ownership and being an entrepreneur in the profession I grew up in.”

Founding of a CPA Firm In 2002, Anton, along with Jim Collins and Gary Mitchell, formed Denver CPA firm Anton Collins Mitchell LLP (ACM). “We had each other’s best interests in mind,” Anton says. “It was a partnership of three individuals with the same vision and goals.” As Anton talked to clients about the new firm, they let him know what he was in for. “They told me I would really understand what it was like to own a business now,” he remembers. “And that I’d start paying attention to postage and when lights were left on. It creates a different sense of ownership,” he laughs. He also realized being the owner was an entirely new burden in terms of responsibility. “But it’s a good feeling to create opportunities for others and share the success.” Recently, ACM was named a "Fastest Growing Private Company" by the Denver Business Journal and has been recognized as a "Best Company to Work For" multiple times. “If you’re not willing to fail and to put something at risk, you’ll never achieve success,” Anton says of his decision to start ACM. “We were willing, from day one, to take the risk in order to achieve success. In that manner, we were very much aligned with the businesses and companies we work with that evaluate and take risks every day.” The firm celebrated its ninth anniversary in July.

From CSCPA to AICPA How does a CPA go from being a member of a smallish state CPA society to chair of the profession’s national body? “The Colorado Society of CPAs is responsible for it all,” Anton says jokingly. But that’s not far from the truth.

Anton’s CSCPA involvement began when he served as a facilitator and instructor for an SEC reporting course. From that experience, he got involved in other CSCPA committees — including real estate and planning for conferences. Eventually he was asked to join the CSCPA board of directors. He served two terms and was chair during the CSCPA’s 100th anniversary in 2004 – 2005. “It was a great experience,” Anton says about visiting each chapter for centennial celebrations and presenting CSCPA members with pioneer awards. “I learned some valuable life lessons from CPAs who had been practicing for more than fifty years,” he says. As a CSCPA leader, Anton attended AICPA Council meetings. His national involvement included a special board committee to evaluate the peer review process. “It continued from there,” he says.

“If you’re not willing to fail, and to put something at risk, you’ll never achieve success.” He was then nominated to serve on the AICPA board, became chair of the finance committee, and learned all of the financial operations of the organization. “I showed up, I participated, and I tried to make a positive contribution every time,” he says. “In each meeting, I learned something, met new people, and improved myself.”

The National Stage Anton finds it a wonderful coincidence that he served as CSCPA chair during the CSCPA’s 100th year and will now have the opportunity to lead the AICPA during its 125th year in 2012. He’s looking forward to celebrating and says there will be many opportunities for members to be involved.

As for what’s on tap for his leadership year, it’s looking like a full slate of activity ahead. Anton says critical items on the radar include: • Supporting the Blue Ribbon Panel on Private Company Financial Reporting recommendations on differential standards in GAAP and a separate, autonomous standard-setting entity for private companies. Anton says the majority of his clients are privately held companies, and they all see a need for changes. • Rolling out the new global management accounting credential and enhancing the value proposition to members in business, industry, and government.

At Home in Colorado Serving as chair of the AICPA will come with a lot of responsibility and a lot of travel, but Anton plans to make plenty of time for his family, firm, and clients. “I really try to integrate work and life,” he says. “I try to blend things that I really enjoy with work.” Last January, he combined his love of skiing and work by heli-skiing with two clients in Canada. You will also find Anton mountain biking after work and on weekends with his family, coworkers, and clients. He and Julie have two sons: Cam, 18, a freshman at Fort Lewis College; and Jake, 12, who is in middle school and an avid hockey player. The family enjoys skiing together and has a home in Winter Park. As Anton prepares for his term as chair of the AICPA’s board of directors, he reflects on Colorado’s long history as part of the profession’s national footprint. “It’s important that we continue to reach beyond our own state boundaries and support the profession,” he says. A few people have suggested Anton change his first name to Marvin to keep the CSCPA/AICPA tradition alive: AICPA chairs named Marvin (Stone and Strait). The idea makes Anton laugh. He replies simply: “I’m proud to continue Colorado’s legacy of significant involvement at the national level.” s Contact Greg Anton at ganton@acmllp. com or follow him on Twitter with handle @ gregantoncpa.

September/October 2011

www.cocpa.org

5

Colorado Department of Revenue Update

What’s Up and What’s Ahead

Editor’s Note: Since late fall, 2009, the Colorado Society of CPAs (CSCPA) has been working with members and the Colorado Department of Revenue (CDOR) on a wide variety of issues and problems arising from the Department’s multi-year, phased conversion to CITA, the Colorado Integrated Tax Architecture. Efforts have included formal outreach to Gov. John Hickenlooper’s office, regular meetings with the Department’s executive director and senior management, periodic electronic updates to members, assistance in resolving members’ specific client matters, and appointment of a joint CSCPA/CDOR task force to provide practitioner input, develop resources, and collaborate on solutions. To receive the periodic electronic Colorado Department of Revenue updates, e-mail your name and “CDOR Update Distribution List” to Caitlyn Major at the CSCPA office, cmajor@cocpa.org. For priority assistance with an urgent client matter, e-mail CSCPA CEO Mary Medley, mmedley@ cocpa.org. Include the client(s) name(s), last four digits of the SSN(s), tax ID number(s), or the Colorado Account Number(s) (CAN(s), which appear on any letter or notice from the Department), and a brief description of the issue(s). Attach a pdf file of the most recent notice, if available. Medley will forward the email to the Department for immediate attention.

Job One: Customer Service and Effective Communication Barbara Brohl, executive director of the Colorado Department of Revenue, stepped into the role, July 18, 2011, succeeding Roxy Huber in the Department’s top management position. In a recent conversation with CSCPA CEO Mary Medley, Brohl discussed what she’s focusing on early in her tenure. “I keep asking, every time a new issue or approach comes up: How does this impact our customer — the Colorado citizen? How are we informing the customer?” Brohl

6

observes that effective, understandable communication is key in helping taxpayers (and their tax preparers) navigate the new system and comply with the tax laws. She notes that the Department must employ multiple communication methods, including an easily navigable, informative website, to deliver on the Department’s mission: “…to provide exceptional service in an effective and innovative manner that instills public confidence while fulfilling our duties to collect revenues, responsibly license and regulate qualified persons and entities, increase productivity, and assure the vigorous and fair enforcement of the laws of Colorado.” And, she’s well aware that there have been issues, so far, with the conversion to the new system. As did Roxy Huber before her, Brohl acknowledges that the Department could have done a better job, especially in communications with citizens and practitioners. “I know it’s been difficult for everyone involved. We have to get our arms around the notices problems, as one example. We have to prioritize the issues, and we have to make CITA work with limited resources.” Nonetheless, Brohl is optimistic that things will improve and points to the collaboration between her staff and the CSCPA as a way to gain understanding and resolution of issues as they arise. A self-described problem solver, with the background to back up the moniker, Brohl is determined to understand the problems which have vexed taxpayers and tax practitioners and to work with her team, the CSCPA, and others to fix them ASAP. Bet on Brohl to accomplish Job One — with a lot of help.

Tax Amnesty Program Coming On June 3, 2011, Gov. John Hickenlooper signed into law Senate Bill 11-184, which authorizes the Colorado Department of Revenue’s executive director to conduct a tax amnesty program from Oct. 1 to Nov. 15, 2011. Those with overdue taxes can pay the full amount owed, plus half the total interest owed without imposition of any fine or other civil or criminal penalty otherwise

NewsAccount September/October 2011

provided for by law. The program applies to taxes that were due on or before Dec. 31, 2010. It does not include 2010 Colorado income tax, which was due, April 18, 2011. Individuals and businesses in the following situations also do not qualify for the amnesty program: • Tax Delinquency: If the taxpayer receives a delinquency notice on or before Oct. 1, 2011, for a particular tax and filing period, that amount is not eligible. • Criminal Investigation: Taxpayers facing criminal investigation are not eligible. Individuals, businesses, and contractors with unpaid taxes in the following categories are included in the amnesty period: • Personal, corporate, partnership, and fiduciary income taxes • State sales and use tax and the following taxes the Department of Revenue collects on behalf of counties and municipalities: county or city taxes; local marketing and promotion taxes; county lodging taxes; county rental taxes; local improvement district sales taxes; RTD/CD/FD sales, retailer’s use, and consumer use taxes • Gasoline, gasohol, MTBE, special fuel tax, and environmental response surcharge • Fermented malt beverages (3.2 beer) and alcohol beverages • Cigarette tax and tobacco products tax • Severance tax and oil and gas withholding Note that International Fuel Tax Agreement (IFTA) taxes are not eligible for amnesty. The application form to file for amnesty will be available for download at the Colorado Department of Revenue website. No supplemental application or documentation is required, except with amended returns, which will require a special application, also to be found at the Department’s website. All amnesty tax returns must be filed on paper forms.

CDOR Update

Continued on 15 >

Business: Governor Hickenlooper Style

C

olorado Gov. John Hickenlooper recently spoke with NewsAccount contributing writer Natalie Rooney about Colorado’s business environment. Here’s what he had to say about doing business in Colorado, his administration’s initiatives, and how CSCPA members can get involved. What can CPAs do to make sure that companies come to Colorado and thrive here? What is your “ask” of the CPA profession to get great companies to Colorado? CPAs play such a crucial role in almost every business, and business is such a priority right now, so the opportunities are endless. First and foremost, we’re doing a state initiative against red tape. It would be very constructive to hear from CPAs who deal with regulations and reporting requirements to delineate for us what they think the red tape is, not only from a statewide perspective, but also from a federal perspective. This information could then be passed to Senators [Mark] Udall and [Michael] Bennet. Second, we’d like to look at what would be a better, more fair way to tax in terms of the business personal property tax. If we want to get rid of that tax, what would we tax in its place? Any suggestions on how to simplify the tax code for business would be welcome. Finally, many times in business, big innovations come from the To contribute feedback to the Red Tape Initiative, visit www.colorado.gov/ cs/Satellite/OEDIT/ OEDIT/1251590791258.

BY NATALIE ROONEY people looking at numbers. We’re currently working on an initiative with the heads of Colorado’s business schools and national research labs to set up a virtual center of innovation. In the fall of 2012, we’ll be hosting an innovation conference that will bring in CEOs from major Fortune 100 companies who are experts on the subject. The conference will create a network of people oriented towards innovation. We would love input from CPAs as we begin to do that. As we get a greater number of ideas, how do we implement them? We need objective, data-driven information from CPAs and their people involved in managing enterprises. CPAs can take a big role in this. Colorado has a history of being a great place for entrepreneurs and to start a business, but we have a terrible record of keeping businesses as they mature. What can be done to change this? First, we continue through reforming the tax code, reducing red tape, and making it easier to do business. Entrepreneurs build their businesses to a certain point and then want to sell and relax. They often sell to larger companies, to who pays the most, and then they merge their headquarters and move out of Colorado. We’re working hard to find two or three signature companies who are going to move here. About a year and a half ago, Denver attracted DaVita, a Fortune 300 company. We want to provide access to capital and mentors for start-ups. We want to recognize and support companies that are growing in Colorado so they know they are beloved. In your opinion, how important are corporate income tax rates in attracting businesses from outside Colorado? Of all of the states that have corporate income taxes, Colorado’s are the lowest. People get agitated over our corporate income tax rates, but the California and Illinois tax rates are double Colorado’s, which gives us the competitive advantage. How do we not waste what we’ve collected? The Center for Innovation provides ways to maximize. This doesn’t just mean for economic development, but how do you make government more successful? We have the best cabinet in the U.S. It’s a team of people to help us reinvent government around certain principles. We want to be: Effective — when we say we’ll do it, we do. Efficient — do things at the lowest possible cost. Essential — we can’t be all things to all people, but we can do the things that no one else can do or can do effectively. Elegant — both the person receiving the service and providing the service should come away from each transaction feeling better about a successful transaction. We want to drive home that we are in the customer service business — which is no different than when I ran a business. We’re providing our citizens what they need in a positive environment. s

September/October 2011

www.cocpa.org

7

Business Friendly

The classic Colorado bumper sticker says it all: “Not a native, but I got here as fast as I could.” Yes, Colorado is well known for its beautiful scenery, variety of outdoor activities, and quality of life. It’s a place people want to live. But snowcapped peaks aside, is Colorado a place where businesses want to be located? Is Colorado a place where businesses can thrive? The answer: It all depends on who you ask.

In contrast, the 2011 State Business Tax Climate Index from the Tax Foundation, which ranked Colorado 15th, focused strictly on five separate tax indices. It’s important to note that not all indices are apples-to-apples comparisons.

What the Rankings Say

The differences in rankings aside, Colorado has a history of being one of the easiest states in which to start a business and having the least expensive cost of entry. “There’s a simple registration process, a small fee, and you’re in business,” says Tom Clark, executive vice president of the Metro Denver Economic Development Corporation (Metro Denver EDC). “Innovation is based on an economy driven primarily by small business and entrepreneurship. Keeping them from going into business is bad policy, and we’re good at not doing that.” Clark feels that once Colorado attracts a company’s headquarters, the state has very little problem keeping it here. While there have been some corporate moves in recent years, he says, by and large, those companies were in maturing industries and were being rolled up into larger corporations. He cited examples such as First Data, which moved to Atlanta. With its capital base in Europe, the company cut three hours off of its overseas flights with the move. Clark gave MillerCoors as another example. When Miller purchased Molson Coors Brewing Company in Denver, it chose to locate the headquarters of the new business in Chicago over Milwaukee or Denver in order to stay close to the many beer drinkers in Canada. “The company needed to be in a neutral place,” Clark says.

It seems everyone has a poll, ranking, or index to determine which states are the most business friendly. It also seems everyone’s results turn out a bit differently. How does Colorado stack up? One poll on the best states for business ranked Colorado third. One ranking the top 20 states in which to start a small business ranked Colorado as tenth. Yet another ranked the state 15th for its tax climate. Why the big difference among these rankings? Experts say that many times, the science of ranking states turns out not to be a science at all, relying more on subjective decisions from the group conducting the poll. Different indices measure different things, says Mark Robyn, an economist with the Tax Foundation in Washington, D.C. “There are indices that make attempts to compare states more difficult, assessing measures such as workforce quality and living standards.” For example, the CNBC report, “America’s Top States for Business 2010,” which ranked Colorado third, not only included factors such as the economy, access to capital, and cost of doing business, but also more subjective factors such as quality of life, education, and transportation.

8

NewsAccount September/October 2011

A Great Start-Up State

BY NATALIE ROONEY In fact, Clark says Colorado tends to be the most difficult market from which to recruit CFOs. “Headhunters know they’re not going to have a lot of luck getting people to leave the state,” he says.

Where Colorado Gets High Marks If you examine the indices floating around, you’ll see that Colorado gets high marks in areas like quality of life, business friendliness, and economy. “We’ve done some major changes in corporate tax policy and income tax that will stand us well for awhile,” adds Clark, discussing the state’s change to a single factor apportionment. The switch provides a tax savings for companies already located here and an incentive to bring outside companies to the state. Clark also says the state finally has tax credits like other states. The Job Growth Incentive Tax Credit allows employers to write off their share of FICA against their income tax liability. “It puts us on a level playing field with most states in the incentive business,” he says. Prior to the credit, the only incentive Colorado offered corporate headquarters was $800 to conduct employee training. “It wasn’t exactly the best sales pitch,” Clark adds. Robert B. Hottman, CPA, CEO of EKS&H, says Colorado’s strengths include being a great incubator for start-up companies and access to highly educated people. And of course, there’s the Colorado lifestyle, mentioned in so many of the rankings. Hottman notes that it can’t be the only driver of why an organization would stay or move here. “Sometimes we put too much emphasis on lifestyle,” he says, adding that the Colorado business community is open and welcoming, which you don’t always see in other states. “We can’t be provincial in our thinking,” Hottman warns. “What’s good for one is good for all.”

The sixth edition of Metro Denver’s annual benchmark study, “Toward a More Competitive Economy” (TMCC), reports that “Colorado continues to be a center of innovation — with a highly educated workforce that attracts some of the world’s brightest minds. We have made great strides in growing our innovation clusters over the years, particularly in aerospace, energy, and bioscience.”

Areas for Improvement While the TMCC study has praise for Colorado, it also weaves a cautionary tale, advising Coloradans to be mindful of how their decisions at the polls impact the state in the long term. According to the report, “Colorado continues its trend toward becoming a weaker competitor for new jobs and investment. In many respects, the state continues to live off the investments it made in the past.” In addition, the report states that Colorado has moved from a “middle-level” tax state to a “low-level” tax state. Tax increases have been approved by voters at the local level (eighth-highest local tax revenue per capita) while the state’s coffers continue to further deplete (10th-lowest state tax revenue per capita).

Complexity and Technology Problematic “Complexity” is a word that is mentioned over and over again when CPAs discuss the problems they and their clients face when doing business in Colorado. That complexity is something that must be dealt with sooner rather than later if the state is going to thrive.

Business September/October 2011

Continued on 10 > www.cocpa.org

9

Business

Continued from 9

“On the surface, we are an extremely friendly state,” says Joe Bertsch, CPA, tax partner at EKS&H. “We have one of the lowest state income tax rates and the lowest sales and use tax rate. That is attractive.” But as Colorado companies grow, they realize it becomes more and more complex to comply with the tax reporting and payment mechanisms that exist because of Colorado’s home rule structure. “Our sales and use tax is the most complicated in the country,” says Chuck Berry, president of the Colorado Association of Commerce and Industry (CACI). “We give so much flexibility to local governments in terms of base and rate and the point at which they tax. The result is an incredibly confusing system.” This complicated system drives up the cost of doing business in Colorado, says Dan Pilcher, CACI’s senior vice president and chief operating officer. Adding insult to injury is the state’s antiquated information technology structure which frustrates CPAs and their clients alike. Clark doesn’t pull any punches when he discusses the state’s tax collection system which is split between the state and the local communities, all of which have different policies in terms of how aggressively they collect. “If you’re a retail sales tax paying business in Colorado doing business in several communities, it’s a virtual nightmare,” he says. “You combine the complexities the state has with its archaic system, throw in home rule which means you’ve got to know every little rule that relates to an individual’s jurisdiction, rates that are all over the place in terms of what they include or exclude or are exempt from, and you have a complex sales tax system,” Hottman says. “That creates a lot of frustration in Colorado.”

10

Eliminating Tax Exemptions During the 2010 session, the Colorado General Assembly enacted a dozen bills, which were signed by then-Gov. Bill Ritter, that eliminated or suspended various business tax exemptions, credits, and exclusions to close the gap between spending and revenues to balance the 2010-2011 fiscal year budget as required by the Colorado Constitution. Pilcher says the so-called “dirty dozen” were strongly opposed by the business community because the package increased the amount of taxes companies paid by more than $230 million while they struggled amidst the recession. “In tough times you have to make tough decisions, and people are looking for every avenue to balance the budget,” Hottman says, adding that the incentive should be how do we as a state take what we have and streamline, eliminating red tape so we can still provide services, but in a more cost-effective manner so that tax increases aren’t necessary. “A balanced budget is a real strength,” Bertsch agrees, “But you do have to invest to have economic growth and be business friendly. We have to incentivize businesses, or at least not disincentivize them, to come here.” Hottman says he hopes Gov. John Hickenlooper’s red tape initiative is successful so that the state gets the most out of what it has. “As business owners and advisors to business owners, we applaud the administration’s efforts to create efficiencies and get people involved. If the Governor can pull it off, it will enable us to invest in things that really matter.”

Righting the Balance Clark describes the shift from roles filled by the state legislature to local governments resulting from legislation like the Taxpayer Bill of

NewsAccount September/October 2011

Rights (TABOR) as challenging for Colorado to overcome. “We have robbed state government of being a player in foundational elements,” he says. “That’s not business friendly. That’s short-sighted and goofy.” Things like infrastructure, education, and affordable health care — things that should be handled at the state level — are drivers in an economy. Local governments, where the money and decisionmaking now lie, are more focused on quality of life issues, such as trails, parks, libraries, and art centers. While nice to have, these things don’t drive a state economy, and unfortunately, it’s the shift that has taken place in Colorado. “What matters to us now,” Clark says, “is that we adjust our state tax receipts up while reducing the local burden. It’s a difficult conversation to have, but we won’t survive very long with that out of balance.”

Colorado’s Albatross: The Business Personal Property Tax Colorado hasn’t been a manufacturing state for many years. One of the purported culprits? The state’s business personal property tax, which raises an estimated $823 million a year for counties, cities, special districts, and local school districts. Opponents call the tax, which is levied on a business’s equipment — everything from desks, chairs, and computers to equipment for a capital intensive manufacturing business — “onerous” and say it keeps those capital intensive businesses from coming to Colorado because of the very high corporate taxes that would be owed on the equipment. “It’s a competitive advantage for other states because it’s an additional cost of doing business in Colorado,” says Bertsch. “That tax is really a burr under our saddle,” says Berry. “It’s a factor that discourages

Fortune Revenues businesses looking at relocation or exCompany 500 Rank (millions) pansion in Colorado. Unfortunately, 1 DISH Network 193 $12,640.7 you can’t just get rid of it. Where’s 2 Qwest 209 $11,730 your replacement revenue? If it were Communications easy to do, we would have done it 3 Liberty Media 224 $10,982 long ago.” 4 Liberty Global 255 $9,667.7 The business personal property tax 5 Newmont Mining 260 $9,540 is like reverse psychology, says Clark, 6 Ball 300 $7,948.5 who is an economist by background. “We’re going to have to get serious 7 DaVita 359 $6,447.4 about it in coming years because 8 CH2M Hill 422 $5,422.8 America needs to start making things 9 Western Union 431 $5,192.7 again from a global competitive position.” ability to use operating losses at the state levHow soon the tax goes away is anyone’s el, says Bertsch. If you have an operating loss guess. Recent legislative efforts to address carry forward, you are limited in how much the tax have failed because of the fiscal im- of that you can use. pact, according to Loren Furman, CACI’s The state has also limited the use of the vice president of government relations. enterprise zone investment credit, which has been a significant shelter from state income taxes. Other Incentives All of these factors combine to make Historically, Colorado has not been par- Colorado less appealing to new business. ticularly competitive with other states in terms of giving out financial incentives for More Cons than Pros? companies to relocate here or even grow, says Berry. “Colorado offers some modest Suddenly it seems Colorado, which programs, but when you look at other states was ranked third in several polls and and what they do to lure companies, Colo- maybe made us feel a little bit smug rado isn’t very competitive,” he says. about living here, has a lot more negaFinancial incentives can be tricky to deal tives than positives going for it. The with, says Pilcher, recalling when United TMCC study encourages readers to focus Airlines was shopping around for a location on Colorado’s strengths — our state confor its maintenance facility in the early 90s. tinues to be a center of innovation and “When incentives were offered, a number has a highly educated workforce — but of Colorado businesses said, ‘Wait a minute, not rest on our laurels at a time when you’re going to provide these incentives to other states and countries are gaining a United? We’re already here; what about us?’ competitive advantage. It’s a big issue. What does the state do for “Colorado has so many things going for rank and file businesses that are already here?” it,” says Pilcher. “We do have our problems Other moves seen as business unfriend- like any other state, but there are a lot of ly include the state restricting a company’s good things happening, too.” s

The Colorado Blueprint In an effort to improve Colorado’s b u s i n e s s c l i m a t e , G o v. J o h n Hickenlooper in late July unveiled the Colorado Blueprint, an economic plan for the state built on public comments and county goals set during the first half of 2011. The plan highlights six focus areas for economic development: •

Build a business-friendly environment.

•

Recruit, grow, and retain businesses.

•

Increase access to capital.

•

Create and market a stronger Colorado brand.

•

Educate and train the workforce of the future.

•

Cultivate innovation and technology.

More than 5,000 Colorado residents from all 64 counties were involved in developing the Blueprint. According to the Hickenlooper administration, the document will continue to be updated over time, and it will be re-evaluated every nine months to measure progress on its goals.

For more on the Colorado Blueprint, go to www.colorado. gov/cs/Satellite/OEDIT/ OEDIT/1251595201376.

September/October 2011

www.cocpa.org

11

Greetings from the Road

Four Corners 2011-2012 CSCPA Chair Mike Bearup visits with members across Colorado during the 2011 Chair Tour.

Colorado Springs

Southeast 12

NewsAccount September/October 2011

Gathering for Good Networking YP Style The CSCPA hosted the 2011 Young Professionals Kickball Showdown on Aug. 13 at Clement Park in Littleton.

Taking home the trophy were the Clifton Kickers of Clifton Gunderson LLP, shown below.

2011 Showdown Sponsors

The Bridge to Our Future

Over 1200 college students and their advisors from across the country gathered, Aug. 11-13, for the Beta Alpha Psi 2011 Annual Meeting in Denver. The first day featured a community service event with Project Homeless Connect and Mile High United Way to provide services for the homeless and those at risk. At right, Theta Psi chapter members from the University of Northern Colorado, Greeley, and their advisor, Prof. Allen McConnell, assisted individuals through each step of obtaining critical services.

September/October 2011

www.cocpa.org

13

Estate Planning - It’s Never Too Late BY GEORGIA Z. PHILLIPS, CPA GRAT. QPRT. IDGT. ILIT. FLP. Given the abundance of acronyms used in estate planning, it’s no wonder clients can feel as if they are swimming in a bowl of alphabet soup. Estate planning laws are complex, and the focus on one’s mortality can combine to make a difficult task even more unpleasant. As a result, individuals arguably spend more time and effort planning their vacations than their estates. The main purpose of estate planning is to transfer a decedent’s assets upon his or her death. Without a comprehensive estate plan, a significant part of what an individual has achieved can be lost or end up in the hands of unintended beneficiaries. CPAs, together with a team of trusted legal and financial advisors, can help clients navigate this often confusing area, so that clients’ directives are met after they are gone.

• A recipient of property acquired from a decedent who dies in 2010 can receive fair market value, i.e. “stepped up” basis. Note that for a decedent who dies during 2010, an executor may elect to use modified carryover basis rules. (Consideration should be give to overall current and future tax impact before such an election is made.)

• Exemption portability. Any portion of the $5 million personal exemption not used at the death of the “first-to die” spouse can be used by the surviving spouse. • Estate and gift taxes are now unified — increasing the gift tax exemption from $1 million to $5 million. Thus, the $5 million exemption can be used during life or preserved until death. • The generation-skipping transfer tax exemption was increased to $5 million. • The estate, gift, and generation-skipping tax rate applicable in 2011 and 2012 is a maximum marginal rate of 35%.

14

• Use of valuation discount entities for transfer of a closely managed business or family investment assets. This technique takes advantage of discounting for lack of marketability or control. Such planning may involve the use of family limited partnerships (FLPs) or family limited liability companies (FLLCs). • Grantor retained annuity trusts (GRATs) can be used to freeze the value of an asset in the grantor’s estate while transferring most of the appreciation to the beneficiaries of a trust. • A sale to an intentionally defective grantor trust (IDGT) is a strategy whereby an irrevocable trust purchases an asset from a taxpayer in exchange for a promissory note. To the extent that the asset increases in value, or generates income in excess of the required debt service on the promissory note, such value will accrue for the benefit of the trust beneficiaries.

The 2010 Tax Relief Act The 2010 Tax Relief Act, signed into law by President Obama on Dec. 17, 2010, made significant changes to federal estate, gift, and generation-skipping transfer tax provisions. These changes may have a substantial and far-reaching impact on a client’s estate plan. The main provisions affecting estate taxation can be summarized as follows: • The estate tax exemption was increased to $5 million per individual.

• Lifetime gifting opportunities of $5 million per taxpayer are available for 2011 and 2012.

Although the 2010 Tax Relief Act increases both the estate and gift tax exemption amounts, and reduces the top marginal rate to 35%, the law applies only to tax years 2011 and 2012. Unless Congressional action is taken, the pre-2001 laws will apply in 2013, with a reversion to a $1 million estate and gift tax exemption with a top marginal tax rate of 55%.

Planning Opportunities Estate planning opportunities range from the simple to the complex and can include: • Gifts to an unlimited number of donees each year, as long as the annual gift exclusion per recipient isn’t exceeded. For 2011 the exclusion amount is $13,000 per donee, with $26,000 per donee for married taxpayers. • Unlimited gifts of tuition and medical expense payments, as long as the tuition or medical expenses are paid directly to the qualified educational institution or medical provider, respectively.

NewsAccount September/October 2011

• An irrevocable life insurance trust (ILIT) enables a taxpayer (the grantor of the trust) to purchase life insurance on his or her life. The trust is the owner of the policy, with the taxpayer being the insured. A beneficiary of an ILIT can be a spouse, child, or any other individual. If the trust is structured properly, the life insurance death benefits paid to the trust will not be included in the gross estate of the insured. • A taxpayer can gift a personal residence to a qualified personal residence trust (QPRT) for the benefit of the taxpayer’s children while retaining use of the residence for a specified period of time. The taxpayer’s retained interest in the residence reduces the value of the gift, allowing the taxpayer to transfer an asset for something less than its full fair market value.

Additional Considerations Estate planning is a continual process that, once addressed, should be revisited

in the case of major life events such as death, divorce, wealth, and special needs. Basic estate planning allows all individuals, regardless of wealth level, to create, promote, and protect their legacy. Well-planned estates avoid probate. If proper planning hasn’t been done, and a will doesn’t exist, assets will generally pass intestacy, according to the rules of the decedent’s state of residency. Additional issues that may need to be addressed to clarify a client’s vision for his or her estate include: • Protection with respect to catastrophic illness, assets, remarriage, creditors, divorce, and beneficiaries • Values promotion • Dealing with spendthrift heirs • Blended family issues • Medical directives, planning for incapacitation, and long term care needs • Special needs of a spouse or child

Conclusion As we approach year end and engage clients in tax planning conversations, now is a good time to initiate the subject of creating a good estate plan or reviewing an existing one. Effective estate planning can offer clients peace of mind, knowing they have provided for their loved ones and have made arrangements to protect and promote their legacy. This article is intended to be an overview of the 2010 Tax Relief Act estate tax legislation, and any planning opportunities are presented only as examples. It is strongly encouraged that practitioners and their clients obtain legal counsel during the design, review, and implementation of an estate plan. s

Georgia Z. Phillips, CPA, is a tax manager with Ryan, Gunsauls & O’Donnell, P.C., Denver. She is a member of the CSCPA’s Editorial Board and the CSCPA/Colorado Department of Revenue Joint Task Force. Contact her at gphillips@ rgo-cpa.com.

CDOR Update

Continued from 6

If a taxpayer has an eligible tax return, a payment plan may be set up. However, the full amount of the tax and half of any interest due must be paid by Dec. 31, 2011. For more information, go to www. colorado.gov/cs/Satellite/Revenue/ REVX/1251594484975.

Disallowed Conservation Easement Credits May 19, 2011, Gov. Hickenlooper signed into law House Bill 11-1300, which provides that the donor of a conservation easement, designated as the tax matters representative (TMR), has the option to waive the administrative hearing and appeal the disallowance of the credit directly to a district court. Or, the TMR may request an expedited administrative hearing and final determination. In accordance with Sec. 39-22-522.5(14) C.R.S., prior to issuance of a final determination or the conclusion of an appeal regarding a conservation easement tax credit, the Department will cease all actions to collect any amount of the disputed tax, interest, or other charges asserted to be owed. For more information and to review the legislation, go to www.colorado.gov/cs/Satellite/ Revenue/REVX/1251594611331.

tax; use tax; special event sales tax; retailer’s use tax; withholding tax; international fuel tax agreement tax; exempt fuel refunds; and individual income tax (available since April 25, 2011). The following services have been updated or are now available for the first time online for the taxes listed: • Access Your Account (Sign Up/Login) • File a Return • Amend a Sales Tax Return • File a Zero Sales Tax Return • Local Sales/Use Tax Rates • Sales Tax License Verification • Sales Tax Rates for Each Business Location within an Account • File a Zero Retailer’s Use Tax Return • Submit Electronic W-2’s or Type in W-2 Annual Reconciliation Data • Allow a Tax Preparer or Payroll Company to Submit W-2 Data for a Business • File a Zero Withholding Return • Make a Payment (by echeck, credit card, or through electronic funds transfer) • View Payments • View Letters from the Department • Change a Mailing Address • Close An Account • File a Protest

Revenue Online Access and Enhanced Functionality

2011 Forms In Process – One Form for Estimated Tax Payments Coming

The joint Colorado Society of CPAs/ Colorado Department of Revenue task force which was formed in May, 2011, has developed model language CPAs can use to inform their clients of the newly enhanced Revenue Online platform and to obtain consent to set up access to the client’s account as a third party. Go to www.cocpa. org for details. Revenue Online, www.colorado.gov/ RevenueOnline, the Colorado Department of Revenue’s secure portal where both business and individual taxpayers can access their Colorado income tax accounts, was upgraded, Aug. 29, 2011, to enhance existing features and add functionality. The system enables taxpayers to access information involving income tax (C-Corp., S-Corp., fiduciary, and partnerships); sales

The Department has begun designing the 2011 income tax forms and is seeking input. Expect to see significant changes to the individual income tax form, particularly the 104CR credit schedule. The changes are designed to encourage electronic filing, and the form will be geared toward the efiler. The Department’s goal: Simplified software that eliminates many of the errors that have caused credits initially to be denied. To review the proposed changes and provide feedback on the new forms, go to www.colorado.gov/cs/Satellite/Revenue/ REVX/1176842266433. In addition, the Department is eliminating the mailing of coupon books next year. Estimated tax payment vouchers will change to a single form to be used for any quarterly payment. s

September/October 2011

www.cocpa.org

15

Credit, Housing, and…Recovery? BY LOUIS S. BARNES

H

ere we are, four years from the beginning of the greatest bank run of all time, and we have no consensus about the wrongs that led to the run, little agreement about the mechanics of the run itself, and no agreement at all about how to get out of it. In July 2007, a bank-on-bank “wholesale” collateral-liquidation panic began, all large U.S. and European banks simultaneously discovering that several trillion dollars in collateral held against loans to each other were defective. As institutions tried to liquidate, markets quickly went “no bid,” many to this day with bids too low to accept and losses too big to recognize. This defective collateral was about half mortgage-related, with the other half in asset-based securities (ABS). Today the aggregate has collapsed by more than half the original $4.5 trillion outstanding. The run persists. The markets are closed to new ABS securitization, no matter how rigorously constructed. The run has spread outward, especially into housing, very much still in the grip of a classic credit-default/asset-deflation

spiral, in which default begets less credit, which causes assets to decline in value, and in turn begets more defaults and less credit. Yet, public discourse on the nature of our economic predicament is stuck in “overcapacity.” Or perhaps “deficient demand” caused by a protracted and inevitable need to “deleverage” from excessive debt. The Fed is trapped transfusing a patient with an open artery, the same for Keynesian stimulus, when the real problem is a balance sheet one. Assets unsupported by credit are falling in value with catastrophic effect on net worth both inside the financial system and within households. Since the housing bubble burst, some have advocated for the standard financialmarket prescription: clearing theory. Let prices fall as they may, and surely sellers will diminish and buyers arrive in numbers. Then the inventory will clear, and prices will be able to rise again. Others believe that homeowners should be kept in homes at all costs. Today we sit with no housing policy since the tax credit assistance expired in mid-2010.

The housing wealth effect, which added 8%-10% to disposable income annually from 2003 through 2006, is now running 3%-4% negative. The psychological effect of a quarter of American homes with mortgages underwater is as devastating as the direct financial consequence. Even owners of freeand-clear homes have suffered deep losses, as well as loss of liquidity — the simple ability to sell a home when needed. Since 2007, the aggregate value of U.S. homes has fallen from $22 trillion to $16 trillion, yet deleveraging has cut mortgage balances only from $11.2 trillion to $10.4 trillion. The mortgaged fraction of U.S. homes, about 70%, has little, if any, aggregate equity at all — precisely as economist Hiram Minsky described. Overdone efforts to deleverage are inevitably self-defeating, increasing leverage and defaults. The same is true for efforts to tighten credit. Post-bubble, never ever tighten beyond standards prevailing before the bubble. If you do, levered assets cannot escape the credit/deflation spiral. s

2011 Real Estate Conference November 11 Hyatt Regency-DTC Louis S. Barnes will discuss originalsource data from the Fed’s Z-1 to illustrate the credit bubble as it inflated and where we are now. He also will provide hard data on over-tightened mortgage credit, mortgage delinquency, and defaulted inventory, along with data on the actual credit situation beyond mortgages. This conference will be available in person or through live webcast. Register at www.cocpa.org/continuing-education/conferences.html, or call (303) 773-2877 or (800) 5239082.

16

NewsAccount September/October 2011

Educational Foundation News

CSCPA 2011 Scholarship Awards Congratulations to the following accounting students who were awarded scholarships from the Educational Foundation of the Colorado Society of CPAs. Each received $3000. Seventeen students received firm named scholarships of $3000.

Educational Foundation Scholarship Winners Molly Clark, a senior at Metropolitan State College of Denver, will graduate in 2011 with a B.S. in accounting. Tyler Daniels, a senior at Western State College, will graduate in December 2011, with a B.A. in accounting and business administration. Jonathan Havey, a junior at the University of Denver, will graduate in June 2013, with a BSAcc in accounting and film studies production. Keren Li is the recipient of the Educational Foundation Scholarship in memory of Dr. John D. Bazley. Li, a junior at the University of Denver, will graduate in June 2012, with a B.A. in accounting. Matthew Motz, a student at the University of Colorado-Denver, will graduate with a Masters in accounting. Lisa Norman, a junior at Colorado Mesa University, will graduate in spring 2013 with a B.S. in accounting.

Firm Scholarships Rabiou Alassani, recipient of the Mark J. Smith Scholarship, will graduate in May 2012 with a B.S. in accounting from Metropolitan State College of Denver. Alexandra Arnold, recipient of the Otto and Betty Butterly Scholarship, will

graduate in May 2012 with a concurrent B.S./M.S. in business administration with an emphasis in accounting from the University of Colorado at Boulder. Cyril Barton-Dobein, recipient of the PricewaterhouseCoopers LLP Scholarship, will graduate in May 2012 with a Masters in accounting from the University of Colorado at Boulder. Meghan Buckwalter, recipient of the Hein & Associates LLP Scholarship, will graduate in December 2011 with a B.S. in accounting from Colorado State University. Brooke Caton, recipient of the Past Presidents Scholarship, will graduate in May 2012 with a Bachelors in business administration, accounting, and Spanish from the University of Northern Colorado. Kelsey Carter, recipient of the Ehrhardt Keefe Steiner & Hottman PC Scholarship, will graduate in May 2013 with a B.S. in accounting and finance from Colorado State University. Liqian Jia, recipient of the Hugh C. Braly Scholarship, will graduate in November 2011 with a Masters in accounting from the University of Denver. Jonathan Kaiser, recipient of the KPMG LLP Scholarship, will graduate in June 2012 with a B.S. in accounting from the University of Denver. Nastassia Matusevich, recipient of the Gordon Scheer Scholarship, is expected to graduate in the spring of 2012 with a Masters of science from the University of Colorado at Denver.

istration and accounting from the University of Northern Colorado, Rebeka Pena, recipient of the Ehrhardt Keefe Steiner & Hottman PC Scholarship, will graduate in 2012 with a MAcc. from Colorado State University. Douglas Purdy, recipient of the Eide Bailly LLP Scholarship, will graduate in December 2012 with a B.S. in accounting and MPAcc from Metropolitan State College of Denver. Viola Sanchez, recipient of the Mark J. Smith Scholarship, will graduate in May 2015 with a B.S. in accounting and MBA from Colorado State University at Pueblo. Joubert Santiago, recipient of the Ehrhardt Keefe Steiner & Hottman PC Scholarship, will graduate in 2012 with an M.S. in accounting from the University of Phoenix. Oliver Tromp, recipient of the Ehrhardt Keefe Steiner & Hottman PC Scholarship, will graduate in May 2012 with a B.S. in accounting from the University of Northern Colorado. Christopher Winsley, recipient of the GHP Horwath PC Scholarship, will graduate in December 2011 with a B.A. in accounting from Western State College. Megan Woodruff, recipient of the Anton Collins Mitchell LLP Scholarship, will graduate in May 2012 with a Bachelors in business administration/accounting from the University of Northern Colorado.

Giana Mazza, recipient of the Ernst & Young LLP Scholarship, will graduate in June 2012 with a B.S. in business adminSeptember/October 2011

www.cocpa.org

17

The Hazards of Unclaimed Property BY JAMES M. BOAK, CPA

The amount of unclaimed property in the United States is estimated to be $30 billion to $40 billion. And that likely does not include the amounts not reported to state governments. The Colorado State Treasurer currently maintains a list of over 1.7 million names of individuals and businesses to whom property is owed but is unclaimed. Some states refer to these properties as “treasure” available to citizens. Colorado refers to it as the Great Colorado Payback. All states have unclaimed property laws that require the reporting and conveying of unclaimed property to the state by all companies and businesses. All are derived from medieval escheat laws under which all lost property went to the crown and local lords. Today this property is held by the state for the rightful owners. Knowing the unclaimed property laws in every state in which you do business could be critical to the sustainability of your business. Common unclaimed assets held by companies include: • checking accounts • savings accounts • oil and gas royalties • payroll wages • utility refunds • stocks and bonds • safe deposit boxes • uncashed insurance checks • mutual funds • money orders • dividends • security deposits

How do the laws work? After a certain period of time, a business (the property “holder”) must file a report with the state that provides information about the owner of the unclaimed property, such as the owner’s name, last known address, description of the property, etc. Then the holder must convey the property to the state. The state holds the property in perpetuity. In time, the state will sell the non-cash property for cash.

18

The state maintains a public list of unclaimed property, inviting owners to claim it. Money or property turned over to the state for safekeeping always belongs to the owner or heirs of the account, and there are no time limits for filing a claim. Periodically, the state may use a portion of the unclaimed cash, knowing that a substantial amount will never be claimed, even though it is still owed to the rightful owner in perpetuity. The state bases such a transfer on historical statistics.

How does it work in Colorado? Colorado’s unclaimed property laws are contained in the Colorado Revised Statutes 38-13, also known as the Unclaimed Property Act. The act contains rules for delay of reporting (called the dormancy period), remitting property, levying interest and penalties for compliance failure, and the handling of unclaimed property by the state administrator (Colorado Treasurer’s Office). The act specifies the handling by holders for all major types of assets. The rules are tailored to each class of asset. For example, the dormancy period varies by property types: Money orders - 7 years; outstanding checks - 5 years; property held by fiduciaries - 3 years; utility deposits - 1 year; gaming chips - N/A.

So, what are the hazards? Many companies, especially smaller ones, are unaware of, or may simply ignore, the filing and property remission requirements. For example, un-cashed checks are often simply erased from the outstanding check list and effectively taken into income. Unclaimed oil and gas royalties are carried on the books as liabilities for years — but are not timely remitted. If discovered by the Treasurer’s office in an audit, these actions can result in interest and penalties. Delays beyond the prescribed dormancy periods in Colorado are as follows: • Failure to deliver the property timely as prescribed results in interest at 18% of the property’s value and a penalty of 25% of the property’s value.

NewsAccount September/October 2011

• Failure to properly report unclaimed property after the dormancy grace period results in a penalty of $100 per day with a maximum of $5,000. • Willfully refusing to remit property after a demand from the Treasurer’s Office results in a civil penalty of three times the value of the property plus other possible civil penalties. To avoid these problems, companies should establish policies to detect unclaimed property annually and establish controls to insure timely filing of reports. This burden often falls on a company’s internal auditors and accountants. External CPAs, and especially auditors, should maintain current knowledge of unclaimed property laws in order to detect and advise companies on the existence of potential liabilities. For private and public companies, SFAS 5 (now ASC 450), Accounting for Contingencies, requires disclosure of, and possibly recording, material unclaimed property liabilities. Under the Sarbanes-Oxley Act of 2002, public companies must have controls to detect all material liabilities, including those related to unclaimed property, to be in compliance with securities laws.

Conclusion In a recent article, “Accounting for Unclaimed Property,” published in The CPA Journal, Sonia Walwyn perhaps said it best, “It is very important for accounting professionals to remember that unclaimed property laws apply to all businesses, including public accounting firms…Be knowledgeable and vigilant. Arming management with the tools needed to attain accurate and timely compliance will help insure that one’s financial statements [do in fact] present fairly [its financial position].” For more information, visit the National Association of Unclaimed Property Administrators at www.unclaimed.org and the Great Colorado Payback at www.colorado.gov/ treasury/gcp.s Contact James M. Boak, CPA, at jboak@ eidebailly.com. May/June 2011

www.cocpa.org

REGISTERED AGENT SERVICES FOR ALL ENTITIES LOWEST ANNUAL COST $79 PER YEAR BEST SERVICE AVAILABLE FOR COLORADO REGISTERED AGENT, LLC 743 HORIZON COURT, #107 GRAND JUNCTION, CO 81506 TEL: 877-355-8075 www.registeredagentcolorado.com OBTAIN SERVICES ONLINE OR OVER THE PHONE SAVE YOUR CLIENT’S MONEY

September/October 2011

www.cocpa.org

19

SEC Corner

Accounting Standards Update BY DONNA L. JOHNSON, CPA On June 15, 2011, the Financial Accounting Standards Board (FASB) issued Financial Accounting Standards Update No. 2011-05: Presentation of Comprehensive Income (Topic 220). This update does not change the accounting for comprehensive income, only the presentation of comprehensive income in the financial statements. The update is available for download at www.fasb.org. Under both generally accepted accounting principles in the United States (U.S. GAAP) and International Financial Reporting Standards (IFRS), a full set of financial statements must present comprehensive income in two parts: net income and its components, and other comprehensive income and its components. Current U.S. GAAP has three alternatives for presenting other comprehensive income and its components in financial statements. One of those presentation options is to present the components of other comprehensive income as part of the statement of changes in stockholders’ equity. This presentation in the statement of changes in stockholders’ equity is not an option under IFRS. Under IFRS, entities may present components of other comprehensive income either in a single statement of comprehensive income or in the second of two consecutive statements. Several recent projects by the FASB, such as accounting for financial instruments, and by the International Accounting Standards Board (IASB), such as pension accounting, may increase the volume and complexity of items reported in other comprehensive income. As a result, the FASB and IASB undertook a joint project to address concerns about differences in how comprehensive income is reported and to increase the prominence of other comprehensive income in financial statements. This project does not change whether items are reported in net income or in other comprehensive income and does not change the guidance on whether and when items of other comprehensive income are reclas-

20

sified to net income. The project addresses concerns about how reclassifications are presented in financial statements. All entities that report items of other comprehensive income, in any period presented, will be affected by the changes in this update.

Essential Elements To increase the prominence of items reported in other comprehensive income, the FASB decided to eliminate the option to present components of other comprehensive income as part of the statement of changes in stockholders’ equity, among other amendments in this update. For both U.S. GAAP and IFRS, the amendments require that all nonowner changes in stockholders’ equity be presented either in a single continuous statement of comprehensive income or in two separate but consecutive statements. In a single continuous statement, the entity is required to present the components of net income and total net income, the components of other comprehensive income, and a total for other comprehensive income, along with the total of comprehensive income in that statement. In the two-statement approach, an entity is required to present components of net income and total net income in the statement of net income. The statement of other comprehensive income should immediately follow the statement of net income and include the components of other comprehensive income, a total for other comprehensive income, and a total for comprehensive income. Regardless of whether an entity chooses to present comprehensive income in a single continuous statement or in two separate but consecutive statements, the entity is required to present on the face of the financial statements reclassification adjustments for items that are reclassified from other comprehensive income to net income in the statement(s) where the components of net income and the components of other comprehensive income are presented.

NewsAccount September/October 2011

An option remains in place for an entity to present components of other comprehensive income either net of related tax effects or before related tax effects, with one amount shown for the aggregate income tax expense or benefit related to the total of other comprehensive income items. In both cases, the tax effect for each component must be disclosed in the notes to the financial statements or presented in the statement in which other comprehensive income is presented. The amendments do not affect how earnings per share is calculated or presented. The amendments did not completely converge how comprehensive income is reported under U.S. GAAP and IFRS. Differences remain between the two standards as to whether an item of income is initially reported in net income or other comprehensive income. In addition, under IFRS not all items of other comprehensive income must be reclassified to net income.

Effective Dates For public entities, the amendments are effective for fiscal years, and interim periods within those years, beginning after Dec. 15, 2011. For nonpublic entities, the amendments are effective for fiscal years ending after Dec. 15, 2012, and interim and annual periods thereafter. Early adoption is permitted, and the amendments do not require any transition disclosures.s Donna L. Johnson, CPA, is a member of the CSCPA SEC Practice Forum and can be reached at johnsondlcpa@msn.com.

how do i choose the right accounting firm? Conduct in-person meeting

Industry and technical expertise

Quality – PCAOB

A firm that can grow with me

and Peer Review

Will they help me sleep better at night?

It was easy - we called acM 303.830.1120 www.acmllp.com MoneyBagAd.pdf

1

3/30/11

11:14 AM

What’s your practice worth? C

M

Don’t sell for too little Call or email today for a Free Practice Valuation Report.

Y

CM

Your Colorado Connection!

MY

CY

CMY

K

(303) 816-8213 Bill@APS-CO-TX.com Bill Anecelle, CPA, MBA

September/October 2011

www.cocpa.org

21

The State of The Industry:

Commercial Real Estate Throughout 2011, NewsAccount is talking with CPAs from various industries that are important in the U.S. and Colorado economies. We’re asking: What’s happening today? What factors will affect your industry over the the next 12 months? In this issue we focus on commercial real estate. BY NATALIE ROONEY

Bob Flynn

Founding Principal Crestone Partners, LLC, Denver

About The Organization Crestone Partners was founded in 2006. My two partners and I have over 75 years of combined experience in commercial and residential real estate investment and management. We invest primarily in mixed-use commercial real estate, but we also have interests in undeveloped land. Our firm provides asset management, property management, receivership, and consulting services to our partners and clients. Our areas of expertise include underwriting, financing, renovation, construction management, and repositioning and selling complex, mixed-use assets. Our principals and employees are recognized leaders in energy and environmental systems and have a proven track record of upgrading properties to achieve Energy Star and LEED certifications.

What role does commercial real estate play in the Colorado economy? As is the case in most of the rest of the country, commercial and residential real estate, particularly construction, play a major role in the health of Colorado’s economy. The industry employs 2.5 million Coloradans — over 100,000 of them in commercial and residential construction, alone. And during this severe recession, construction has been the hardest hit employment sector in the state. In addition

22

to construction jobs, thousands of Colorado residents are employed in commercial real estate financing, architectural and engineering services, property management and leasing, and investment brokerage services. In recent years, many Coloradans employed in commercial real estate architecture, engineering, and finance have lost their jobs. Since commercial real estate tends to be a trailing economic indicator — late to go into recession and late to come out of recession — most of those jobs lost during the recession will not return until an overall economic recovery is well underway.

What challenges face the commercial real estate industry in Colorado? Does this differ from national challenges? In my view, the biggest challenge we face in Colorado, and elsewhere, is for property owners to manage through an extended period of job losses. Through last year, Colorado lost over 130,000 jobs during the most severe recession we’ve experienced since the 1930s. Commercial real estate cash flow and valuations are strongest during periods of sustained job growth. Job growth drives demand for office, industrial, and retail space. Conversely, job losses drive up building vacancies and drive down rental rates. It is very difficult for commercial property investors and developers to thrive in an environment of falling rents, while costs of building materials escalate. There is reason to be optimistic, however. Colorado has added 11,000 jobs in the first

NewsAccount September/October 2011

five months of 2011, and unemployment has fallen here from 9.2 percent to 8.7 percent. Also, national media outlets such as CNBC, Forbes, and Business Week continue to rank Colorado as one of the top 10 states for businesses.

What is your role within Crestone Partners, LLC? I spend almost all of my time in two areas. First, I oversee day-to-day asset management functions for some of our existing real estate holdings, and second, I spend a great deal of time pursuing new business and investments on behalf of our firm and our institutional partners.